Tuyo Crypto Cards Review 2026

Compare Tuyo crypto cards and review issuer terms, fees, and availability.

Prefer mobile? Scan to continue

Opens the mobile signup with your SpendNode link, code sulik.

SpendNode Rating for Tuyo

Tuyo pairs a clean self-custody model with a real token-rewards commitment to users. Rain as card issuer and Bridge as fiat rails are battle-tested infrastructure, and the multi-product app shows ambition beyond just a card.

The lineup is narrow today (one virtual card, physical coming soon) and the company is young enough that the operational track record is short. On fee transparency and trust positioning, Tuyo lands near the top of the new entrants. The 2026 TGE with 20% of supply for users is the most differentiated feature.

Issuer Snapshot

Editorial vendor score stays separate from user reviews. Methodology

Product Quality

3.8

Trust & Custody

4.5

Fee Transparency

4.5

Operational Reliability

3.9

Market Relevance

4.1

On This Page

Tuyo is a US-based fintech that issues a self-custodial Visa debit card for spending USDC on Base directly from a user-controlled wallet. The card has no annual fee, charges 0% on USD transactions and up to 1% on other currencies, supports Apple Pay and Google Pay, and earns TUYOs points toward a 2026 token generation event with 20% of supply reserved for users and community.

What Is Tuyo?

SpendNode app screenshot

Tuyo Card - Free, self-custodial Visa. Spend USDC from your own wallet at 40M+ Apple Pay/Google Pay terminals and 175M+ Visa locations worldwide. Stay in full control of your USDC until it is spent.

Tuyo is a self-custodial Visa debit card for USDC, not an exchange-linked card. Your USDC sits in a non-custodial wallet on Base that you control with a private key; Tuyo can only pull up to your activated daily limit when you tap. Everything else stays in your wallet.

That custody model is the same architecture used by Gnosis Pay (Safe multi-sig on Gnosis Chain) and Ready's Argent smart account on Starknet (card program unavailable), but Tuyo runs on Base, uses Rain as issuer, and adds two distinctive features that neither design offers: a TUYOs token rewards program with a 2026 TGE, and a discretionary "Buy Now, Pay Maybe" mechanic that can wipe out the cost of individual transactions.

The card itself is free. No issuance fee, no monthly fee, no annual fee. USD transactions are 0%. Non-USD transactions carry up to a 1% FX spread, which is competitive but not the cleanest in market; Gnosis Pay has no issuer FX markup. Apple Pay and Google Pay are supported, and the card is virtual-only for now with a physical card "coming soon" per the Tuyo app.

The Product Ecosystem

Tuyo is not just a card. The app bundles four products into one self-custodial wallet:

- Tuyo Card - The Visa debit covered in detail on this page. Free, USDC on Base, self-custodial.

- Tuyo Earn - Yield vaults that route idle USDC, EURC, or BTC into third-party DeFi protocols (Morpho and others). Tuyo Earn balance can optionally be flagged as spendable from the card via a setting toggle.

- Tuyo Trade - Token trading across 5 networks with 15,000+ tokens listed.

- Tuyo Transfer - Free global transfers and multi-currency virtual accounts via Bridge.xyz. USD/MXN/EUR can be received by wire, ACH, SEPA, or SPEI and auto-converted to USDC or EURC into your wallet.

Card spend earns TUYOs across the whole ecosystem, so the card is also the on-ramp to the points program rather than a standalone product.

Available crypto cards by Tuyo in August 2026

1. Tuyo Card

Free Self-Custodial Visa for USDC - 0% on USD, TUYOs Rewards Built-In

Tuyo Card Referral Code sulik: Get $10

Use Tuyo Card referral code sulik by signing up through SpendNode's Tuyo referral link. New users receive $10 after making at least five Tuyo Card payments of $5 or more on five different days.

How to Use Tuyo Referral Code sulik

- Open SpendNode's Tuyo referral link so code sulik is attached to your signup.

- Create your Tuyo account, complete identity verification, and activate the free virtual Tuyo Card.

- Make at least one card payment of $5 or more on five separate days. Five payments made on the same day do not qualify.

- Once all five qualifying payments are complete, you become eligible for the $10 referral reward.

How Tuyo Card Spending Works

The transaction flow is the same in spirit as any self-custodial card, but the specifics matter. Here is what happens when you tap.

