SpendNode Rating for COCA

COCA is one of the strongest issuer stories in the market because the lineup is ambitious, the self-custody angle is real, and the cards are built to compete on value rather than just ideology.

The upside is obvious: strong product ambition, distinctive structure, and category relevance. The score stops short of the very top because token-tier complexity still adds real friction.

Issuer Snapshot

Editorial vendor score stays separate from user reviews. Methodology

Product Quality

4.3

Trust & Custody

4.2

Fee Transparency

3.8

Operational Reliability

4.0

Market Relevance

4.4

On This Page

What Is COCA?

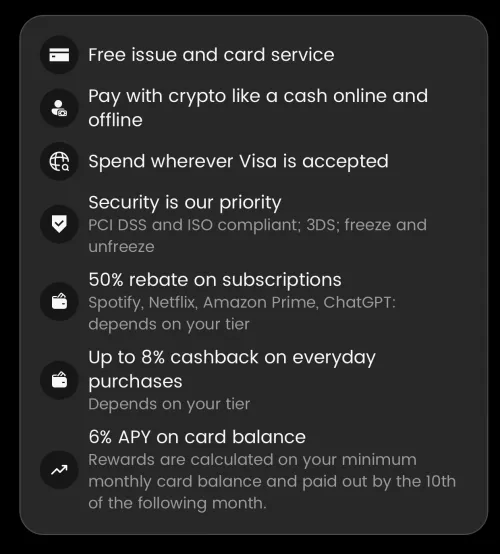

COCA is a self-banking super app offering a non-custodial Visa debit card (not a credit card) issued by Wirex, with up to 8% stablecoin cashback within monthly allowance (1% after) across six staking tiers (Starter through Elite), 0% FX fees, and 6% APY on stablecoin balances via Morpho lending markets (tier-based caps from $5K to unlimited).

Additional features include 50% subscription rebates across four categories (Video Streaming, AI Assistants, Music, Marketplaces) scaling by tier with $70/mo cap per service, personal IBAN with SEPA transfers, $200/month free ATM withdrawals, and smart contract wallet security powered by Privy (ERC-4337/EIP-7702). Available in 70 countries.

Curve Integration Update (Feb 2026): COCA is continuing to support Curve and is not discontinuing the integration. Until March 31, Curve transactions remain eligible for full cashback under your current tier. Starting April 1, cashback on Curve transactions moves to 1% for all users regardless of tier, with no limits.

Deposit address reminder (Apr 2026): COCA says crypto deposit addresses changed with the COCA 3.0 upgrade. Before sending funds, open the COCA app, go to Add Money, choose Crypto Deposit, and copy the current deposit address. Funds sent to an old address may not arrive.

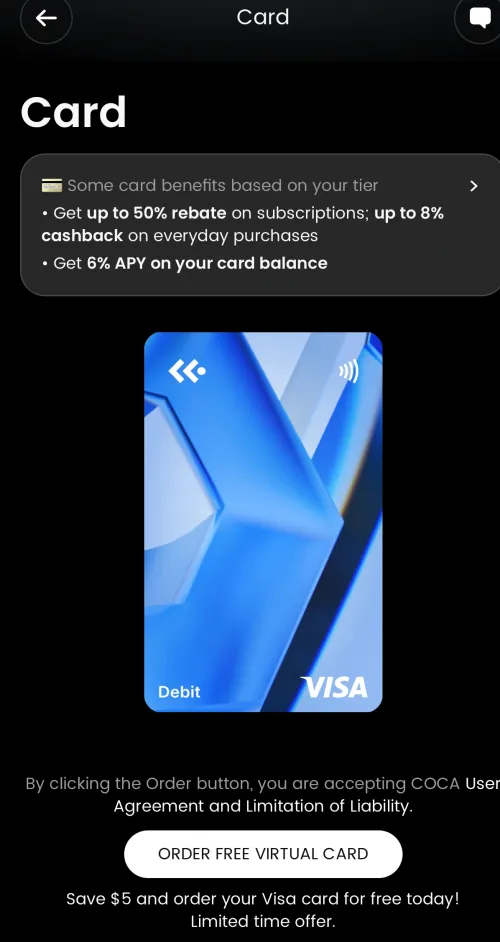

SpendNode app screenshot

COCA Visa Card - Non-custodial Visa debit with up to 8% cashback, 50% subscription rebates, and 6% APY via Morpho. Issued by Wirex, available in 70 countries.

