Tuyo Card Review 2026

Free self-custodial Visa debit. Spend USDC on Base from your own wallet with 0% USD fees, Apple Pay and Google Pay support, and TUYOs token rewards.

Prefer mobile? Scan to continue

Opens the mobile signup with your SpendNode link, code sulik.

SpendNode Rating for Tuyo Card

Tuyo is genuinely free and genuinely self-custodial, which is rare. The 0% USD fee schedule is the cleanest in market for stablecoin spenders.

Free is not the same as high return. Without a guaranteed cashback rate, net value lags free cards like Jupiter Global, Coinbase, and Bitget at every spending volume. The TUYOs program with a 2026 TGE and 20% supply reserved for users is the upside leg, but treat it as speculative on top of the core card economics. Self-custody architecture lands the trust score near the top of the new entrants.

Also relevant for Stablecoin Spending.

How It Competes

Cost Efficiency

3.6

Product Utility

3.6

Custody & Trust

4.5

Reliability & UX

3.8

Transparency

4.4

APPLE PAY

Verified

GOOGLE PAY

Verified

NO ANNUAL FEE

Verified

Tuyo Card Overview

Free Self-Custodial Visa for USDC - 0% on USD, TUYOs Rewards Built-In

The Tuyo Card is a free self-custodial Visa where Free annual fee meets 0% on USD transactions and TUYOs rewards toward a 2026 token launch. The daily limit starts at $2,000 and increases with account history up to $10,000/day.

Fees & Charges

Annual Fee

Free

FX Fee

1%

ATM Fee

TBD

Requirements

Supported Regions

GLOBAL

Spendable Assets

USDC

On This Page

The Tuyo Card is a self-custodial Visa debit card issued by Signify Holdings (Rain) that lets users spend USDC on Base directly from a non-custodial wallet. It has no annual fee, charges 0% on USD transactions and up to 1% on other currencies, supports Apple Pay and Google Pay, and earns TUYOs points toward a 2026 token generation event.

What Is the Tuyo Card?

The Tuyo Card is a free virtual Visa debit that pulls USDC from your own self-custodial wallet on Base when you tap. The card is issued by Rain (Signify Holdings), the same issuer behind Avici, and the wallet sits inside the Tuyo app with a private key backed up to your device's secure enclave.

The card stands apart on fee schedule, rewards model, and the BNPM discount mechanic. Fees: zero issuance, zero annual, 0% on USD purchases, up to 1% FX on non-USD. Rewards: every dollar of card spend accrues TUYOs toward a 2026 token generation event where 20% of supply is reserved for users and community. BNPM: a discretionary feature where Tuyo may absorb part or all of a transaction at its sole discretion.

If you spend USDC and want a card that does not lock funds with an exchange, the Tuyo Card and ether.fi Core are two available options with broad coverage. Ready Lite formerly offered a similar USDC-funded model in the EEA/UK but is unavailable.

New users can use Tuyo Card referral code sulik through SpendNode's Tuyo link to get $10. Qualification requires five card payments of at least $5, with each payment made on a different day.

Card Specs

Physical and Virtual Cards

- Virtual card: Issued instantly upon KYC approval through the Tuyo app

- Physical card: Coming soon (not yet available as of May 2026)

- Design: Black with green tuyo wordmark in display serif; Visa logo top right

- Card art seen in app: Stylized layered yo glyph in deep green

The virtual card lives in the Tuyo app and can be provisioned to Apple Pay or Google Pay immediately. There is no waiting period for a physical card to ship because there is currently no physical card. Tuyo has signaled a physical card on the roadmap but has not announced a date.

Payment Network

- Network: Visa

- Acceptance: 175M+ Visa merchant locations worldwide (per Tuyo's marketing; the app at one point shows 40M which is closer to Apple Pay and Google Pay tap-eligible terminals specifically)

- Contactless: Yes (via mobile wallet only since no physical card yet)

- Mobile wallets: Apple Pay, Google Pay

- Note on mobile wallets: Apple or Google may decline the add-to-wallet step based on their own device, location, or account risk checks. This is not Tuyo-specific; it applies to most newer card programs.