Step 1. You load USDC into your Tuyo wallet. You can deposit USDC (or any token) on Ethereum, Base, Arbitrum, Optimism, or Polygon, and Tuyo converts to Base USDC for free inside the app. Funds remain in a non-custodial wallet whose private key is on your device (backed up to iCloud or Google for recovery).

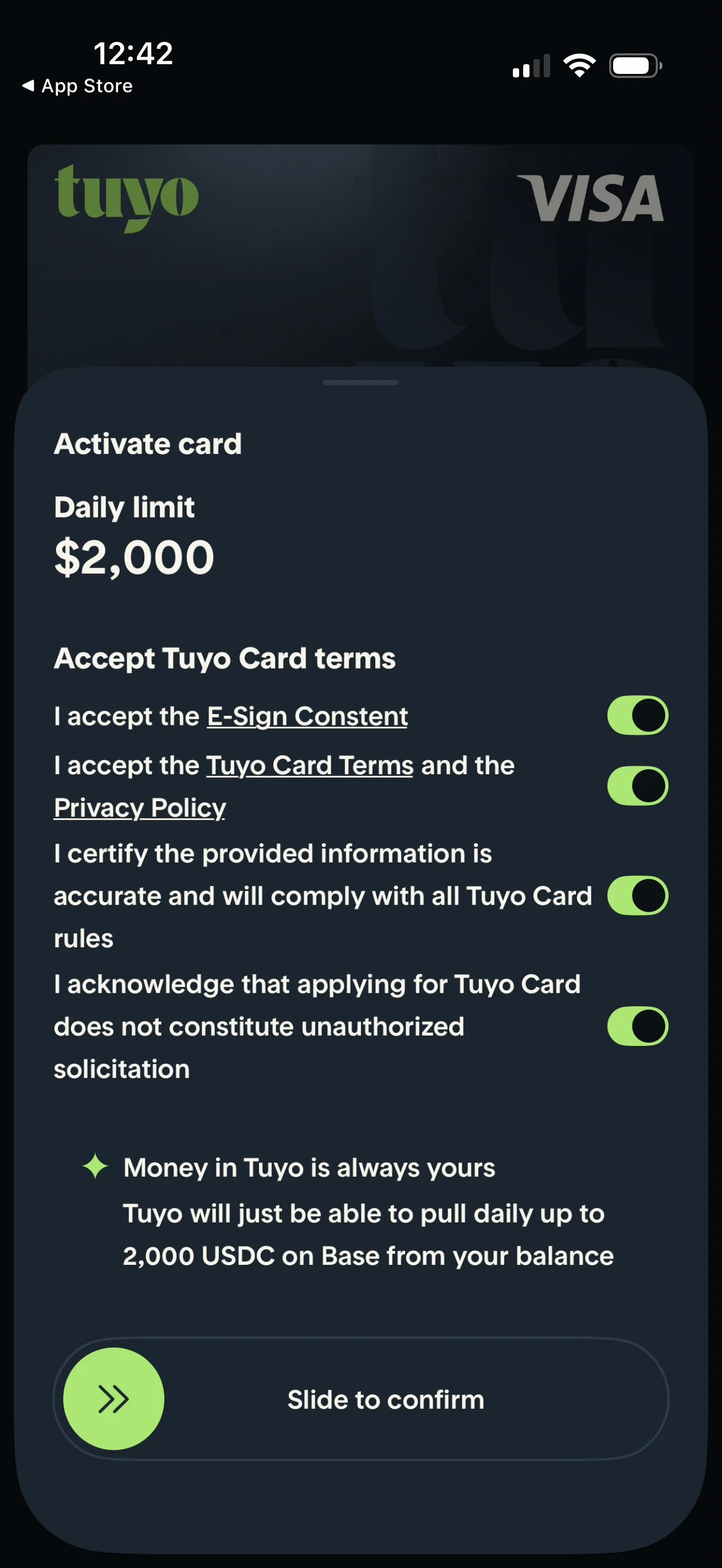

Step 2. At card activation you accept a daily debit authorization. The first authorization is for $2,000 per day. As your account history matures, Tuyo can raise this limit up to $10,000 per day. The activation modal phrases it directly: "Money in Tuyo is always yours. Tuyo will just be able to pull daily up to 2,000 USDC on Base from your balance."

