SpendNode Rating for Rizon

Rizon combines a US-issued Visa Platinum, self-custodial stablecoin collateral, and passport-based access across 49 nationalities with unusually low entry and plan pricing. The card flow worked smoothly in our testing, and the published fee schedule includes competitive international and ATM rates.

The product scores well for a coherent working stack: a named US issuer, user-controlled smart-contract collateral, virtual and physical Visa cards, USD and EUR account details, and paid tiers that materially reduce fees. We completed signup, KYC, funding, and card activation ourselves. Rizon also publishes its plan rates, cashback cap, ATM pricing, and exclusions; the remaining deductions reflect its short operating history and inconsistencies between some terms and marketing surfaces.

Issuer Snapshot

Editorial vendor score stays separate from user reviews. Methodology

Product Quality

4.3

Trust & Custody

4.4

Fee Transparency

4.3

Operational Reliability

4.2

Market Relevance

4.5

On This Page

Rizon is a stablecoin spending app operated by Rizon Global, Inc. (Delaware) whose US-issued Visa Platinum cards, issued by Third National, are secured by stablecoin collateral held in the user's own non-custodial smart-contract wallet. Eligibility is passport-based across 49 nationalities, with virtual and physical card formats and three subscription plans that set the fee and cashback economics.

What Is Rizon?

Most crypto cards draw their maps by residence. Rizon draws its map by citizenship: if your passport is on its 49-nationality list, you can open an account and hold a US-issued Visa Platinum from anywhere you happen to live. A Pakistani engineer in Riyadh, an Egyptian designer in Kuwait, a Filipino seafarer between ports - all shut out of most US card products by their address - qualify through their passport.

That is the product in one sentence. Around the card, the app stacks a US virtual bank account and EUR account details (through integrated banking partners), stock investing with names like Tesla and Apple, stablecoin deposits on three chains, and a subscription system that decides your fees and cashback.

We signed up, verified, and funded an account ourselves in July 2026. KYC cleared in about two minutes and the first top-up was spendable immediately - one of the faster onboardings we have tested.