Security Features

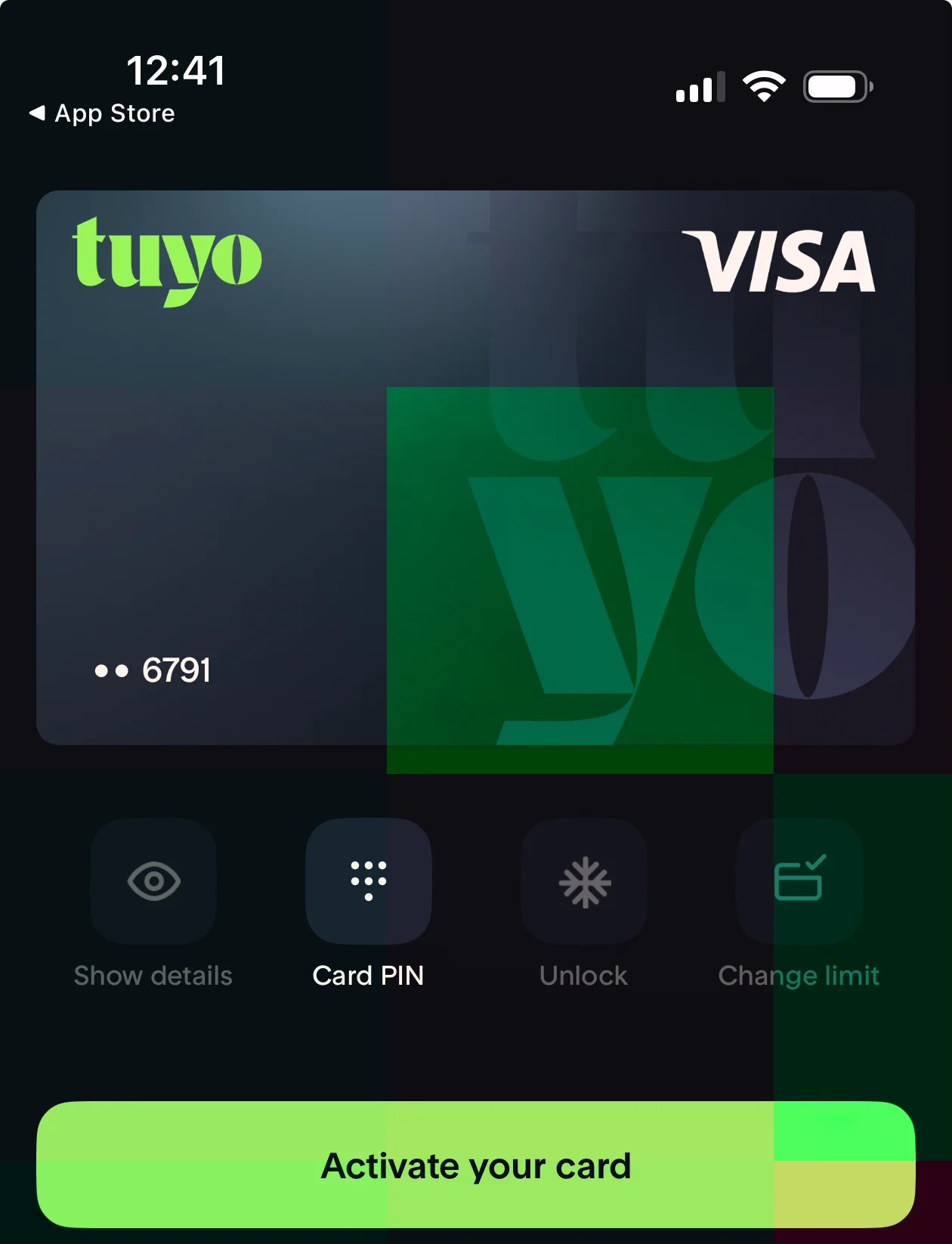

SpendNode app screenshot

Card controls in-app. Show details, set Card PIN, Unlock (freeze and unfreeze), Change limit. Daily limit changes are subject to Tuyo's activation rules.

