Compare Crypto Cards

Select up to 4 cards to compare side by side. See rewards, fees, custody models, and trade-offs without juggling multiple tabs.

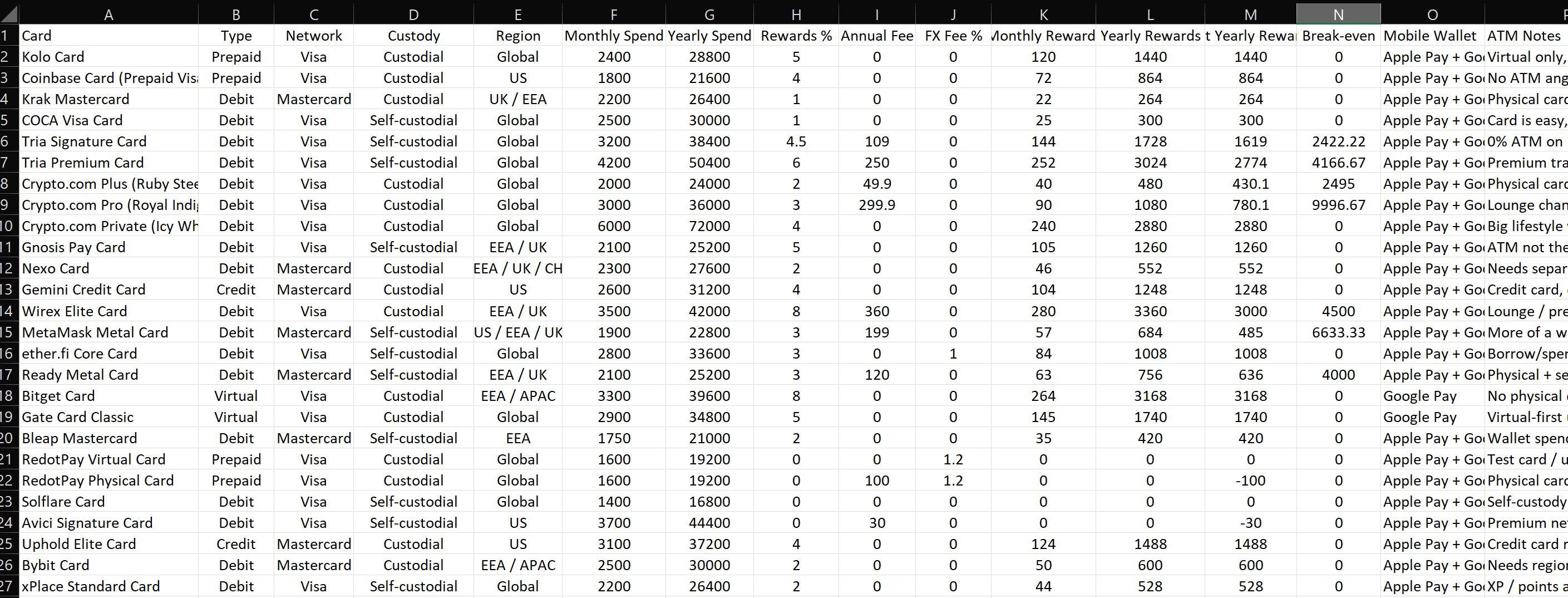

61 matching cards shown

Why We Built This Tool

Before I even started this project and gathered a team of people passionate about digital finances, my personal goal was to be able to maximize on my spending. I tried different online tools but they were either too cluttered or their information was just outdated and wrong. I would end up writing down my spending and returns on different cards in an Excel file to get a sense of what was working out and what was not.

Obviously, this would become too difficult to track with the ever-growing number of different cards with different benefits. So, when I started this whole project, a real comparison tool was the first thing I wanted to create. One place where the data is verified, the fees are transparent, and you can see exactly what you are getting before you commit.

The methodology section below explains how we evaluate each card. But the short version is: we do not rank by headline cashback alone. We look at what you actually keep after every fee, spread, and requirement is accounted for. If you want to see our top picks instead, you can check them out on our main rankings page.