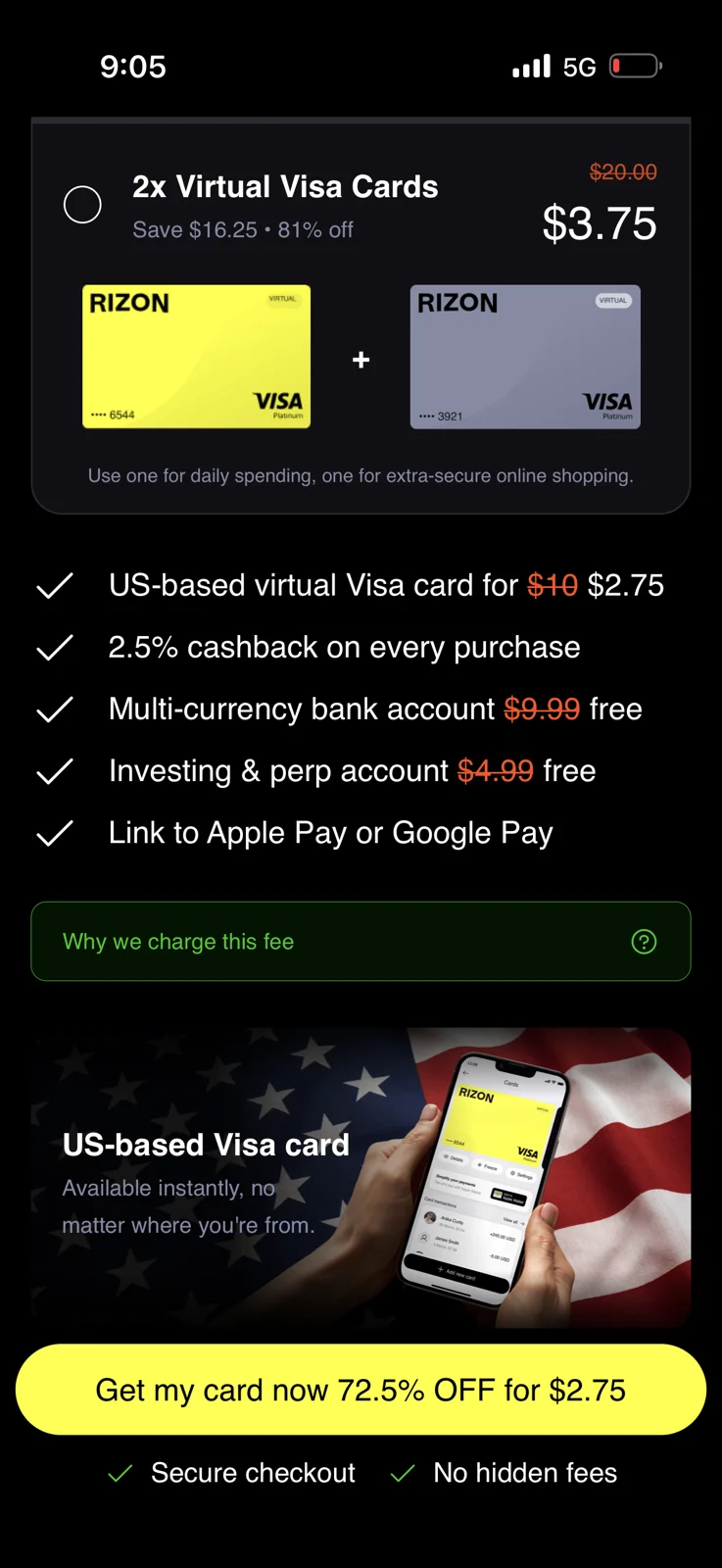

The pricing hook matters up front: the virtual card lists at $10, and SpendNode's code spendnode cuts it to $1. That makes Rizon the cheapest US-issued Visa entry in our catalog, and the sensible way to test everything this review covers.

Available crypto cards by Rizon in July 2026

1. Rizon Standard Card

A $1 US virtual Visa Platinum for passport holders the traditional card system skips.