- Self-custodial wallet: Private key stored on your device with iCloud or Google Drive backup

- Daily debit authorization: Tuyo can only pull up to your activated daily limit from your USDC on Base balance, capping single-day loss exposure

- Card PIN: Settable in-app

- Freeze/unfreeze: Lock/unlock toggle in the Card screen

- Card details visibility: Hidden by default with a Show details action

The "Tuyo can only pull up to your daily limit" architecture is the practical safety net. Even if your phone is compromised and your card is added to a third-party wallet, the attacker is bounded by your daily limit (which starts at $2,000) rather than your full USDC balance.

How Spending Works

Example: $80 dinner in San Francisco

Step 1. You load USDC into your Tuyo wallet. If you have USDC on Ethereum, Arbitrum, Optimism, or Polygon, Tuyo converts to Base USDC for free inside the app. You end up with $200 in your Tuyo wallet.

Step 2. You tap your phone with Apple Pay at the restaurant terminal. Visa sends an authorization request for $80 to Tuyo.

Step 3. Tuyo's back end checks your USDC on Base balance and your activated daily limit. Both are sufficient ($200 balance, $2,000 daily limit). The transaction authorizes.

Step 4. Tuyo debits 80 USDC from your wallet. Since this is a USD-denominated purchase, no FX spread applies. The merchant receives $80 over standard Visa rails.

Step 5. Card spend of $80 accrues TUYOs at the current Season 3 rate. The TUYOs appear in your Rewards screen within the Tuyo app. They have no spendable value until the 2026 TGE.

Step 6. Buy Now Pay Maybe may or may not trigger. If it does, Tuyo absorbs part or all of the $80, and your USDC debit is reduced or zeroed. You only see this when the transaction finalizes.

If the dinner had been EUR 80 in Paris instead: Tuyo would convert at Visa's USD-to-EUR rate plus up to 1% spread, so you would be debited roughly $84-87 in USDC depending on the daily Visa rate.

Fees and Rates

The Tuyo Card has no annual fee, so the standard break-even calculation does not apply. The number that matters is the per-transaction cost.

At $500/month spending (light user, 100% USD)

- Annual spend: $6,000

- Annual fees: $0 (no issuance, no annual, 0% on USD)

- TUYOs accrued on $6,000 of card spend

- Compared to a 2% cashback card: you forgo $120/year in cashback

The Tuyo Card breaks even against any 2% cashback card if the TGE delivers $120 or more in TUYOs token value per $6,000 of accrued points. Whether that happens depends entirely on TGE valuation, which is unannounced.

At $1,500/month spending (regular user, 70% USD / 30% non-USD)

- Annual spend: $18,000

- Annual fees: 1% on $5,400 of non-USD spend = $54

- TUYOs accrued on full $18,000

- Compared to a 4% cashback card (Coinbase): you forgo $720/year in cashback minus $0 fees on Coinbase

At this volume, the FX cost is small but the cashback opportunity cost is material. The Tuyo Card wins if you value the TGE position and self-custody more than $666/year in cashback.

At $3,000/month spending (heavy user, 60% USD / 40% non-USD)

- Annual spend: $36,000

- Annual fees: 1% on $14,400 of non-USD spend = $144

- TUYOs accrued on full $36,000

- Compared to COCA Premium (5% USDC, requires staking 3K COCA): COCA earns $1,800/year vs Tuyo's $0 cashback

At $36K of spend, the cashback gap against COCA is $1,800/year. The Tuyo Card makes sense at this volume only if (a) you do not want to stake COCA tokens, (b) you want simpler tax reporting than ETH-collateralized cards, and (c) the TUYOs TGE could plausibly deliver more than $1,800 in token value.