Step 3. You tap your card (or your phone via Apple Pay or Google Pay) at any Visa merchant. The Tuyo back end debits the equivalent USDC from your Base balance for the dollar amount of the purchase. The merchant receives fiat over standard Visa rails.

Step 4. Tuyo applies the FX spread if the merchant currency is not USD: up to 1% on the converted amount. USD purchases incur no spread.

Step 5. If "Buy Now, Pay Maybe" triggers on the transaction, Tuyo may not debit some or all of the authorization amount. You only see this after the fact when the transaction settles. There is no opt-in and no notification before the fact.

Step 6. Card spend accrues TUYOs at the current season's rate. TUYOs are recorded in the app and have no spendable value until the token generation event.

Fees and Rates

| Fee | Amount | Notes |

|---|---|---|

| Issuance | $0 | Free |

| Monthly fee | $0 | Free |

| Annual fee | $0 | Free |

| USD transactions | 0% | No spread, no markup |

| Non-USD transactions | Up to 1% FX spread | Includes Visa network rate |

| USDC conversion (other chains to Base) | Free | Ethereum, Base, Arbitrum, Optimism, Polygon |

| ATM access | Pending physical card launch | Not currently available |

| Daily spending limit | $2,000 at activation, up to $10,000 with usage | Tuyo can only debit up to this amount per day |

This is among the cleanest fee schedules for USD spenders on a globally available self-custodial Visa. ether.fi Core adds a 0-0.5% FX margin on cross-border purchases, while Gnosis Pay (EEA/UK only, EUR-settled) has no issuer markup on its base currency. Ready's former Lite and Metal tiers are retained in the historical comparison below but are unavailable.

Advertised vs Reality: The FX Truth

The "up to 1%" FX language matters. Tuyo does not claim 0% FX globally; the card is positioned as 0% on USD with a small spread on everything else. For US-based USD spending, the effective rate is zero. For a European user spending in EUR, the effective rate is up to 1%, which is competitive with debit but not better than zero-FX alternatives in the EEA.

For comparison at $1,000 in EUR spending:

- Tuyo: up to $10 (1% spread)

- Ready Metal (unavailable): $0 historical FX cost (plus 120 USDC/year fee)

- ether.fi Core: $0 (0% FX on EUR, no fee)

- Gnosis Pay (EURe): $0 FX issuer markup, but only available in EEA/UK and EUR-settled

- Traditional bank card: typically $25-35 (2.5-3.5%)

Tuyo wins decisively against traditional banks on FX. On EUR it trails ether.fi and Gnosis Pay, but it skips ether.fi's ETH-collateral lock and works globally. Against Gnosis Pay, Tuyo trades slightly worse EUR FX for free entry and a TUYOs upside.

Custody, Security, and Rain as Issuer

SpendNode app screenshot

The self-custody architecture in one screen. At card activation, you authorize Tuyo to pull up to a fixed daily limit from your USDC on Base balance. The rest of your wallet is never accessible to the card processor.

Tuyo is non-custodial from the ground up. The Tuyo Terms of Service state plainly: "The Service is a purely non-custodial application, meaning we do not ever have custody, possession, or control of your digital assets at any time." Your private key is stored on your device with optional iCloud or Google Drive backup. If Tuyo as a company disappears tomorrow, your USDC stays on Base in your wallet and you can sweep it from any compatible wallet by importing the seed phrase.

The card issuance partner is Signify Holdings, Inc., trading as Rain. This is the same back end used by Avici, which means the card mechanics (BIN, authorization flow, freeze controls, PIN management) are proven in production rather than a Tuyo-built card stack. Rain handles the regulated card-issuing relationships with banking partners.

The fiat side is run by Bridge Ventures, Inc. (Bridge.xyz), a regulated money transmitter in the United States and compliant with EEA regulations. Bridge runs the virtual account numbers that let you receive USD by wire or ACH, MXN by SPEI, or EUR by SEPA, and auto-converts incoming fiat to USDC or EURC into your Tuyo wallet.

This split-stack approach (Tuyo for wallet and app, Rain for card issuance, Bridge for fiat) is the modern self-custody-card playbook. It means Tuyo Inc. itself is not a money transmitter, bank, or asset custodian, which simplifies the regulatory surface and explains why the card can launch globally faster than a traditional bank card.