2. Rizon Gold Card

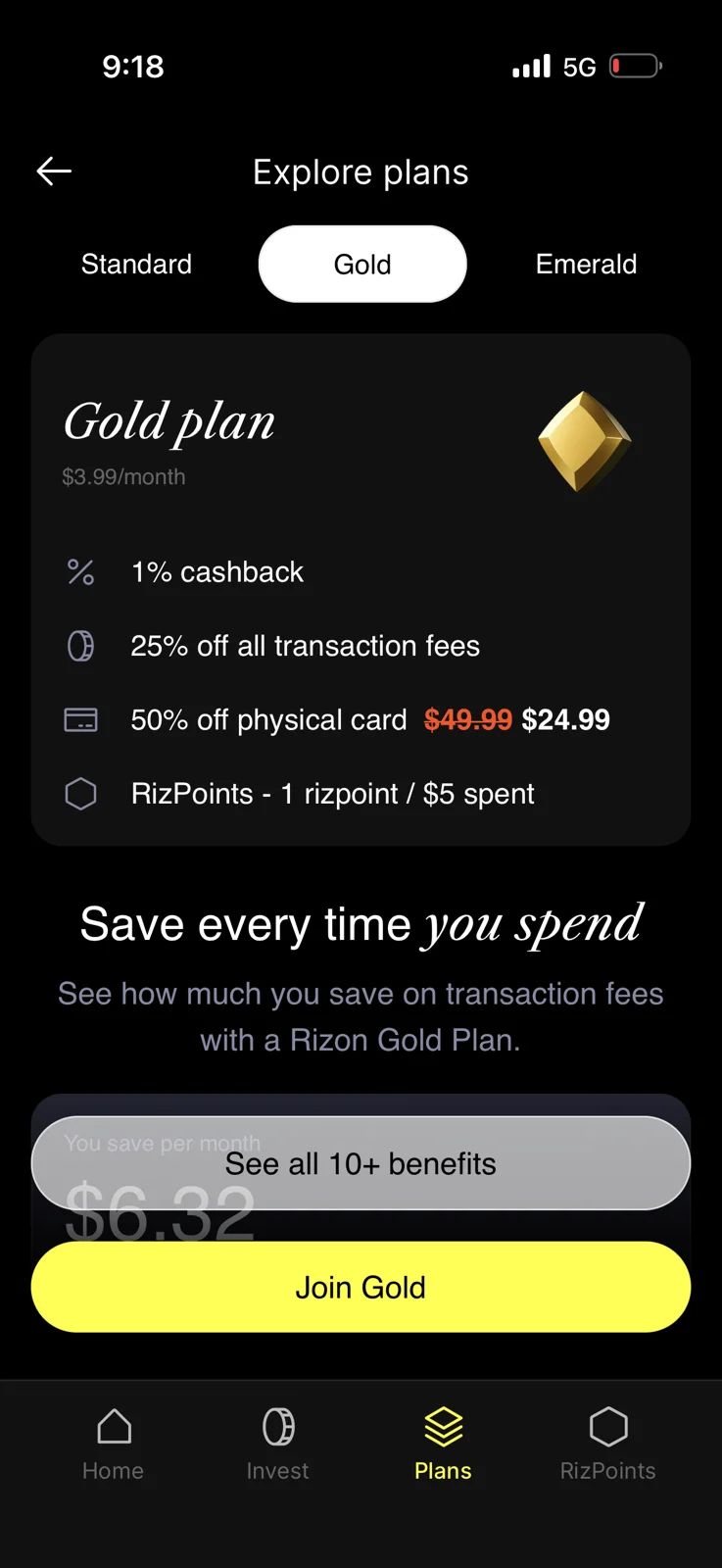

The fee-discount tier: international transaction costs drop to ~1.275% and the plan fee earns itself back in cashback.

3. Rizon Emerald Card

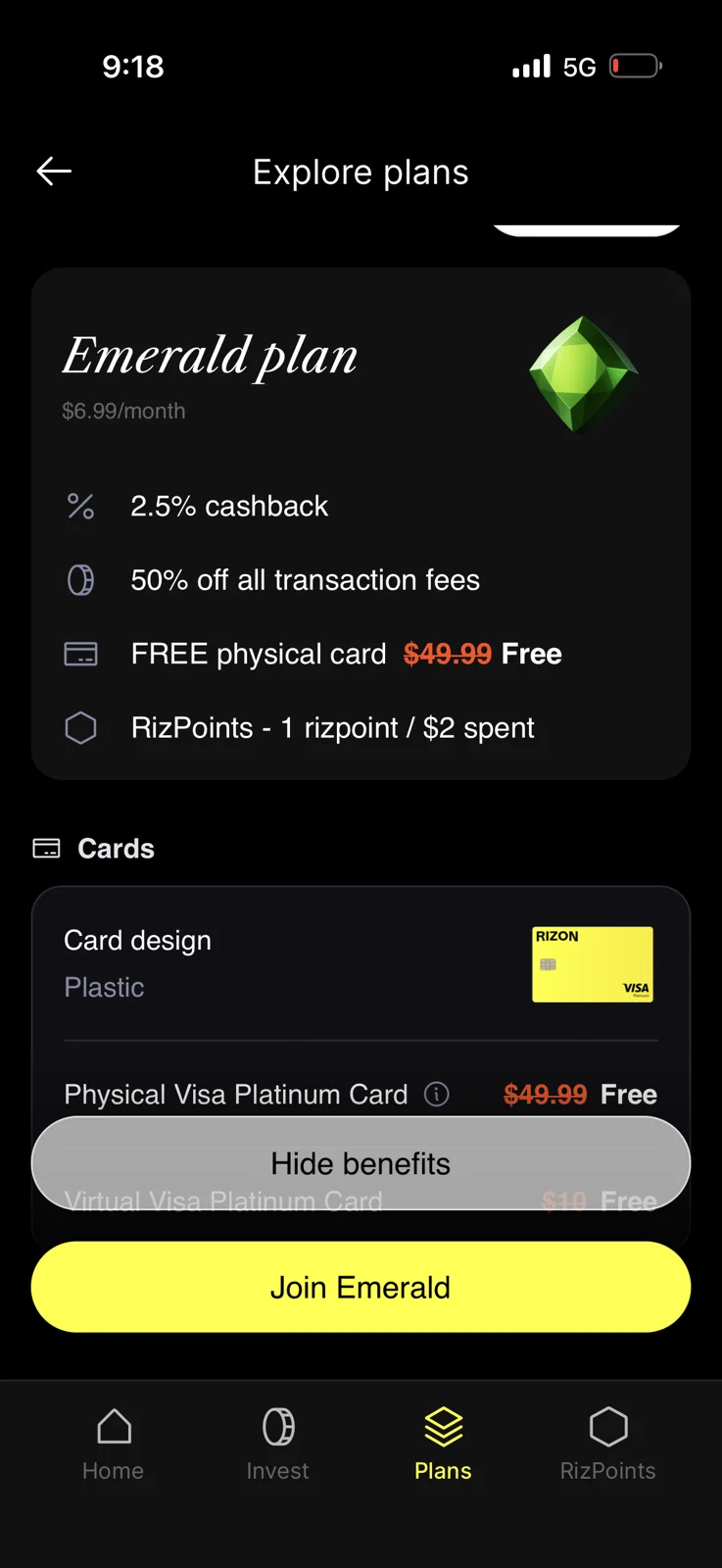

Rizon's top plan: international fees near 1%, trading at 0.85%, and the physical Visa Platinum included.