TUYOs Token Economics

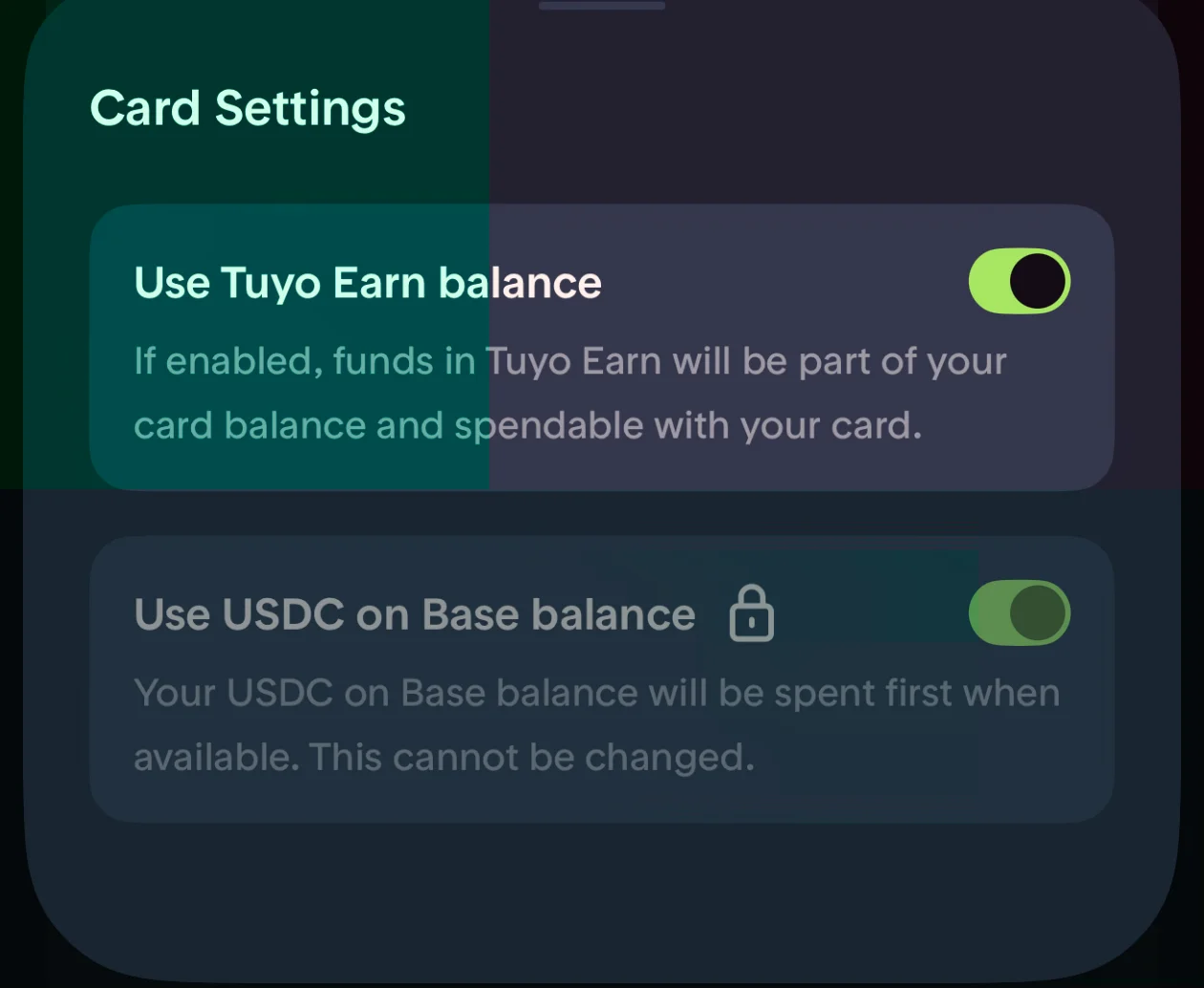

SpendNode app screenshot

Card balance settings. The card always spends USDC on Base first. You can optionally let the card draw from your Tuyo Earn balance too, which means yield-earning funds stay productive until the moment you tap.

TUYOs are the core economic upside of the Tuyo Card, and they are also the speculative leg of the whole product. The framing matters.

What you earn. Every dollar of card spend earns TUYOs at the current season's rate, visible in the Tuyo app. Trading and Earn yields also accrue TUYOs. Referrals earn 20% of a friend's TUYOs rewards.

The seasons schedule.