Is Tuyo Safe?

A self-custodial card's bankruptcy story is structurally different from a custodial card's. Here is the actual exposure analysis.

Your USDC on Base. Safe. The wallet is non-custodial. If Tuyo Inc. shuts down, your private key still controls your USDC on Base. You can import the seed phrase into Rabby, MetaMask, or any compatible Base wallet and move the funds out. There is no court process and no creditor queue.

Your TUYOs points. At risk. TUYOs are tracked internally by Tuyo and have no on-chain representation until the TGE. If Tuyo shuts down before the TGE, accrued TUYOs probably vanish. This is the speculative leg of the program and explicitly disclosed in the rewards terms.

Your virtual accounts at Bridge. Bridge is a separate regulated money transmitter. If Tuyo shuts down but Bridge survives, your virtual account relationship is with Bridge directly. If Bridge shuts down, customer funds would be subject to its money transmitter regulatory framework rather than Tuyo's. Bridge is not a bank, so the funds in virtual accounts are not FDIC-insured; they are held under money transmitter customer fund protection rules.

Card spending capability. Disabled. The card uses Tuyo's authorization system to debit your wallet. If Tuyo's back end is offline, the card declines. Your funds are safe, but you cannot spend with the Tuyo Card until you move to another wallet or card.

For most users, the practical implication is simple: USDC custody is preserved, but card functionality and TUYOs upside both depend on Tuyo as a company surviving to the TGE and beyond.

Is Tuyo a Scam?

-

Tuyo Inc. is a Delaware-incorporated US company with published support and legal contact details (support@tuyo.com, 302-219-4850, 1317 Edgewater Dr #1739, Orlando, Florida 32804), a public Terms of Service, and California-specific consumer rights disclosures.

-

Cards are issued by Signify Holdings (Rain), the same regulated card issuer behind Avici. Rain handles the licensed banking relationships and KYC/AML compliance; Tuyo Inc. is not itself a card issuer, bank, or money transmitter.

-

Fiat services run through Bridge Ventures (Bridge.xyz), described in Tuyo's own Terms of Service as "a licensed and regulated money transmitter in the United States and compliant with relevant regulations in the U.S. and the European Economic Area." Bridge handles virtual account numbers and stablecoin conversions.

-

The non-custodial architecture is contractual and verifiable. Tuyo's Terms state directly: "The Service is a purely non-custodial application, meaning we do not ever have custody, possession, or control of your digital assets at any time." USDC sits on Base in a wallet whose private key is stored on the user's device. Tuyo can only debit up to the activated daily limit.

-

Tuyo has a public user base of 50,000+ per its homepage and runs a structured TUYOs rewards program with a published seasons schedule (Pioneers, Early Adopters, FOMO, Stacking Season) and a written 20% supply commitment to users and community at TGE.

-

The Buy Now, Pay Maybe terms are unusually direct about what BNPM is and is not. The Terms explicitly state BNPM is not a sweepstakes, lottery, prize, or rewards program, that there is no opt-in or guarantee, and that Tuyo can modify or exclude it at any time. Most marketing-heavy vendors would soften that language. Tuyo did not.

The TUYOs Rewards Program

TUYOs are points earned across Tuyo's product surface and are the most distinctive thing about the card economically. Card spend earns TUYOs at the current season's rate, with multipliers stepping down each season. Trading and Earn yields also accrue TUYOs, as do referrals (20% of a friend's TUYOs reward).

Token generation event. Tuyo has publicly committed to a TGE in 2026 with 20% of token supply reserved for users and the community. This is a stronger commitment than most "points might become tokens" programs, which usually keep the percentage vague or condition the TGE on internal milestones.

Seasons structure. The program has progressed through four seasons:

- Season 0: Pioneers (retroactive + first 48 hours after launch, ended Nov 1, 2025)

- Season 1: Early Adopters (Nov 1 - Dec 11, 2025)

- Season 2: FOMO (Dec 11, 2025 - Jan 22, 2026)

- Season 3: Stacking Season (Jan 22, 2026 - TGE 2026)

Multipliers are highest in earlier seasons. Joining today puts you in Season 3, which is the longest single season and likely the lowest multiplier per TUYO compared to Pioneers, but covers the longest TGE-eligibility window.