The Card Lineup

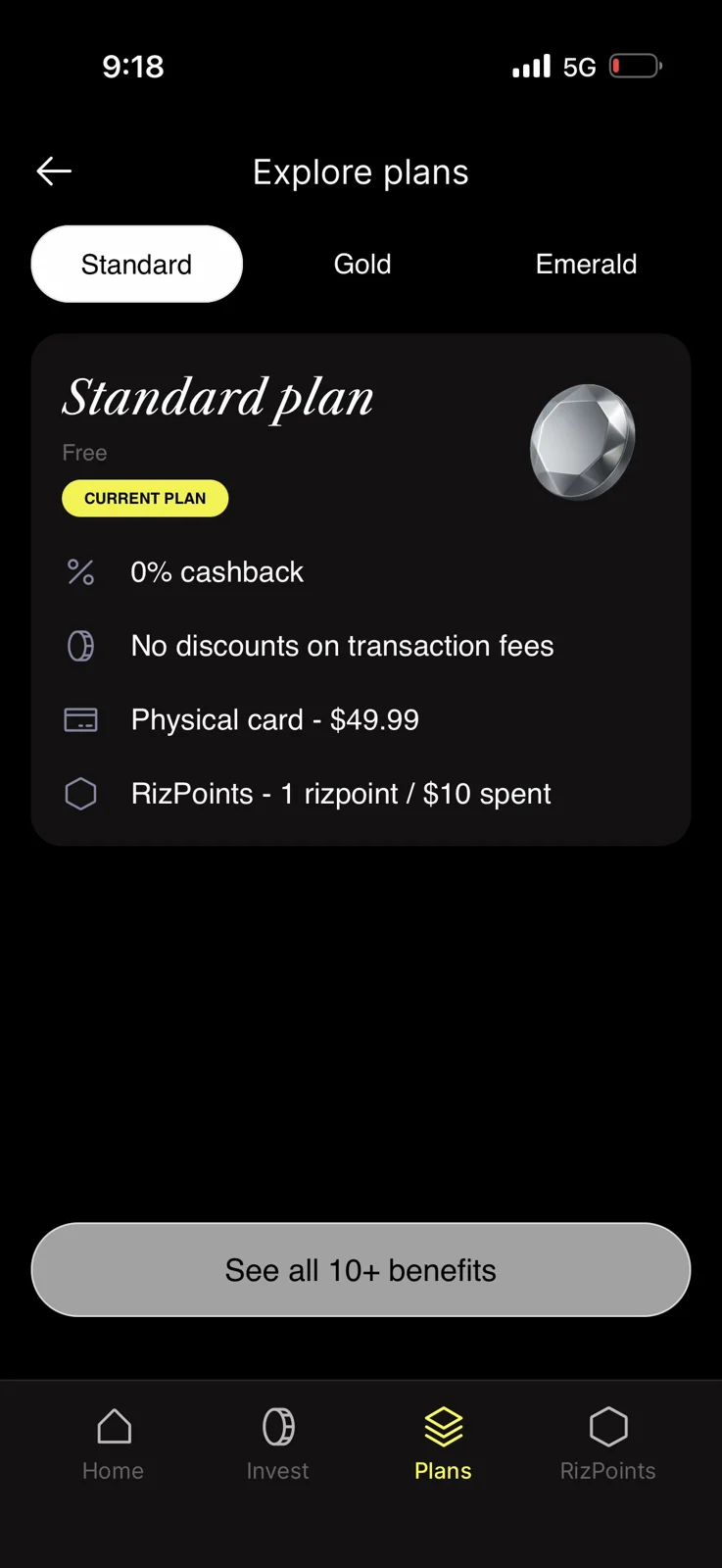

Rizon sells one card on three plans. Every plan runs the same US-issued Visa Platinum and the same collateralized account; the tier changes the economics.

- Rizon Standard Card - The free plan and the $1 entry point (code spendnode). Full fees, no cashback, US Visa access.