- Season 0 (Pioneers): retroactive + 48h after launch, ended Nov 1, 2025

- Season 1 (Early Adopters): Nov 1 - Dec 11, 2025

- Season 2 (FOMO): Dec 11, 2025 - Jan 22, 2026

- Season 3 (Stacking Season): Jan 22, 2026 - TGE 2026

Multipliers step down each season. A new user joining today is in Season 3, the longest single season and likely the lowest multiplier per TUYO compared to earlier seasons, but covering the longest eligibility window before TGE.

The TGE commitment. Tuyo has publicly stated a 2026 TGE with 20% of token supply reserved for users and community. This is a stronger written commitment than most points programs, which usually keep the percentage vague.

The risk scenario. TUYOs are explicitly described in Tuyo's Terms of Service as having "no monetary significance" until TGE. The Terms also reserve Tuyo's right to modify, suspend, or terminate the program. The 20% supply reservation is credible, but TGE valuation, vesting schedule, and per-TUYO conversion ratio are all undisclosed. Treat TUYOs as a position in a planned but not-yet-guaranteed token launch.

Break-even math against cashback. A 2% cashback card on $24,000 of annual spend earns $480/year. For Tuyo to match that, the TGE would need to value your annual TUYOs accrual at $480 or more. Without a published conversion ratio, you cannot pre-calculate this; you can only compare it after the TGE.

Buy Now, Pay Maybe

BNPM is the second economic feature unique to Tuyo. The Terms of Service language is precise about what it is and is not.

What it is. A discretionary feature where Tuyo may elect, in its sole discretion, not to debit some or all of a Tuyo Card transaction from your wallet. The merchant always receives the full transaction amount; Tuyo absorbs the difference.

What it is not. Not a sweepstakes, lottery, prize, contest, raffle, game of chance, or rewards program. There is no opt-in, enrollment, minimum spend, or guaranteed application. You cannot do anything to qualify for BNPM or increase the odds it triggers on a given transaction.

Practical reality. BNPM is a marketing-funded discount that may or may not apply to any individual purchase. The safe approach is to ignore it entirely and treat any BNPM trigger as a pleasant surprise.

Restrictions. BNPM is not available in jurisdictions where prohibited by law, including some US states and territories. If you are subject to a restriction, BNPM simply does not apply to your transactions; the rest of the card works normally.

Foreign Exchange: Advertised vs Reality

Tuyo's FX claim is "0% fee on USD transactions, up to 1% FX spread on other currencies." This is unusually clean phrasing because it does not pretend to be 0% globally.

Example: EUR 100 purchase in Berlin

- Visa mid-market rate (illustrative): EUR 1 = USD 1.07

- True conversion: $107

- Tuyo's 1% FX spread cap: +$1.07

- You pay: roughly $108 (depending on the day's Visa rate)

- Effective FX cost: approximately 1%

Comparison at the same EUR 100 purchase:

- Tuyo: ~$108 (1%)

- Ready Metal (unavailable; historical 0% FX): $107 (interbank rate, no issuer spread)

- Gnosis Pay with EURe: $107 (no FX because settled in EURe directly)

- ether.fi Core (0% FX on EUR): $107

- Traditional bank card (2.75% FX): $109.94

Tuyo beats every traditional bank card. It trails available options such as Gnosis Pay and ether.fi on EUR spending, which makes those the better picks for EUR-primary spenders. For USD spenders, Tuyo's 0% USD rate is the lowest-fee option among globally available self-custody Visas.

Limits and Restrictions

Spending Limits

| Period | Limit |

|---|---|

| Daily (at activation) | $2,000 |

| Daily (with usage and account history) | up to $10,000 |

| Per-transaction | Constrained by remaining daily limit |

The daily limit is the activated daily debit authorization. Tuyo can only pull up to this amount from your USDC on Base balance per day, which doubles as a security feature. You can request limit increases as your account matures.

ATM Withdrawals

ATM access is currently unavailable. Tuyo has not yet released a physical card and the FAQ acknowledges this. ATM functionality will likely launch alongside the physical card.

Restricted Spending

- BNPM excludes some merchants, MCCs, or transaction types at Tuyo's discretion

- BNPM unavailable in restricted US states and other jurisdictions

- Cards declined for transactions exceeding daily limit or USDC balance

- Account-level restrictions if KYC verification fails

Is the Tuyo Card Safe?