TUYOs are speculative. The Tuyo Terms of Service describe them as "intended solely for internal tracking, testing, and community engagement purposes" with "no monetary significance." Treat the 20% reservation as a credible signal of intent, but plan around card economics first and TUYOs as upside.

What Is Buy Now, Pay Maybe?

BNPM is the most marketing-forward feature on the Tuyo site, headlined as "the card that might not charge you." The legal reality is more bounded. From the Terms of Service:

- BNPM is a discretionary processing-discount feature. Tuyo, in its sole discretion, may elect not to debit some or all of a Tuyo Card transaction from your wallet.

- The merchant always receives the full transaction amount. Tuyo absorbs the difference.

- BNPM is not a sweepstakes, lottery, prize, contest, raffle, game of chance, or rewards program. There is no opt-in, no enrollment, no minimum spend, and no action that qualifies you for or increases the likelihood of BNPM.

- Tuyo can exclude or restrict BNPM by merchant, MCC, or transaction type, and can change the rules at any time without notice.

- BNPM is not available in any jurisdictions where prohibited by law, including some US states and territories.

What that means in practice: BNPM is a marketing-funded discount that may or may not apply to any given transaction. Treat it as a possible upside on top of normal card spending, not as a guaranteed reward rate.

Real User Scenarios

Maria, freelance designer in Mexico City spending $1,500/month in USDC

Maria gets paid in USDC by clients in the US and used to convert through a Mexican exchange to MXN, paying 2-3% on each conversion. She moves to Tuyo and receives USDC directly into her self-custodial wallet via Bridge's virtual SPEI account. She spends the USDC on the card daily.

At $1,500/month, with roughly 80% USD-denominated purchases (online subscriptions, US-based SaaS, USD-priced services) and 20% MXN spending (groceries, transit), Maria's effective fee rate is approximately 0.2% (1% on the 20% non-USD slice). Annual fee cost: roughly $36/year compared to $450-540/year on a 2.5-3% bank card. She also accrues TUYOs across her $18,000 annual spend, which could be a meaningful airdrop position depending on TGE valuation.

The trade-off: no native MXN settlement, so her FX exposure is to Visa's USD-to-MXN conversion plus Tuyo's 1% spread. Acceptable at her volume, less so if she primarily spent in MXN.

James, US-based software engineer spending $2,500/month on USDC

James already holds USDC in a Coinbase Wallet and is comfortable with self-custody. He moves to Tuyo for the 0% USD experience and the TGE upside. His spending is roughly 95% domestic USD (groceries, dining, subscriptions, travel within the US) and 5% on international online purchases.

At $2,500/month, James pays effectively zero FX on the USD slice and approximately 1% on the $1,500/year of non-USD spending, for an annual fee cost of roughly $15. He earns TUYOs on the full $30K of annual spend. Compared to a 2% cashback card on the same volume ($600/year), James is giving up $585/year of guaranteed cashback in exchange for self-custody and a speculative airdrop position. The TGE would need to deliver at least $585 in token value at vesting to break even on the trade.

Sofia, EU-based crypto user spending $3,000/month, mostly in EUR

Sofia is based in Berlin and spends primarily in EUR. She loads her Tuyo wallet with USDC via SEPA into Bridge (which converts EUR to EURC, though Tuyo's card spends from USDC on Base specifically) or from existing on-chain USDC.

Her usage exposes the FX trade-off: at 100% EUR-denominated spending, Sofia pays up to 1% on every transaction, or roughly $360/year on $36K of spending. For comparison, Gnosis Pay settles in EURe (a Gnosis-Chain EUR stablecoin) at 0% issuer markup and is the better fit for EUR-primary spenders. Tuyo makes more sense for Sofia only if the TGE upside outweighs the $360/year FX delta.