The app bundles all of these into a single non-custodial wallet with up to 50% hotel discounts and Apple Pay/Google Pay. No other crypto card in 2026 combines this many reward streams in one product.

The architecture differs from exchange-linked cards in three concrete ways. COCA uses Privy-powered smart contract wallets (ERC-4337/EIP-7702) where you control your funds. The yield comes from Morpho lending markets managed by Gauntlet, not from COCA subsidizing rates. The card is issued by Wirex (FCA-regulated UK, licensed EEA). Over 1M users globally across 70 countries.

The catch remains the $COCA token. Maximum benefits require staking 30,000 $COCA for Elite tier, a small-cap token trading on MEXC, BitMart, and DEXes. Staked tokens are locked for the duration of your tier membership, and unstaking requires cancelling your tier followed by a 30-day cooldown. We recommend starting at Starter tier (zero staking needed): 1% cashback, 0% FX, and 6% APY on balances up to $5K is a competitive baseline. The gap between Starter and Elite is where the risk-reward calculation lives.

The Ecosystem: One Product, Six Tiers

COCA Visa Card - Non-custodial Visa debit card. Tiers require staking $COCA tokens (locked during membership, 30-day cooldown to unstake after cancellation). Card issued by Wirex.

Available crypto cards by COCA in August 2026

1. COCA Visa Card

Self-Banking: 8% Cashback + 6% APY + 0% FX

Fees and Rates

| Fee | Cost | Notes |

|---|---|---|

| Annual fee | $0 | All tiers |

| FX fee | 0% | Zero FX fees on all currencies |

| ATM withdrawals | $200/month free | 2% on amounts above $200 |

| ATM daily limit | 850 EUR | Max 5 transactions/day |

| ATM monthly limit | 5,000 EUR | |

| Virtual card | Free | All tiers |

| Physical card | $20 | Free for Premium/Premium+/Elite |

| Trading fee | 0% | Commission-free |

| Cross-chain swaps | Free |

Purchase limits: 30,000 EUR per transaction, 30,000 EUR/day, 30,000 EUR/month, 75,000 EUR/quarter, 100,000 EUR semi-annually.

COCA charges 0% FX on all currencies. Combined with $0 annual fee, free virtual card, and $200/month free ATM withdrawals, COCA has one of the cleanest fee structures of any crypto card. The zero FX model means cashback rate equals net return regardless of which currency you spend in.

Fees and ROI framework

$0 annual fee. 0% FX on all currencies. $200/month free ATM (2% above). Six staking tiers: Starter (0) 1%, Standard (stake 300) 3%/$1K allowance, Standard+ (stake 1K) 4%/$1.75K, Premium (stake 3K) 5%/$2.5K, Premium+ (stake 10K) 6%/$5K, Elite (stake 30K) 8%/$10K. Above monthly allowance, 1% cashback. Staked tokens locked during membership, 30-day cooldown to unstake.

6% APY on stablecoin balance up to tier cap ($5K-unlimited, 2% above). 50% subscription rebates by category (Video/AI/Music/Marketplaces) scaling by tier, $70/mo cap per service. At Elite with $3,000/month (within $10K allowance): $2,880 cashback + APY + sub rebates = approx. $3,300+/year. Break-even on token risk depends on $COCA price stability.