Your USDC on Base. Safe. The wallet is non-custodial. Tuyo Inc. does not hold your private keys. If Tuyo shuts down tomorrow, you can import your seed phrase into Rabby, MetaMask, or any compatible wallet and move USDC out at will. There is no creditor process and no court queue. This is the structural advantage of the self-custody model.

Your TUYOs. At risk. TUYOs are tracked internally by Tuyo with no on-chain representation until TGE. If Tuyo shuts down before TGE, accrued TUYOs likely vanish. The Terms of Service reserve Tuyo's right to terminate the program. Maximum exposure on TUYOs is the speculative value of points accrued to date.

Your virtual accounts at Bridge. Bridge Ventures is a separately licensed money transmitter. If Tuyo shuts down but Bridge survives, your virtual SEPA/ACH/SPEI accounts are direct customer relationships with Bridge under money transmitter customer fund rules. Not FDIC-insured.

The card itself. Stops working. Authorization flows through Tuyo's back end, so if Tuyo is offline, the card declines. Funds are recoverable from the wallet, but card-as-spending-method ends with the company.

Comparison to exchange-custodial cards. Custodial cards (Coinbase, Crypto.com, Bitget, KAST) pool your funds in exchange accounts. If the exchange fails, you join the unsecured creditor queue (FTX users initially lost 100%, then recovered 40-60% after bankruptcy proceedings). With Tuyo, your USDC is structurally outside that risk.

Real User Scenarios

Scenario 1: Maria, freelance designer in Mexico City ($1,500/month)

Setup: Maria gets paid in USDC by US clients via Bridge's virtual SPEI account. USDC auto-deposits into her Tuyo wallet on Base. She uses the Tuyo Card via Apple Pay for daily spending split roughly 80% online USD subscriptions and 20% local MXN purchases.

Results after 12 months: $18,000 spent on the card. USD slice ($14,400) cost $0 in FX. MXN slice ($3,600) cost approximately $36 (1% FX). She avoided roughly $450/year in conversion fees compared to converting USDC to MXN through a Mexican exchange first. She accrued TUYOs across the full $18,000 of card spend.

Verdict: "I get paid in USDC and spend in USDC. The 0% USD fee is the entire pitch and Tuyo delivers it. The TUYOs are speculative but I am spending anyway."

Scenario 2: James, US software engineer ($2,500/month)

Setup: James moves $5,000 in USDC from Coinbase Wallet to Tuyo. He already self-custodies and is comfortable managing seed phrases. He uses the card for 95% domestic USD spending (groceries, dining, travel) and 5% international online purchases.

Results after 12 months: $30,000 spent. FX cost on the 5% non-USD slice: approximately $15. He chose Tuyo over Coinbase Card (4% cashback in BTC) and forwent $1,200/year in guaranteed cashback for self-custody and a TUYOs position. TGE value of his accrued TUYOs is undetermined.

Verdict: "I am betting the TUYOs TGE delivers more than $1,200 in token value at vesting. Coinbase Card was the safer pick, but I wanted the self-custody."

Scenario 3: Sofia, Berlin-based crypto user ($3,000/month, mostly EUR)

Setup: Sofia loads Tuyo with USDC bridged from Optimism. She spends primarily in EUR at local merchants and online. Apple Pay is her primary tap method.

Results after 12 months: $36,000 spent, 90% in EUR. FX cost: approximately $324 (1% on $32,400). Compared to Gnosis Pay with EURe (0% FX), she paid $324 more in FX over the year. She kept Tuyo for the TUYOs position but moved high-volume EUR spending to Gnosis Pay.

Verdict: "Tuyo is great for USD. For EUR I switched to Gnosis Pay after three months. I keep the Tuyo Card for travel outside the eurozone and to keep accruing TUYOs."

How the Tuyo Card Compares

For US-based USDC spenders: The Tuyo Card competes with Coinbase Card (4% rotating cashback, $0 fee, custodial) and Avici (secured credit, no rewards, self-custodial via Rain). Coinbase Card has higher guaranteed returns but is custodial. Avici uses the same Rain issuer as Tuyo but is a credit-line product against crypto collateral. Tuyo's value over both is the TUYOs upside and the simpler debit model.

