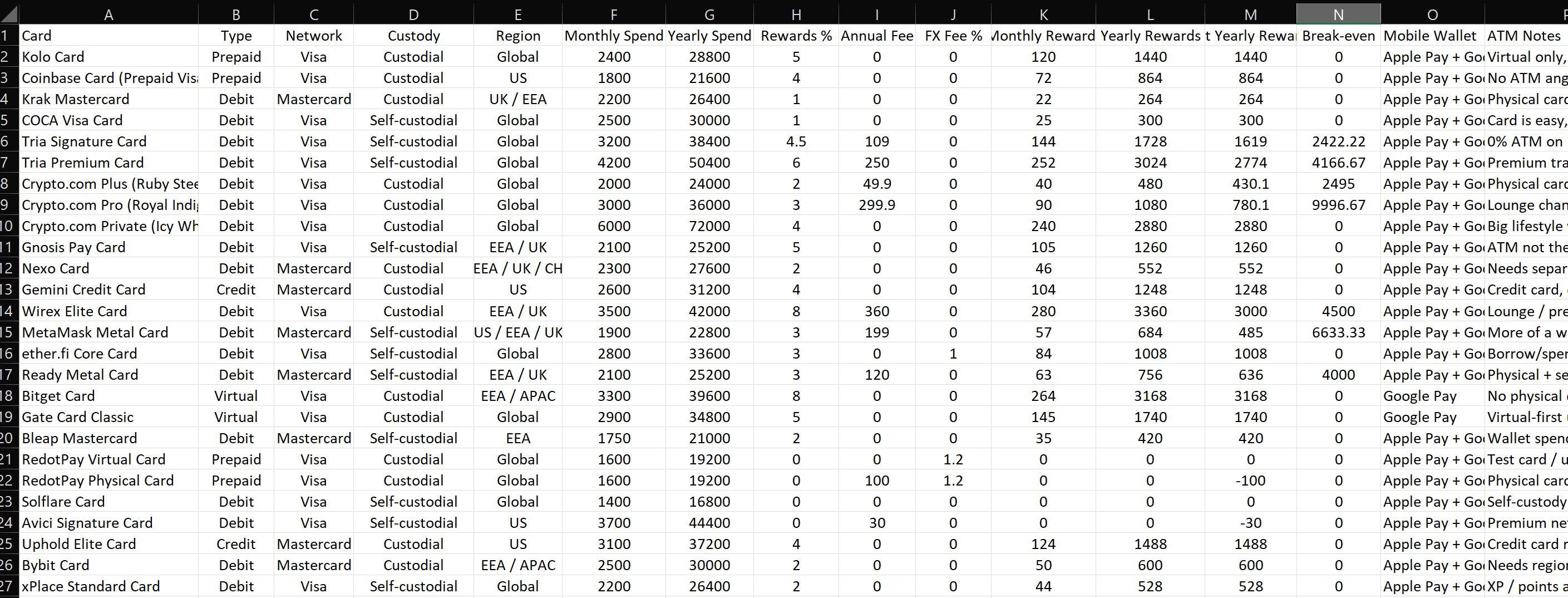

Compare Crypto Cards

Select up to 4 crypto cards to compare side by side. See rewards, fees, custody models, and trade-offs without juggling multiple tabs.

Last modified: Aug 9, 2026

71 matching cards shown

Why We Built This Crypto Card Comparison Tool

Before SpendNode existed, comparing crypto cards meant opening ten tabs, guessing which fee pages were still current, and usually ending up in a spreadsheet. That was not a serious way to make a money decision, especially once cards started adding token locks, hidden FX drag, and different custody models.

This tool exists so you can compare the important parts in one place: rewards, fees, custody, availability, and what the card is actually trying to be.

That spreadsheet became the tool above: every card lined up on the same rows, with the numbers already filled in.

How to Compare Crypto Cards

Start with your region. Then narrow the list to two to four cards that are actually available to you. After that, use the table to check what matters for your use case:

- rewards and whether they come with staking or fee drag

- custody model and counterparty risk

- FX and annual-fee structure

- supported assets and funding flow

- Apple Pay, Google Pay, ATM, and card-type differences

The point is not to turn every decision into a giant research project. It is to get you from a messy shortlist to a believable final choice.