- Rizon Gold Card - $3.99/month: 25% off transaction fees (~1.275% international), 1% cashback capped at the plan fee, free virtual card, physical at $24.99.

- Rizon Emerald Card - $6.99/month: fees near 1%, trading at 0.85%, 2.5% cashback capped at the plan fee, both cards included.

- Metal card - Announced as coming soon; not yet purchasable.

Virtual cards issue in minutes on all plans, the physical card is available on all plans at tier-dependent pricing, and paid plans carry a minimum 3-month commitment.

The Wallet and Collateral Design

Rizon's architecture is closer to Plasma One than to RedotPay. When you sign up, a smart-contract wallet is created for you (wallet infrastructure by Privy) on Polygon, Optimism, or Arbitrum. Your USDC or USDT sits in that contract, controlled by you.

The card itself is legally a collateralized charge card from Third National: the stablecoins in your wallet secure whatever you spend, the account runs at 0% APR with no interest mechanics, and the balance settles from your collateral. Rizon's own terms are explicit that the company does not custody funds, transmit money, or hold your keys.

The practical meaning: if Rizon the company disappeared, your stablecoins would still be in a contract your wallet controls. The card would stop working; your money would not stop being yours. After the passport-based access, this is Rizon's strongest structural feature.

One nuance worth recording: Rizon operates under two terms sets. US persons contract with the US Spend Card Terms (international fee 1.7% + $0.10); everyone else accepts a parallel non-US agreement (1.7% + $0.30, and a second clause in the same document that says 1.5% + $0.30). Their general app terms, under a Lithuanian entity, also describe an earlier Rain-issued debit program. The product you get today in the app is the Third National card; the paperwork has not fully caught up with itself.

Fees, Plans, and Rates

The three Rizon plans as shown in-app in July 2026. Rizon runs near-constant in-app discount promotions, so treat listed prices as ceilings.

| Feature | Standard (free) | Gold | Emerald |

|---|---|---|---|

| Price | $0 | $3.99/mo | $6.99/mo |

| Minimum commitment | - | 3 months | 3 months |

| Cashback | 0% | 1% | 2.5% |

| Cashback cap per period | - | One month's plan fee | One month's plan fee |

| International fee | 1.7% + $0.10-0.30 | ~1.275% (25% off) | ~1.02% (40% off) |

| Trading fee | 1.7% | ~1.275% | 0.85% |

| Small-transaction fee | $0.50 | $0.38 | $0.25 |

| Virtual card | $10 ($1 with code spendnode) | Free | Free |

| Physical card | $49.99 | $24.99 | Included |

| ATM withdrawal | $1 + 0.65% | $1 + 0.65% | $1 + 0.65% |

| RizPoints earn | 1 / $10 spent | 1 / $5 spent | 1 / $2 spent |

| Bank account opening | $1.99 | $0.99 | Free |

USD spending at US merchants carries no listed transaction fee on any plan, which is the clean path through the whole schedule. The ATM rate deserves its own sentence: $1 + 0.65% is materially cheaper than the 2-3% typical of prepaid competitors, and it is published, which several rivals' ATM terms are not.

How the cashback cap works

Rizon's help documentation states that cashback is capped at the value of one month's subscription fee for each subscription period. On Emerald, the 2.5% stops accruing once it reaches the Emerald fee, which happens at roughly $280 of eligible monthly spend.

The structural consequence: Rizon's cashback rebates the plan fee rather than paying beyond it. For active spenders that makes the paid plans effectively free, and a free plan you were buying anyway for the fee discounts is a fine outcome.

It is a different mechanism from cards like KAST (1.5% USD to $2,000/month, no fee-linked cap) or Plasma One (2% in XPL on the free tier), where cashback accrues independently of any subscription. Compare the programs by mechanism, not by headline rate.

The dependable value in the plans is the fee discounts: a Gold subscriber spending $800/month internationally saves roughly $3.40/month in transaction fees, and the capped cashback returns the plan fee on top.

Gold crosses the free plan at roughly $280/month of international spend; Emerald crosses at roughly $220/month and overtakes Gold at about $170/month, where its higher cashback rate plus deeper fee discount cover the extra $3 of monthly fee. The per-tier break-evens live on the Gold and Emerald pages.

What earns cashback and what does not

Rizon publishes an MCC exclusion list, and it covers more ordinary life than most: insurance premiums, utilities, rent payments, education, tax and government payments, money transfers, quasi-cash, gambling, charities. Card purchases at regular merchants earn; bill-shaped spending largely does not. Cashback stacks with RizPoints - you always earn both on eligible spend.