Rewards and Cashback

SpendNode app screenshot

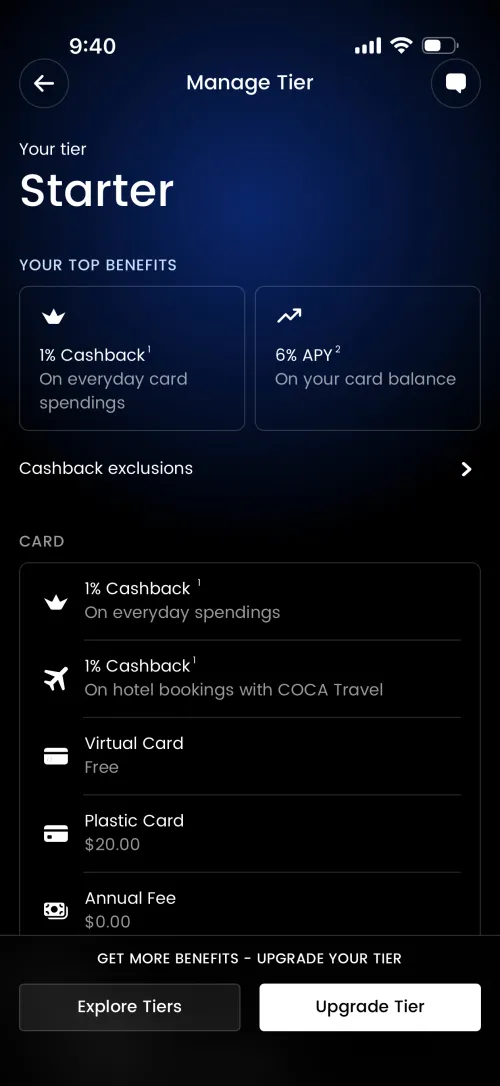

Starter Tier - No tokens required. 1% cashback, 6% APY, free virtual card. The baseline tier for testing COCA's card, IBAN, and yield stack without adding token exposure.

| Tier | $COCA Staked | Cashback | Monthly Allowance | APY Cap | Plastic Card |

|---|---|---|---|---|---|

| Starter | 0 | 1% | - | $5K | $20 |

| Standard | 300 | 3% | $1,000 | $50K | $20 |

| Standard+ | 1,000 | 4% | $1,750 | $250K | $20 |

| Premium | 3,000 | 5% | $2,500 | $500K | Free |

| Premium+ | 10,000 | 6% | $5,000 | Unlimited | Free |

| Elite | 30,000 | 8% | $10,000 | Unlimited | Free |

All tiers: $0 annual fee, free virtual card, 6% APY up to tier cap (2% above cap), 0% FX fees, 0% trading fees, free cross-chain swaps. Above monthly allowance, all purchases earn 1%. Premium/Premium+/Elite get 100% card issue fee rebate (delivery not included).

SpendNode app screenshot

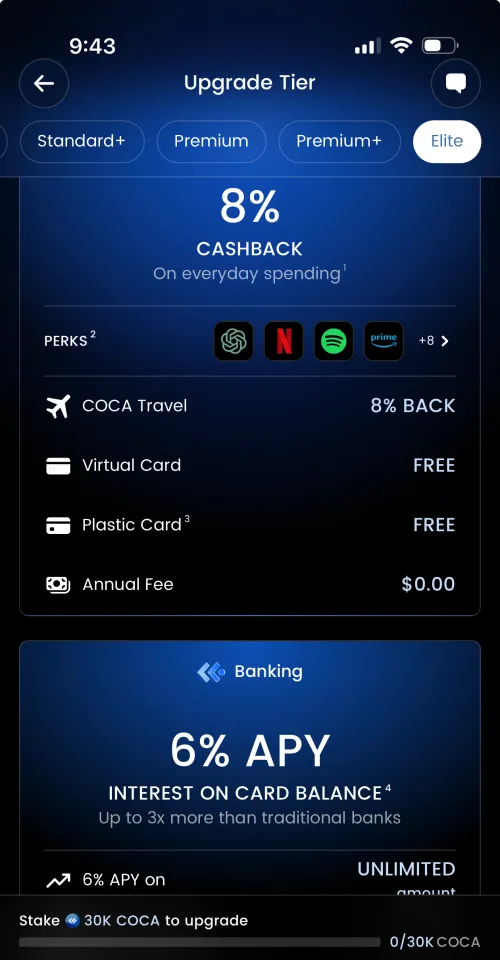

Elite Tier - 8% cashback on first $10,000/mo, all subscription rebates across 4 categories, unlimited 6% APY. Requires staking 30,000 $COCA tokens (30-day cooldown to unstake).

Subscription rebates scale by tier and category. Standard gets 1 service from Video Streaming (Netflix, Disney+, Paramount+, YouTube Premium). Standard+ and Premium add AI Assistants. Premium+ adds Music. Elite adds Marketplaces. Each category allows one subscription at 50% back, $70/mo cap per service. Starter gets none.