For EU-based USDC spenders: Gnosis Pay (0% FX on EURe, up to 5% GNO cashback with token holdings) beats Tuyo on EUR economics. Ready Metal did too before its program became unavailable. Tuyo wins if you specifically want USD-settled spending or want exposure to the 2026 TGE.

For ETH-rich users wanting tax efficiency: ether.fi Core lets you borrow against staked ETH without selling, avoiding taxable disposal events. Tuyo debits USDC directly from your wallet, which is a stablecoin-to-stablecoin event with effectively zero taxable gain. Both are tax-efficient but in different ways: ether.fi avoids selling ETH; Tuyo avoids spending volatile crypto.

Tuyo Card unique value: Free, self-custodial, USDC-only Visa with a credible 2026 TGE and 20% supply reservation for users. The simplest entry to self-custody spending plus speculative airdrop exposure available globally outside the UK.

Who Should Choose the Tuyo Card

Use the Tuyo Card if:

- You spend primarily in USD and want zero fees on USD purchases

- You hold USDC on Base or any major L2 and want to spend it without selling

- You want exposure to a planned 2026 token launch with 20% supply reserved for users

- You prefer self-custody over exchange custody for stablecoin balances

- You already use Tuyo Earn, Trade, or Transfer

Skip the Tuyo Card if:

- You spend primarily in EUR or GBP (use Gnosis Pay instead)

- You need ATM cash access today (no physical card, no ATM yet)

- You are based in the United Kingdom (services not intended for UK persons)

- You prefer guaranteed cashback over speculative token rewards

- You want to spend BTC or ETH directly

The Tuyo Card lands as the cleanest free self-custodial Visa for USDC spenders globally. The 0% USD fee and TUYOs TGE are the differentiators; the physical card and non-USD FX are the limitations. For the right user, it is a strong addition to a stablecoin-first spending stack alongside one cashback-optimized card for non-USDC spending.

Sources and Verification

All card specs, fees, and limits verified from:

User scenarios are composite illustrations based on Tuyo's published fee schedule and reward terms. TUYOs token value, TGE date, and per-TUYO conversion ratio are not disclosed; treat any token-related projections as speculative.

Written by Aleksandar Dukic

FAQ

What fees does the Tuyo Card have?

No issuance fee, no monthly or annual fee, and 0% on USD transactions. The only cost is a small FX spread of up to ~1% when spending in currencies other than USD.

Which tokens work with the Tuyo Card?

The card is powered by USDC on Base. You can deposit USDC (or any token) on Ethereum, Base, Arbitrum, Optimism, or Polygon and convert it to Base USDC for free inside Tuyo.

Does Tuyo support Apple Pay and Google Pay?

Yes. The Tuyo Card can be added to Apple Pay and Google Pay. In some cases Apple or Google may decline the add based on their own device, location, or account risk checks.

What are the card spending limits?

Spending starts at $2,000/day at card activation and increases with usage and account history up to $10,000/day. Tuyo can only debit up to your active daily limit from your USDC on Base balance.

Is the Tuyo Card available in the UK?

No. Tuyo's services are not intended for and should not be accessed by persons located in the United Kingdom.

Does the Tuyo Card have a referral bonus or promo code?

Yes. Use Tuyo Card referral code sulik by signing up through SpendNode's Tuyo link. New users get $10 after making at least five card payments of $5 or more on five different days.

Is Tuyo Card referral code sulik working in August 2026?

Yes. sulik is a working Tuyo Card referral code as of August 10, 2026 - we re-verify it regularly. Sign up through the referral link, then make at least five card payments of $5 or more on five different days to qualify for the $10 reward.

This is a debit card. Some merchants with pre-authorization holds (hotels, car rentals) may temporarily hold funds beyond the transaction amount.

You retain custody of your funds until the moment of spending. Your balance is not exposed to provider insolvency risk.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?

User Reviews

Reviews are moderated and may take a moment to appear.