One checkout note: the purchase screen advertises "2.5% cashback on every purchase," a rate that requires the Emerald plan and is subject to the cap and exclusions above. And Rizon runs rotating in-app discounts more or less permanently (72.5% off when we signed up), so treat list prices as ceilings. Our code spendnode beats the rotating offers at 90% off, every time.

How to Apply for a Rizon Card

We went through the full flow ourselves in July 2026, and it was one of the faster onboardings we have tested: account, KYC, and first top-up finished in about two minutes.

Step 1. Download Rizon and sign up. iOS or Android. The app asks for a referral code right away; that screen can be skipped (SpendNode's discount code comes later, at the card purchase step).

Step 2. Complete KYC. Passport-based verification with a selfie check. This is where the 49-nationality rule applies: the passport decides eligibility, not your address. Our verification cleared in roughly two minutes.

Step 3. Buy the card with code spendnode. At the card purchase step, the app shows a rotating discount with a countdown timer (72.5% off when we signed up). Ignore the clock and enter spendnode instead: 90% off, $1 for the virtual card, every time.

The card purchase step. The app's rotating offer showed 72.5% off with a countdown when we signed up; code spendnode prices the card at $1 regardless.

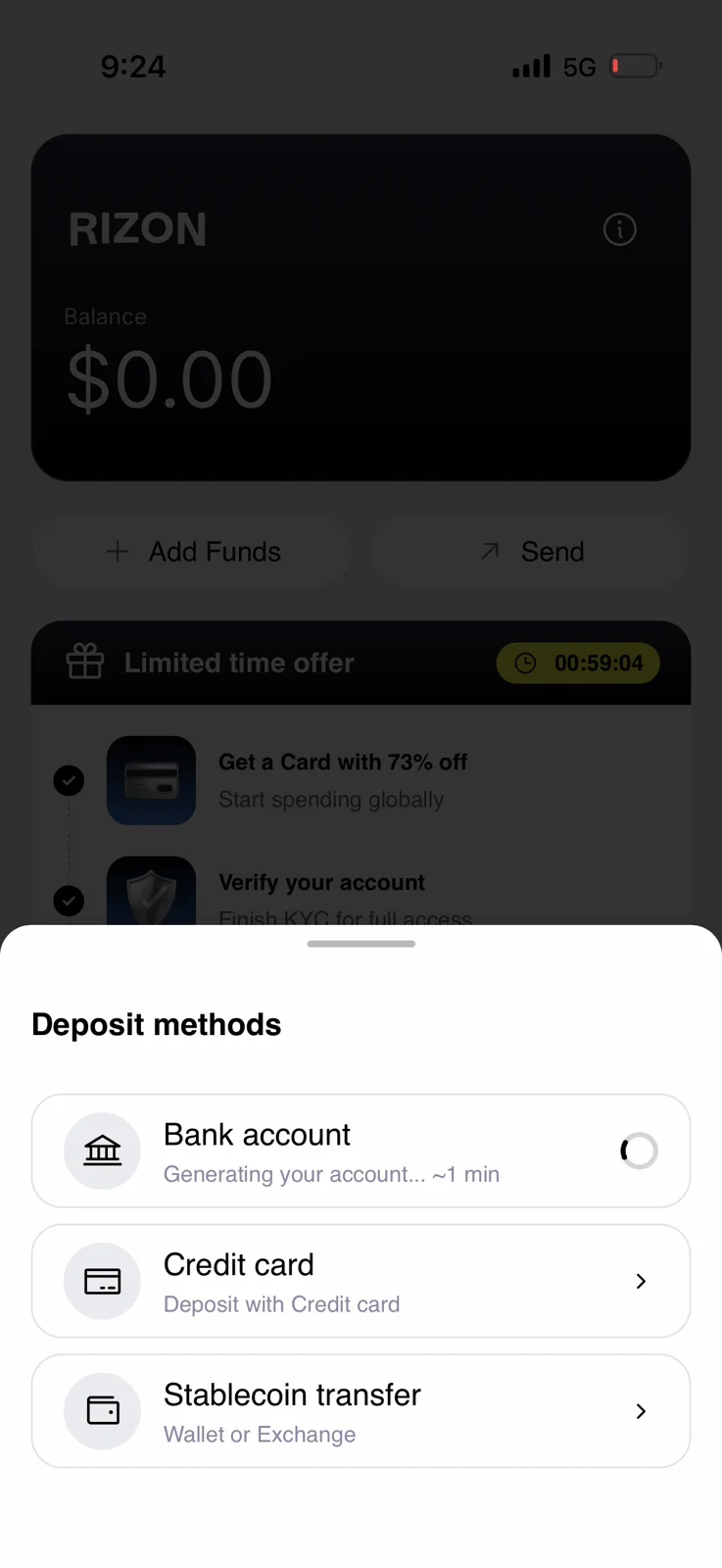

Step 4. Fund the wallet. Three deposit routes: a US bank account (virtual account details generate in about a minute), a credit card, or a stablecoin transfer from any wallet or exchange. We funded with stablecoins; the balance was spendable immediately.

SpendNode app screenshot

The three funding rails - bank transfer to generated US account details, credit card, or stablecoin transfer. The stablecoin route settles fastest and matches the card's collateral design.

Step 5. Add to Apple Pay or Google Pay and spend. The virtual card provisions to phone wallets immediately; the physical card, if ordered, ships to the 49-country delivery list.

Countries and Availability

Rizon is available in 49 countries as of July 2026. We count a country here when at least one active Rizon card variant lists it, so individual product pages may be narrower.

Available Regions

Africa

Cote d'Ivoire (CI), Egypt (EG), Ghana (GH), Kenya (KE), Morocco (MA), Senegal (SN), South Africa (ZA), Uganda (UG), Zambia (ZM)

Americas