Technology: Privy Smart Wallets + Morpho Yield

COCA's architecture is built on three pillars:

1. Privy Non-Custodial Wallets (ERC-4337/EIP-7702)

- Smart contract wallets where you control the keys - COCA cannot move your funds

- Privy handles key management: SOC 2 Type I and Type II certified, audited by Cure53, Zellic, and Doyensec

- Biometric recovery (no seed phrase needed, though private key export is available)

- Card payments use authorization-based spending: each transaction approves only the specific amount for that specific merchant

- Apple Pay and Google Pay integration

2. Morpho + Gauntlet APY Engine

- 6% APY generated from Morpho on-chain lending markets (not COCA subsidizing rates)

- Gauntlet provides risk management: curated allocations, supply caps, ongoing monitoring

- Interest calculated on minimum monthly card balance (minimum $1 required), paid by the 10th of the following month in stablecoins

- The 6% comes from actual borrowing demand on Morpho, not from COCA topping up rates

3. IBAN Banking Layer

- Personal IBAN for SEPA bank transfers in EUR (USD where available)

- Receive salary directly to COCA

- Send/receive money like a regular bank account

- Top up via bank transfer, debit/credit card, or stablecoins

Supported assets: USDC, USDT, ETH, BTC, plus popular coins via the Crypto Account.

How to Apply for the COCA Crypto Card

COCA is a non-custodial Visa run through a Privy smart wallet, so there is no seed phrase to write down and no bank-style credit check. Setup is about ordering the card, picking a tier, and funding a balance that earns yield. Here is the flow from sign-up to first payment:

SpendNode app screenshot

The free virtual Visa works anywhere Visa is accepted, with rebates, cashback, and 6% APY that scale with your tier.

- Create your account. Download the COCA app and set it up. COCA uses a Privy smart wallet, so you sign in with an email or passkey rather than a seed phrase.

- Order your free virtual card. Tap Order Free Virtual Card to issue a Visa instantly. A plastic card is optional for around $20.

- Pick your tier. Start on Starter (free, 1% cashback) and move up through Standard, Standard+, Premium, Premium+, and Elite. Higher tiers raise cashback toward 8% and are unlocked by staking COCA, with Elite at 30,000 COCA.

- Get your account details. COCA opens a personal IBAN, so you can receive SEPA transfers, salary, and bills alongside crypto.

- Fund your balance. Deposit supported crypto into your COCA balance, which stays in your non-custodial smart wallet and earns 6% APY through Morpho. Use a fresh deposit address each time, since COCA rotated addresses in the 3.0 upgrade and funds sent to an old one will not arrive.

- Add to Apple Pay and spend. Once funded, add the card to your mobile wallet and spend anywhere Visa is accepted at 0% FX, with cashback and subscription rebates set by your tier.

Countries and Availability

COCA is available in 75 countries as of August 2026. We count a country here when at least one active COCA card variant lists it, so individual product pages may be narrower.

Available Regions

Africa

Ghana (GH), Kenya (KE), Nigeria (NG), South Africa (ZA), Uganda (UG)

Americas

Argentina (AR), Brazil (BR), Chile (CL), Colombia (CO), Ecuador (EC), El Salvador (SV), Mexico (MX), Panama (PA), Peru (PE)

Asia

Azerbaijan (AZ), Georgia (GE), Hong Kong (HK), Israel (IL), Japan (JP), Kazakhstan (KZ), Macau (MO), Malaysia (MY), Oman (OM), Philippines (PH), Saudi Arabia (SA), South Korea (KR), Taiwan (TW), Thailand (TH), Turkey (TR), United Arab Emirates (AE), Uzbekistan (UZ), Vietnam (VN)

Europe

Andorra (AD), Austria (AT), Belgium (BE), Bulgaria (BG), Croatia (HR), Cyprus (CY), Czech Republic (CZ), Denmark (DK), Estonia (EE), Finland (FI), France (FR), Germany (DE), Gibraltar (GI), Greece (GR), Guernsey (GG), Hungary (HU), Iceland (IS), Ireland (IE), Isle of Man (IM), Italy (IT), Jersey (JE), Latvia (LV), Liechtenstein (LI), Lithuania (LT), Luxembourg (LU), Malta (MT), Moldova (MD), Monaco (MC), Montenegro (ME), Netherlands (NL), Norway (NO), Poland (PL), Portugal (PT), Romania (RO), Slovakia (SK), Slovenia (SI), Spain (ES), Sweden (SE), Switzerland (CH), Ukraine (UA), United Kingdom (GB)

Oceania

Australia (AU), New Zealand (NZ)

Major Restricted Markets

These major markets are not currently listed for this vendor. Confirm eligibility with the issuer before applying, especially where card tiers have different country rules.