Our Comparison Methodology

SpendNode evaluates crypto cards across seven critical dimensions, each weighted based on real-world impact on your finances and security. Our "Best for" recommendations at the bottom of each comparison use smart logic to match cards with user profiles, considering not just headline numbers but the complete cost-benefit equation.

Rewards Analysis

We highlight the strongest reward rates, but context matters. A card offering 8% rewards might require staking $15,000 worth of tokens that could lose 30% of their value in a market downturn. Our comparison shows the reward rate, but you still need the full card page to judge the underlying requirements and risks.

When multiple cards tie for the strongest rewards, we flag all of them. This lets you choose based on secondary factors like custody model, regional availability, or staking requirements rather than hiding the tie behind arbitrary tiebreakers.

Fee Structure Transparency

Annual fees are just the start. Our comparison includes:

- Foreign exchange fees: The 0.5-0.9% markup hidden in Visa/Mastercard exchange rates that most cards do not advertise

- Crypto conversion spreads: The 0.3-3% difference between mid-market rates and what you actually pay when spending crypto

- ATM withdrawal costs: Typically 1.5-2.5% effective fee when you include both card issuer and ATM operator charges

A card advertising "zero fees" might still cost you $240/year on $24,000 spending through conversion spreads. We surface these hidden costs so you can calculate true break-even points.

Custody Model Assessment

This is where security meets convenience. Self-custodial cards let you keep crypto in your own wallet until the moment of spending, protecting you from exchange bankruptcies like FTX, where users initially lost access to balances. Custodial cards require trusting an exchange with your funds, introducing counterparty risk.

Our comparison color-codes custody models: green for self-custodial, orange for custodial, and neutral for unknown or mixed cases. If you're comparing cards and see a self-custodial option, our "Best for Security" label flags it as the safer choice for users who care about counterparty risk.

Regional Availability

The best card in the world is useless if you cannot get it. We show exact regional availability and flag cards with unique geographic access. A card available only in the UK might earn a "Best for UK users" label if it is the sole option serving that market with competitive features.

Asset Support Depth

Some cards let you spend only BTC and ETH. Others support 200+ altcoins including DeFi tokens, gaming assets, and even precious metals. If you hold a diversified portfolio with 15 different tokens, a card supporting all Coinbase assets is more practical than one limited to five majors because you avoid the hassle of converting everything to BTC before spending.

Our comparison shows asset counts and lists the supported cryptocurrencies for each card, helping you verify your specific holdings are covered.

Network Differences: Visa vs Mastercard

This matters less than you'd think for most users, but regional quirks exist. Visa dominates some budget airlines and government services. Mastercard is often stronger in parts of the Middle East and among premium merchants. We badge each card's network so you can factor this into decisions if you shop at merchants with network preferences.

Benefit Verification

We verify key benefits with checkmarks in the comparison rows:

- Apple Pay support: Instant virtual card spending via iPhone or Apple Watch

- Google Pay support: NFC payments through Android devices

- No FX fee: True 0% markup on international spending

- No annual fee: Zero cost to hold the card, though spreads can still apply

- Cashback rewards: Earn crypto or cash-equivalent rewards on purchases

A card with checkmarks for Apple Pay, Google Pay, and No Annual Fee but missing No FX Fee means you can spend via mobile wallets without holding costs, but international purchases still incur hidden currency conversion markups.

What Different Users Should Prioritize

Digital Nomads and Frequent Travelers

Your priority: zero foreign exchange fees, the real kind, not the advertised kind. If you spend $30,000/year internationally, a card with genuine 0% FX saves you $180-270/year compared to competitors with hidden 0.6-0.9% exchange-rate markups.

Look for the "Best for Travelers" label in our comparisons. This flags cards that combine 0% FX fees with multi-region availability. Bonus points if the card supports multi-currency balances, letting you pre-convert at mid-market rates before your trip.

Red flag: cards available only in one region. You want global acceptance, ideally with both virtual card support for immediate use and a physical card for merchants that do not accept mobile payments.