Antigua and Barbuda (AG), Argentina (AR), Bahamas (BS), Barbados (BB), Belize (BZ), Bolivia (BO), Brazil (BR), Cayman Islands (KY), Colombia (CO), Costa Rica (CR), Dominica (DM), Dominican Republic (DO), Ecuador (EC), El Salvador (SV), Grenada (GD), Guatemala (GT), Guyana (GY), Honduras (HN), Mexico (MX), Panama (PA), Paraguay (PY), Peru (PE), Saint Kitts and Nevis (KN), Saint Lucia (LC), Saint Vincent and the Grenadines (VC), Suriname (SR), Trinidad and Tobago (TT), Turks and Caicos Islands (TC), United States (US), Uruguay (UY)

Asia

Bangladesh (BD), Japan (JP), Malaysia (MY), Pakistan (PK), Philippines (PH), Singapore (SG), Thailand (TH), United Arab Emirates (AE)

Oceania

Australia (AU), New Zealand (NZ)

Major Restricted Markets

These major markets are not currently listed for this vendor. Confirm eligibility with the issuer before applying, especially where card tiers have different country rules.

Africa

Nigeria (NG)

Americas

Canada (CA), Chile (CL)

Asia

China (CN), Hong Kong (HK), India (IN), Indonesia (ID), South Korea (KR), Taiwan (TW), Turkey (TR)

Europe

Austria (AT), France (FR), Germany (DE), Italy (IT), Netherlands (NL), Poland (PL), Portugal (PT), Spain (ES), Switzerland (CH), United Kingdom (GB)

Because the gate is the passport rather than the address, the practical map is wider than the list: an eligible passport holder living in Saudi Arabia, Qatar, or anywhere else can register, subject to sanctions rules. The 122+ and 147+ country figures in Rizon's marketing describe where the card can spend, which follows ordinary Visa acceptance, not who can sign up.

Physical card delivery covers the same 49 countries. KYC (passport + selfie) is required; supported deposit chains are Polygon, Optimism, and Arbitrum; assets are USDC and USDT; Apple Pay and Google Pay are supported everywhere the card exists.

Rizon vs Other Cards

-

vs RedotPay: The closest competitor by audience. RedotPay is custodial with residence-based registration across ~100 markets and a longer track record; Rizon counters with self-custodial collateral, a US-issued card, cheaper entry ($1 with our code vs $8 with RedotPay's), and cheaper cash: $1 + 0.65% at ATMs against RedotPay's 2-3%, and Emerald's ~1.02% international fee against RedotPay's 2.2% all-in.

-

vs KAST: KAST pays 1.5% USD cashback on a free tier with global shipping, the stronger pure-rewards story. Rizon answers with the US-issued account, self-custody, the $1 entry, and several core passports (Pakistan, Bangladesh, Egypt) where its eligibility is first-class rather than incidental. KAST's paid tiers start at $1,000; Rizon's top plan is $83.88 a year.