Africa

Egypt (EG)

Americas

Canada (CA), United States (US)

Asia

China (CN), India (IN), Indonesia (ID), Singapore (SG)

COCA vs Other Cards

| Feature | COCA | Crypto.com | Plutus | KAST |

|---|---|---|---|---|

| Max Cashback | 8% (Elite) | 8% CRO (Prime) | 9% PLU | 3% USD + 2% Points (Luxe, $50K/mo cap) |

| Free Tier Rate | 1% | 0% | 3% | 1.5% USD ($2K/mo cap) |

| FX Fee | 0% | 0-2% | 0% | 0.5-1.75% |

| Token Requirement | Stake (30-day cooldown) | Stake (180 days) | Stacking | None |

| APY on Balance | 6% (Morpho) | 0% | 0% | 0% |

| Sub Rebates | 50% (4 categories, by tier) | 100% (select) | 100% (select) | None |

| IBAN/Banking | Yes (SEPA) | Yes | No | No |

| Custody | Non-custodial (Privy) | Custodial | Non-custodial | Custodial |

| Countries | 70 | 70+ | 31 (EEA/UK) | 170+ |

COCA wins on: High cashback (up to 8% within monthly allowance) with 0% FX fees, 6% APY on balances (unique among card programs), personal IBAN/SEPA banking, category-based subscription rebates (up to 4 categories at Elite), and non-custodial architecture with audited security.

COCA loses on: $COCA is a small-cap token (higher token risk than CRO or PLU), staked tokens are locked with 30-day cooldown (not instantly liquid like claimed previously), no native App Store listing yet, newer platform with shorter track record, monthly allowance caps limit cashback at higher spend levels, and Privy key recovery depends on COCA infrastructure (not fully self-sovereign like Gnosis Pay).

Competitor Comparison

- vs Crypto.com: Crypto.com offers up to 8% CRO with 180-day staking lockup. COCA offers up to 8% within monthly allowance with staking (30-day cooldown to unstake). COCA wins on higher guaranteed APY and 0% FX. Crypto.com wins on track record, 100% subscription rebates, airport lounges, and native app.

- vs Plutus: Plutus offers 3-9% PLU with subscription (GBP 6.99-19.99/month, no free tier) and 2.5% FX on non-domestic (EEA/UK only). COCA offers 1-8% within monthly allowance with 0% FX across 70 countries. COCA wins on FX, availability, IBAN, APY, and no subscription fees. Plutus wins on max cashback rate for domestic perk optimizers.

- vs KAST: KAST offers 1.5% USD cashback on the first $2,000/month at the free Standard tier with no token requirement and 0.5-1.75% FX. Premium and Luxe tiers add KAST Points (1% and 2%) and higher caps but require paid card costs. COCA offers 1-8% within allowance with $COCA staking and 0% FX. KAST wins on zero token requirement and 170+ countries. COCA wins on max cashback, 0% FX, APY, subscription rebates, IBAN, and uncapped allowance at higher tiers.

- vs Gnosis Pay: Gnosis Pay offers 1-5% GNO with true Safe self-custody and 0% FX. COCA offers 1-8% within allowance with Privy non-custodial and 0% FX. Gnosis wins on true seed-phrase self-custody. COCA wins on higher max cashback (8%), APY, subscription rebates, and IBAN.

Who Should Use COCA?