Cashback Maximizers

Your priority: highest percentage rewards, but only if the math actually works. A card offering 8% rewards that requires staking $17,000 in exchange tokens needs careful analysis:

- Monthly spend: $3,000 x 8% = $240/month = $2,880/year in rewards

- Token staking risk: If token drops 30%, your $17,000 stake loses $5,100

- Opportunity cost: That $17,000 could earn 5-8% APY in stablecoins = $850-1,360/year

Our comparisons surface the strongest reward rates. Read the full card pages to understand staking requirements, token volatility history, and break-even calculations before committing capital.

Ideal scenario: a card with 3-4% cashback requiring zero staking. You earn rewards without locking capital or taking token price risk. If such a card exists in your region, our labels will flag it quickly.

Security-Conscious Holders

Your priority: self-custodial cards that do not require trusting an exchange. After FTX, Celsius, and Voyager collapsed in 2022, custodial risk is real. Even well-regulated exchanges can fail or freeze withdrawals during crises.

Look for the "Best for Security" label, which flags non-custodial cards. These connect to your own wallet, calculate rewards based on your holdings, but never require depositing crypto to an exchange.

Trade-off: self-custodial cards typically have fewer features than custodial exchange cards. You might sacrifice instant virtual card issuance or support for 200+ altcoins in exchange for security.

Budget-Conscious Users

Your priority: zero fees combined with decent rewards. You do not want to pay $99/year for a premium card when free alternatives exist, but you also want rewards that offset hidden spreads.

Look for the "Best for Budget" label on cards with $0 annual fees that still offer meaningful rewards. Calculate net benefit after fees:

- Annual spending: $18,000

- Card with 3% cashback, $0 annual fee: $540 rewards - $0 fee = $540 net

- Card with 5% cashback, $99 annual fee: $900 rewards - $99 fee = $801 net

Hidden gotcha: conversion spreads. A free card with 3% cashback but a 1.5% conversion spread on crypto spending effectively gives you 1.5% net rewards.

Altcoin Portfolio Managers

Your priority: wide asset support. If you hold 20 different tokens, you need a card that supports spending all of them, not just BTC and ETH. Otherwise you are stuck manually converting everything to a supported asset before loading the card.

Look for the "Best for Portfolio Diversity" label, which flags cards supporting large asset ranges. Use the assets row to verify your specific holdings are covered.

Bonus feature: if the card lets you set spending priority, you can optimize spreads. Spending from stablecoins is often cheaper than spending from illiquid altcoins.

Precious Metals Investors

Your priority: the ability to spend Gold or Silver holdings directly. This is an extremely niche feature, but if you hold precious metals as an inflation hedge, having instant spending liquidity without fully exiting your position is powerful.

How it works: you hold $50,000 in Gold on the card platform. You spend $2,000/month via the card. The platform converts $2,000 worth of Gold to fiat and then to the merchant instantly. You pay a 2-3% conversion spread, but you maintain most of your inflation hedge while still accessing spending power.

Alternative: sell Gold, withdraw to bank, and spend via bank card. No conversion spread, but you exit your entire position, wait for settlement, and trigger a taxable event.

How to Use Our Comparison Tool

Step-by-Step Process

Start with your region: Filter cards by where you live. A card with 10% rewards is useless if it is not available in your country.

Select 2-4 cards to compare: Click the plus button on cards that match your initial criteria. The sticky bottom bar shows your selections even while you keep filtering.

Click "Compare Cards": The side-by-side table reveals detailed feature comparisons. Highlighted cells show where a card leads on a given metric.

Read the detailed rows: Use the Assets and Benefits rows to verify your specific holdings, perks, and trade-offs before committing.

Check the "Best For" row: Our smart recommendations suggest which card excels for specific use cases.

Read full reviews: Use the issuer and product links in the comparison table to see complete breakdowns including fee structures, staking requirements, user scenarios, and bankruptcy risks.

Understanding Shareable Links

When you click Compare, the URL updates to include your selections, for example ?comparing=true&cards=card1,card2,card3. This lets you:

- Bookmark comparisons: Save specific card matchups for later review

- Share with others: Send your comparison to friends or advisors for second opinions

- Return later: Your selections persist even if you close the browser, thanks to localStorage

Pro tip: if you're researching cards for a group, create comparison links for different scenarios and share them in a spreadsheet for group decision-making.