Who Should Use Tuyo

Use Tuyo if:

- You spend primarily in USD and want a free, self-custodial alternative to exchange cards

- You hold USDC on Base or any major L2 and want to spend it without bridging or selling

- You want exposure to a planned 2026 token airdrop with 20% of supply reserved for users

- You already use Tuyo Earn, Trade, or Transfer and want a card that complements that stack

- You are comfortable with self-custody and seed-phrase management

Avoid Tuyo if:

- You spend primarily in EUR, GBP, or another non-USD currency (use Gnosis Pay instead for no issuer FX markup in EEA/UK)

- You need ATM access today (no physical card yet, no current ATM functionality)

- You are based in the United Kingdom (services not intended for UK persons)

- You prefer cash cashback over speculative token rewards

- You want to spend BTC, ETH, or other non-stablecoin crypto directly

Verdict

Tuyo lands as one of the cleanest self-custodial Visa cards globally, with a fee schedule that beats every custodial alternative on USD and matches the strongest self-custody competitors on everything except non-USD FX. The TUYOs program with a 2026 TGE and 20% supply reservation for users is the most differentiating feature; it converts everyday USDC spending into a position in an upcoming token launch.

The two structural limitations are the non-USD spread and the lack of a physical card. Both are acceptable for the target user (USD-spending stablecoin holders who want a virtual card on Apple Pay or Google Pay), and the physical card is on the public roadmap. For everyone else, the competitive set is well-defined: Gnosis Pay for EUR spenders in EEA/UK, ether.fi Core for borrow-against-staked-ETH spending with no taxable disposal, and COCA for the highest stablecoin cashback rate with staking.

Fees and ROI Framework

The Tuyo Card has no annual fee, so the break-even calculation is on FX rather than fee recovery. The real test is whether the 1% FX cost on your non-USD slice eats into your TUYOs upside enough to matter.

At three spending levels with 50% USD and 50% non-USD purchases:

- $1,000/month: $60/year in FX cost. TUYOs accrue on $12K of spend.

- $2,500/month: $150/year in FX cost. TUYOs accrue on $30K of spend.

- $5,000/month: $300/year in FX cost. TUYOs accrue on $60K of spend.

The opportunity cost against a 2% cashback card is material for high spenders: at $5K/month, you forgo $1,200/year in guaranteed cashback for self-custody plus a TUYOs position. The TGE needs to deliver enough token value to outpace that gap, which is a bet on an unannounced valuation.

For 100% USD spenders, FX cost is zero and the only opportunity cost is the cashback you skip. This is where Tuyo is most competitive: the card costs effectively nothing to use, and TUYOs are pure upside.

Competitor Comparison

- vs Gnosis Pay: Gnosis Pay wins on EUR-native spending in EEA/UK (0% FX, EURe settlement, up to 5% GNO cashback with token holdings). Tuyo wins on USD spending, global availability outside UK, and TGE upside. Different geographies.

- vs Ready Metal (unavailable): Ready Metal formerly had 0% FX and 3% STRK cashback for 120 USDC/year in EEA/UK. Tuyo remains available, is free, and has broader coverage outside the UK.

- vs ether.fi Core: ether.fi wins on 3% ETH cashback and borrow-against-staked-ETH spending (no taxable disposal). Tuyo wins on USD fee structure and TGE upside. Tax-conscious ETH holders prefer ether.fi; USDC spenders prefer Tuyo.

- vs COCA: COCA wins on cashback rate (up to 8% USDC at Elite with $COCA staking) and yield (6% APY on USDC). Tuyo wins on simplicity and no token to buy upfront. Mid-volume USDC spenders should compare COCA Standard against Tuyo case-by-case.

- vs Avici: Both use Rain as issuer, but Avici is a secured credit card (you post crypto collateral and spend a USD credit line) while Tuyo is a debit card that pulls from your USDC balance. Avici fits users who want to avoid taxable disposals; Tuyo fits users who just want to spend stablecoins.

Availability and Compliance Notes

Tuyo is available globally except to UK residents and OFAC-sanctioned jurisdictions. Card issuance is handled by Signify Holdings (Rain) under licensed banking partners. Fiat services run through Bridge Ventures (Bridge.xyz), a regulated US money transmitter compliant with relevant EEA regulations. KYC is required for card issuance and is run through Tuyo's app at signup.

Buy Now Pay Maybe is unavailable in restricted US states and territories where the program is prohibited by law. The TUYOs rewards program has no monetary value until TGE and Tuyo can modify or terminate the program at any time.

Sources

Countries and Availability

Tuyo is available in 95 countries as of August 2026. We count a country here when at least one active Tuyo card variant lists it, so individual product pages may be narrower.