Ideal user profile:

- Wants a crypto-native bank replacement (card + IBAN + yield + swaps in one app)

- Values non-custodial control with bank-grade UX (no seed phrase hassle)

- Holds stablecoin balances and wants 6% APY alongside card rewards

- Uses eligible subscription services (Netflix, ChatGPT, Spotify, Amazon depending on tier)

- Spends in any currency with 0% FX fees

- Lives in one of the 70 supported countries

Who should avoid:

- Risk-averse users uncomfortable with small-cap $COCA token exposure at higher tiers

- Users who want established, battle-tested platforms - use Crypto.com (8+ years) or Plutus (6+ years)

- Users who need true seed-phrase self-custody - use Gnosis Pay (Safe wallet) or Ledger CL

- Users in countries outside the 70 supported markets

Final take: COCA remains one of the most feature-dense crypto cards available in 2026. Up to 8% cashback (within monthly allowance) + 0% FX + 6% APY + subscription rebates + IBAN banking + non-custodial wallet is unmatched by any single competitor. At Starter tier (zero staking), you get 1% cashback, 0% FX, and 6% APY on up to $5K - competitive with most cards. At Elite tier, 8% cashback on first $10,000/mo delivers the full 8% net on all spending within the allowance. Above the allowance, all tiers drop to 1%.

The entire risk-reward calculation hinges on $COCA token exposure: stake zero tokens at Starter and get solid baseline features, or stake $COCA (locked during membership, 30-day cooldown to unstake) and unlock one of the strongest reward packages in crypto.

Is COCA Safe?

Card issuer: Wirex Limited (FCA-regulated, UK) and UAB Wirex (licensed, EEA). Prepaid card program with Visa network. PCI DSS and ISO compliant. 3DS for online transactions. Freeze/unfreeze in-app.

Wallet security: Privy non-custodial infrastructure. SOC 2 Type I and Type II certified. Third-party audits by Cure53, Zellic, and Doyensec. Bug bounty program. Private key export available (irreversible - you lose COCA wallet access).

Self-banking model: COCA cannot access, freeze, or move your funds. Each card transaction requires your wallet's authorization for the specific amount. This is fundamentally different from custodial exchange cards (Crypto.com, Bybit) where the exchange holds your balance.

What is NOT protected:

- $COCA token value (small-cap, volatile)

- APY rates (DeFi market-dependent, adjusted to stay sustainable)

- Subscription rebates (subject to COCA's partnerships)

- Platform risk: if COCA shuts down, Privy key reconstruction may be complex (you can export private keys as a precaution)

COCA stability indicators (reviewing as of 2026):

- Card issued through Wirex

- No App Store native app listing yet (web/PWA)

Is COCA a Scam?

COCA is not a scam. For a "do everything" crypto app, the supporting stack is unusually traceable - every moving part is delegated to a named, verifiable third party:

1. Card issuer is a regulated card program operator. The card is issued by Wirex Limited (FCA-regulated, UK) and UAB Wirex (licensed EEA). These are real, regulated card program operators running on the actual Visa network, with PCI DSS and ISO compliance and 3DS for online transactions. COCA is the product layer on top; Wirex handles the card rails.

2. Wallet layer is delegated to Privy with public audits. The non-custodial smart contract wallet runs on Privy (ERC-4337 / EIP-7702). Privy holds SOC 2 Type I and Type II certifications, has been audited by Cure53, Zellic, and Doyensec, and runs a bug bounty program. Private key export is available (irreversible) if you want to leave COCA entirely.

3. Yield comes from on-chain DeFi, not a promotional rate. The 6% APY on stablecoin balances is generated by Morpho on-chain lending markets with risk management from Gauntlet. The yield reflects borrowing demand on the protocol, not COCA topping up the rate. Both are established DeFi infrastructure providers you can verify independently.

4. Self-banking means COCA cannot touch your funds. Card payments use authorization-based spending: each transaction approves only the specific amount for that specific merchant. COCA cannot freeze or move your balance. This is fundamentally different from exchange cards like Crypto.com or Bybit where the operator holds your balance outright.

5. The country footprint is fully listed. All 70 supported countries are enumerated by region (UK/Europe, APAC, MEA, LATAM). Scam operators typically claim "global" coverage without specifics.

6. Fees, limits, and tiers are fully specified. The full fee schedule, purchase limits, six-tier staking structure, and allowance caps are all published in tables above. The key scam-check detail is that every tier drops to 1% cashback above its monthly allowance, and that drop-off is stated openly rather than hidden behind the headline 8% rate.

What to be aware of

- $COCA is a small-cap token. Maximum benefits require staking up to 30,000 $COCA for the Elite tier. $COCA trades on smaller venues (MEXC, BitMart, DEXes) and carries real token price risk. If $COCA drops 50%, so does the effective value of your stake and any unsold $COCA rewards.