Common Comparison Scenarios

Scenario: Choosing Between High Rewards vs Low Fees

You're comparing a card with 8% rewards but a $15,000 token staking requirement against a card with 3% cashback and zero staking.

Decision framework:

- If you already hold the token and are bullish, the higher-reward card may win

- If you'd need to buy the token specifically for the card, calculate opportunity cost

- If you're risk-averse or the token is volatile, the lower-requirement card often wins despite lower rewards

Use our comparison to see both options side by side, then click through to full reviews for break-even calculations and token volatility history.

Scenario: Self-Custody vs Convenience

You're comparing a self-custodial card with 3% rewards and limited features against a custodial card with 6% rewards, instant virtual issuance, and 200+ assets.

Decision framework:

- If security is paramount, the self-custodial card may win

- If you need to spend obscure altcoins immediately, the custodial card's asset breadth may win

- If you are comfortable with custodial risk from a regulated exchange, the higher reward rate may justify it

Our "Best for Security" label flags the self-custodial option. If that matters to you, choose it even at the cost of features.

Scenario: Regional Restrictions Limiting Choices

You live in the UK and most cards you're comparing show US-only or region-limited access.

What to do:

- Use the region filter at the top of the comparison page to show only UK-available cards

- If only 2-3 cards remain, compare those even if they are not the best globally

- Our comparison may show a regional recommendation when one card is uniquely available in your market

Do not chase features you cannot access. A mediocre card you can actually get beats an amazing card that rejects your application due to regional restrictions.

When Not to Compare Cards

Sometimes comparison shopping is overkill. Skip the detailed analysis if:

- You already have a card and it works: switching costs may outweigh a 1% reward difference

- Your spending is under $500/month: even a 5% reward difference is only $25/month

- Only one card serves your region: there is no point comparing if you have no alternatives

- You need a card immediately: instant virtual cards beat superior cards with long shipping times if you are traveling tomorrow

Use comparisons for big decisions: your primary spending card, large monthly volumes, or long-term holdings. For secondary cards or small amounts, pick the first reasonable option and move on.

Beyond the Comparison: What to Read Next

Our comparison tool surfaces the key differences, but some decisions require deeper research:

- Our review methodology: How we verify fees, test cards, and calculate ROI scenarios

- Self-custody vs custodial cards: Deep dive on security trade-offs and bankruptcy risk

- Cashback strategies: How to maximize rewards including tax implications

- True zero FX fees explained: Why most 0% FX claims are misleading

For card-specific details, click through to the full vendor and product pages for deeper breakdowns of fees, supported assets, limits, and risks.

Comparison Data Verification

All comparison data is verified from official card issuer sources and updated regularly. We check:

- Card terms and conditions pages for fee structures

- Help centers for spending limits and supported regions

- Blockchain explorers to verify asset support claims where relevant

- Regulatory filings for custody and issuer structure where available

Our database revalidates every 10 minutes via Incremental Static Regeneration. If a card changes its cashback rate or adds a new region, the comparison reflects it within the next update cycle.

Spot an error? Cross-reference our data with issuer websites before making final decisions, especially for time-sensitive promotions or limited-time reward offers.

Final Thoughts: The Best Card Is Personal

There is no universal "best crypto card." The optimal choice depends on your location, spending volume, custody preferences, portfolio composition, travel patterns, and risk tolerance.

Use our comparison tool to narrow your options to two or three finalists, read their full reviews to understand trade-offs, then pick the one that aligns with your priorities. The perfect card that does not fit your life is worse than the good-enough card you will actually use.

Questions? Our individual card reviews include user scenarios matching common profiles. Find someone with similar spending patterns and see which card worked for them. That is often the best predictor of your own experience.

Disclaimer: SpendNode is a data comparison platform. We are not financial advisors. Crypto cards involve risks including asset volatility, custodial risk, and tax complexity. Verify all terms directly with issuers before applying.

Written by Aleksandar Dukic