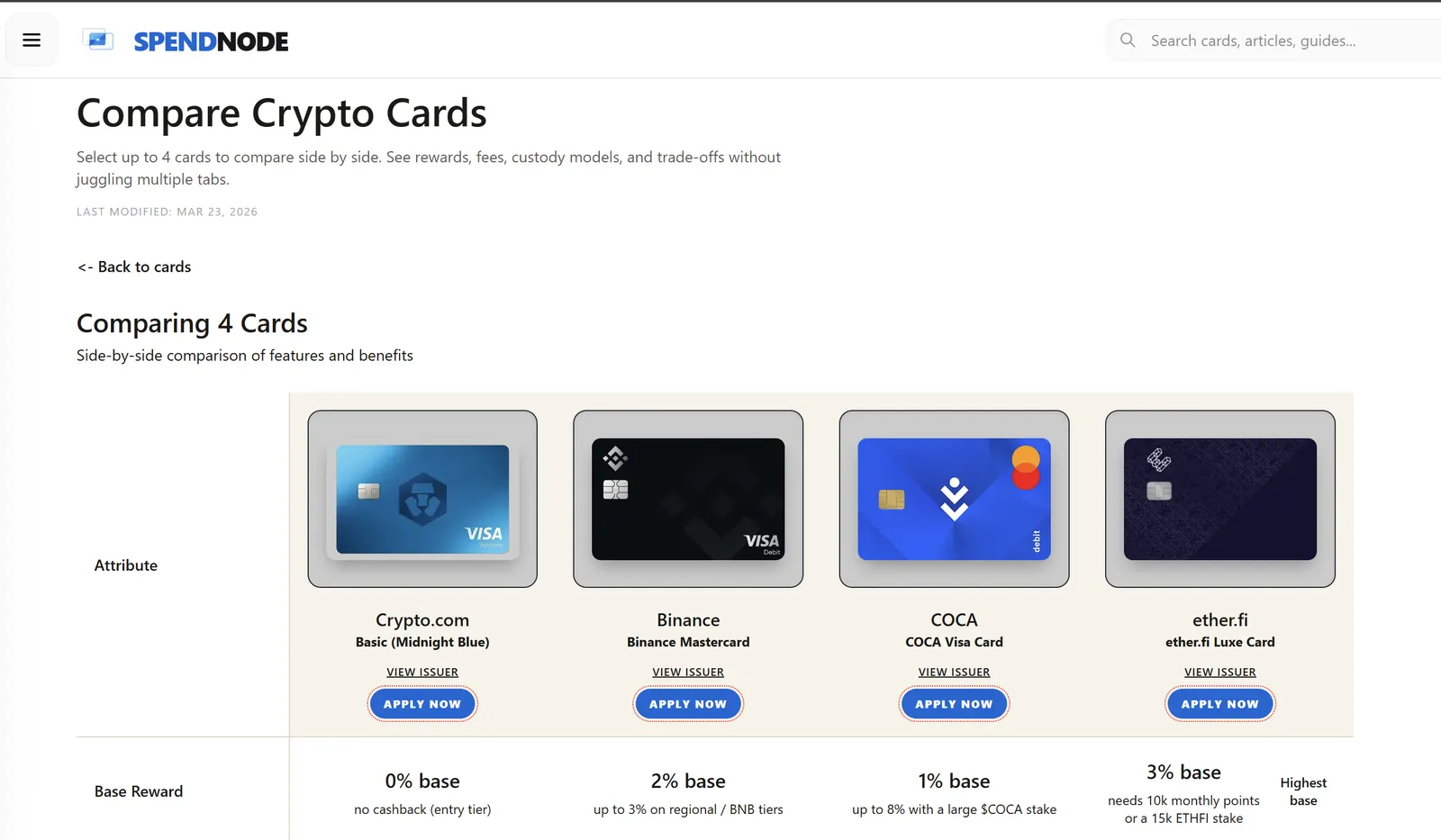

Crypto Cards Compared: Side-by-Side Examples

See how specific cards stack up head to head. Each comparison breaks down rewards, fees, FX, custody, and who the card actually suits.

Binance vs Bybit

Rewards, fees, FX costs, regional availability, BNB cashback, Bybit points, and which card fits you.

Compare Binance and BybitCOCA vs Tria

Real net cashback, 0% vs 1% FX, staking requirements, 15% vs 6% yield, and which card actually wins.

Compare COCA and TriaCOCA vs ether.fi

Debit vs credit line, COCA's 0% FX against ether.fi's low margin, COCA's 1-8% staking tiers against ether.fi's free 3%, and the capital-gains gap for ETH holders.

Compare COCA and ether.fiether.fi vs Tria

Credit line vs debit, free 3% against Tria's capped Season 3 tiers, ether.fi's low FX margin against Tria's 1%, ETH staking vs 15% APY, and the capital-gains gap.

Compare ether.fi and TriaJupiter vs KAST

Jupiter's free 2% base (up to 4% by referring friends, capped at $100/month, withdrawable, plus a $20 bonus) against KAST's lower 0.5% FX, physical metal cards, and tiers that scale for heavy spenders.

Compare Jupiter and KASTKAST vs Plasma One

Stable USD cashback at 0.5% FX but locked to card spend, against Plasma One's higher XPL-token cashback, self-custody, and up to 5% balance yield.

Compare KAST and Plasma OneWhat We Care About Most

We do not treat headline cashback as the whole story. A card advertising 8% back can still lose on real-world value once you factor in staking requirements, token volatility, conversion spread, monthly caps, and annual cost.