- Staked tokens are locked during membership with a 30-day cooldown to unstake. This contradicts any framing that suggests the stake is instantly liquid. Plan around the lockup before committing capital you might need.

- Monthly allowance caps shape the real rate. The headline 8% Elite cashback applies only to the first $10,000/month. Every dollar above the allowance earns 1% regardless of tier. Heavy spenders do not get the headline rate on all spend.

- Privy key recovery is not the same as seed-phrase self-custody. Your funds are non-custodial, but the recovery model depends on COCA infrastructure for the biometric/email flow. If you want full seed-phrase self-sovereignty, Gnosis Pay on Safe is closer to the pure version. You can export private keys from COCA as a precaution, but doing so is an irreversible step.

- Newer platform, shorter track record. COCA does not have the multi-year live history of Crypto.com (8+ years) or Plutus (6+ years). It is building real infrastructure quickly, but it has not yet been stress-tested across a full market cycle.

- No native App Store listing. COCA runs as a web/PWA product rather than a native mobile app. Not a scam signal in itself, but it means you cannot check community reviews or install counts the same way you would for a native app.

- Yield and subscription rebates are product features, not guarantees. Morpho APY is market-driven and will move up or down as lending demand changes. Subscription rebates depend on partnerships COCA can add or remove. Treat both as variable.

SpendNode Verified: The editorial team reviewed COCA's issuer identity, product terms, and live card flow per our methodology. Verification is not an endorsement or guarantee.

Sources and Verification

Written by Aleksandar Dukic

Frequently Asked Questions

Is COCA crypto card available in the United States?

No. COCA crypto card is not available in the United States.

How does $COCA staking work?

Yes, tiers above Starter require staking $COCA tokens. Staked tokens are locked for the duration of your tier membership. To unstake, you must cancel your tier (which downgrades you to Starter), then wait 30 days before claiming your tokens. No partial unstaking is allowed. Starter tier requires zero staking.

What are the 6 tiers and their requirements?

Starter (0 COCA, 1% cashback), Standard (stake 300 COCA, 3%, $1K/mo allowance), Standard+ (stake 1K COCA, 4%, $1.75K/mo), Premium (stake 3K COCA, 5%, $2.5K/mo), Premium+ (stake 10K COCA, 6%, $5K/mo), Elite (stake 30K COCA, 8%, $10K/mo). After the monthly allowance, all purchases earn 1%. All tiers earn 6% APY up to tier cap (2% above).

Who issues the COCA card?

The COCA Visa card is issued in partnership with Wirex. Wirex Limited is FCA-regulated in the UK; UAB Wirex is licensed in the EEA.

Where can I buy $COCA?

Available on MEXC, BitMart, and decentralized exchanges like Uniswap and 1inch via WalletConnect in the COCA app.

How does the APY work?

You earn 6% APY on your stablecoin card balance up to your tier cap (Starter $5K, Standard $50K, Standard+ $250K, Premium $500K, Premium+/Elite unlimited), and 2% APY on any amount above the cap. Interest is calculated on your minimum monthly card balance (minimum $1 required) and paid by the 10th of the following month in stablecoins. Yield is generated via Morpho lending markets with Gauntlet risk management.

Is there an IBAN?

Yes. COCA provides a personal IBAN for SEPA bank transfers in EUR. You can receive salary, send/receive money, and top up your card balance via bank transfer, card top-up, or stablecoins.

Is the COCA Card a credit card?

No. The COCA Card is a non-custodial Visa debit card, not a credit card. You spend from your smart wallet balance - there is no credit line, no APR, and no credit check. For crypto-backed credit card options, see our reviews of Gemini, ether.fi, Nexo, and Avici.

Does the COCA Card have a promo code or discount?

Yes. The COCA referral code is T8kJtJtodTb. Sign up through SpendNode's COCA referral link on our promo codes page, that code is automatically applied and you unlock a $10 bonus after ordering a COCA card and spending $100 on it.

User Reviews

Reviews are moderated and may take a moment to appear.

Latest Page Changes to the COCA Review

- Added COCA's 3.0 deposit-address reminder warning users to copy a fresh crypto deposit address before sending funds

App Store (31 ratings)

Source: Apple App Store - Updated Jul 2026