Available Regions

Africa

Cameroon (CM), Cote d'Ivoire (CI), Egypt (EG), Ethiopia (ET), Ghana (GH), Kenya (KE), Morocco (MA), Mozambique (MZ), Nigeria (NG), Rwanda (RW), Senegal (SN), South Africa (ZA), Tanzania (TZ), Tunisia (TN), Uganda (UG)

Americas

Argentina (AR), Bolivia (BO), Brazil (BR), Canada (CA), Chile (CL), Colombia (CO), Costa Rica (CR), Dominican Republic (DO), Ecuador (EC), El Salvador (SV), Guatemala (GT), Jamaica (JM), Mexico (MX), Panama (PA), Paraguay (PY), Peru (PE), Puerto Rico (PR), Trinidad and Tobago (TT), United States (US), Uruguay (UY)

Asia

Bahrain (BH), Cambodia (KH), Georgia (GE), Hong Kong (HK), Indonesia (ID), Japan (JP), Jordan (JO), Kazakhstan (KZ), Kuwait (KW), Malaysia (MY), Mongolia (MN), Oman (OM), Pakistan (PK), Philippines (PH), Qatar (QA), Saudi Arabia (SA), Singapore (SG), South Korea (KR), Sri Lanka (LK), Taiwan (TW), Thailand (TH), United Arab Emirates (AE), Uzbekistan (UZ)

Europe

Albania (AL), Austria (AT), Belgium (BE), Bulgaria (BG), Croatia (HR), Cyprus (CY), Czech Republic (CZ), Denmark (DK), Estonia (EE), Finland (FI), France (FR), Germany (DE), Greece (GR), Hungary (HU), Iceland (IS), Ireland (IE), Italy (IT), Latvia (LV), Lithuania (LT), Luxembourg (LU), Malta (MT), Montenegro (ME), Netherlands (NL), North Macedonia (MK), Norway (NO), Poland (PL), Portugal (PT), Romania (RO), Serbia (RS), Slovakia (SK), Slovenia (SI), Spain (ES), Sweden (SE), Switzerland (CH)

Oceania

Australia (AU), Fiji (FJ), New Zealand (NZ)

Major Restricted Markets

These major markets are not currently listed for this vendor. Confirm eligibility with the issuer before applying, especially where card tiers have different country rules.

Asia

China (CN), India (IN), Turkey (TR)

Europe

United Kingdom (GB)

Written by Aleksandar Dukic

Frequently Asked Questions

Is Tuyo crypto card available in the United States?

Yes. Tuyo crypto card is available in the United States. Some optional features, including Buy Now, Pay Maybe, may be restricted in certain US states and territories.

Is Tuyo a bank?

No. Tuyo Inc. is a financial technology company, not a bank, exchange, or asset custodian. Tuyo provides a self-custodial wallet where you control the private keys. Cards are issued by Signify Holdings (Rain) and fiat rails are operated by Bridge Ventures (Bridge.xyz), a regulated money transmitter in the US and EEA.

How does the TUYOs rewards program work?

TUYOs are points earned for paying with the Tuyo Card, trading on Tuyo, using Tuyo Earn, and referring friends (20% of friend rewards). The program runs in seasons with multipliers that step down after each season. A token generation event (TGE) is planned for 2026, with 20% of the token supply reserved for users and the community at TGE. TUYOs have no fixed conversion rate and Tuyo can modify or terminate the program at any time.

What is Buy Now, Pay Maybe?

Buy Now, Pay Maybe (BNPM) is a discretionary feature where Tuyo may choose not to debit some or all of a Tuyo Card transaction from your wallet. The merchant still receives the full amount; Tuyo absorbs the difference. There is no opt-in, minimum spend, or guarantee any transaction will receive the benefit. BNPM is not available in jurisdictions where it is prohibited by law, including some US states and territories.

Does Tuyo have a referral bonus or promo code?

Yes. Use Tuyo Card referral code sulik by signing up through SpendNode's Tuyo link. New users get $10 after making at least five card payments of $5 or more on five different days.

Is Tuyo Card referral code sulik working in August 2026?

Yes. sulik is a working Tuyo Card referral code as of August 10, 2026 - we re-verify it regularly. Sign up through the referral link, then make at least five card payments of $5 or more on five different days to qualify for the $10 reward.

User Reviews

Reviews are moderated and may take a moment to appear.