That is why the comparison is built around context:

- reward rate

- fee stack

- custody model

- regional fit

- product practicality

If two cards tie on the obvious headline metric, the next job is to show you where the real difference sits.

Where the Headline Number Can Mislead

A few examples show why the top reward line is a starting point, not an answer.

Say you spend about $2,000 a month abroad, or $24,000 a year. A card that advertises zero FX but quietly bakes a 0.9% spread into its exchange rate costs you around $216 a year in drag that never shows up as a line item. That is enough to wipe out a full 1% cashback edge over a card with genuine no FX fees. For anyone spending mostly outside their home currency, the FX line often matters more than the reward line.

Now take a card paying 8% that asks you to lock $15,000 in the issuer's token. On $3,000 a month of spend, that 8% is roughly $2,880 a year, against about $1,080 from a no-lock 3% card. The gap looks decisive until you price the lock. That $15,000 would earn near $900 a year just sitting in stablecoins, and if the token drops 30% you are down $4,500 on the stake alone, several years of reward advantage gone in a single drawdown.

Then there are caps. A 5% rate capped at $200 of monthly spend pays at most $10 a month, or $120 a year, no matter how much you run through the card. Spend $1,500 a month and your real rate is closer to 0.67%, not 5%. Caps are where the headline and the lived rate drift furthest apart, so we read the cap before the percentage.

None of this fits in one number, which is why the comparison sets the fee stack, the lock, and the cap next to the reward instead of behind it.

What Different Users Should Prioritize

For Travelers

Zero FX should mean zero FX in practice, not just in the headline. If you spend abroad often, the right card is usually the one with the cleanest total cost stack rather than the flashiest reward line.

For Cashback Chasers

Look at net value, not just the posted percentage. If a reward depends on a large token lock or disappears after a cap, that needs to show up in the decision.

For Security-Focused Users

Custody matters. If you care about keeping control of your assets, self-custodial options should be evaluated differently from exchange-linked cards, even when the latter look smoother on rewards.

For Simplicity

Sometimes the best card is not the one with the highest upside. It is the one you can actually explain, fund, and use without creating three new problems.

How to Read the Results

Use the table to eliminate weak fits first. Then click through to the full product and vendor pages for the cards that survive.

The comparison tool is the fast decision layer. The card pages are where we go deeper on:

- break-even math

- real tradeoffs

- editorial rating

- country fit

- screenshots and hands-on notes

What the Tool Can't Show You

The comparison gets you to a shortlist quickly, but a few things only the full card page or the issuer can tell you.

Promotions move faster than any review cycle. A signup bonus or a limited reward boost can appear or expire within a week, so check the live offer before you apply, and our promo codes page when something is running.

Approval odds and onboarding are personal. Two people in the same country can end up with different limits, KYC steps, or funding options depending on their wallet and history.

App quality does not fit in a table. Funding flow, in-app support, and how painful a dispute is are things you only feel once the card is in your phone. That is what our hands-on notes and screenshots on the individual card pages are for.

Crypto Card Comparison FAQ

Which crypto card actually has no FX fee?

Most "0% FX" claims still fold a 0.5% to 1% spread into the exchange rate, so a truly fee-free card is rarer than the marketing suggests. We track the ones that hold up on the no FX fee page, and the comparison flags where advertised and real diverge.

Are crypto card rewards and spending taxable?

In most countries, spending crypto counts as a disposal that can trigger capital gains, and rewards can be treated as income. The rules vary a lot by country, so treat this as a flag rather than advice and confirm with your local tax authority before you lean on a card for large volumes.

Self-custody or custodial, which is safer?

A self-custodial card lets you hold crypto in your own wallet until the moment you spend, so an issuer failure does not strand your balance. Custodial cards tend to be smoother and carry more features, but you are trusting the platform with your funds. If counterparty risk is your main worry, start there.

What is the best crypto card for travel?

There is no single winner, but the shortlist is usually whatever pairs true zero FX with wide acceptance and both a virtual and a physical card. Filter by your region first, then weigh the no FX and Apple Pay and Google Pay lines against the reward rate.

How often is the comparison data verified?

We re-check fees, rewards, and availability against issuer sources on a rolling cycle and stamp each card and page with a verified date. Our methodology explains how. Promotions and rates can still shift between cycles, so confirm anything time-sensitive on the issuer's own site.

Can I compare cards that are not available where I live?

Yes. The tool shows everything by default, and the region filter narrows it to what you can actually get. A strong card that rejects your application helps no one, so set your region early.

Final Thought

There is no universal best crypto card. There is only the best card for your region, funding flow, custody preference, and spending style.

That is what this page is trying to make visible, quickly and without marketing noise.

Disclaimer: SpendNode is a data comparison platform. We are not financial advisors. Crypto cards involve risks including asset volatility, custodial risk, and tax complexity. Verify all terms directly with issuers before applying.

Written by Aleksandar Dukic