-

vs Plasma One: The architectural sibling: self-custodial stablecoin collateral, 0% APR, chain-native design. Plasma One pays cashback in its volatile XPL token and yield on idle balance; Rizon pays in fee relief and a USD-denominated rebate, and adds USD/EUR account details plus in-app stock investing that Plasma One does not have. Their eligibility maps overlap only partly, and Rizon's LATAM-Africa-South Asia coverage reaches passports Plasma One's list misses.

-

vs Jupiter Global: Jupiter pays 2% USDC on a free virtual card and suits USDC-native freelancers. Rizon's case against it is structural: a US-issued Visa Platinum with a bank-account layer and physical card options, where Jupiter is virtual-only with QR handoff.

Is Rizon Safe?

Rizon distributes trust across named counterparties, each with its own role and failure profile.

Rizon Global, Inc. (Delaware C-Corp) operates the app for global users and is the entity behind the US and non-US Spend Card Terms. Rizon Technologies, UAB (Lithuania) appears in the general app terms and the collateral mechanics. Third National issues the card; the US agreement is governed by Puerto Rico law and carries US-style consumer disclosures (CFPB account-opening format, Military Lending Act language). Privy provides the wallet infrastructure; the smart-contract wallet is controlled by you. USD and EUR account details come through integrated banking partners; Rizon's terms state it does not itself provide or hold bank accounts.

What happens if any of these fail?

- If Rizon the company shuts down. Your stablecoins are in a smart-contract wallet you control on public chains. You retain ownership; the card stops working.

- If the card issuer terminates the program. The card stops; the wallet survives. This is the most common failure mode in crypto-card history.

- If a banking partner winds down. The USD/EUR account details would follow that partner's process; do not treat them as insured deposits.

- A mechanism to understand rather than fear: the collateral contract can liquidate your balance to settle what you have spent. That is how a 0%-APR charge card can exist without a credit check; it also means the contract, not a support agent, enforces settlement.

The sensible posture is the one we recommend for every stablecoin card: fund the wallet with what you plan to spend and keep savings elsewhere.

Is Rizon a Scam?

No. The markers that usually give away a scam crypto fintech - unverifiable corporate structure, no regulated card issuer, no real KYC, anonymous operators - are absent here.

The corporate structure is verifiable: Rizon Global, Inc. is a Delaware C-Corporation with a registered agent address in Newark, Delaware, and the Lithuanian entity Rizon Technologies, UAB appears consistently across the legal documents. The card issuer, Third National, is named in the Spend Card Terms, and the US product carries the standard federal consumer-credit disclosures a real US card program requires.

KYC is real: passport verification with a selfie liveness check, cleared in about two minutes in our test.

The product works as advertised in our hands-on testing: signup, verification, funding, and the discount code all behaved exactly as described, and the deposit routes (bank details, card, stablecoin transfer) generated and settled properly.

Real risks exist, and they are product risks rather than scam markers: the company is young, the terms documents contain internal inconsistencies (two different fixed FX components in one agreement), the cashback program caps at the plan fee, and the collateral contract enforces settlement automatically. We document all of them on this page and the tier pages; none of them is a reason to doubt the product is real.

SpendNode Verified: The editorial team reviewed Rizon's issuer identity, product terms, public fee schedule, and live card flow per our methodology. We also completed signup, KYC, funding, and card activation in the Rizon app in July 2026. Verification is not an endorsement or guarantee.

Who Should Use Rizon?

Rizon fits people whose passport is on the list and whose problem is access: freelancers paid in dollars who need a US card for the platforms and merchants that reject local ones, expats and workers abroad whose home passport qualifies even where their residence does not, and stablecoin holders across LATAM, Africa, and South Asia who want spending rails without handing custody to an exchange.

The plan mapping is simple. Standard suits USD-denominated spenders and anyone testing the app: at $1 through code spendnode, the trial cost rounds to zero. Gold suits cross-border spenders from about $280/month, where the fee discounts outrun the plan fee. Emerald suits people running Rizon as their main international rail: fees near 1%, both cards included, ATM cash at the cheapest published rate in its peer group, and a plan fee that active spenders get back through the cashback rebate.

It is also one of the few cards in our catalog where the whole stack - card, US account details, EUR details, investing - costs under $7 a month at the top tier. RedotPay Pro runs $129 a year, Plasma One Core $199, KAST's premium tiers $1,000 and up. Rizon's ceiling price is a rounding error next to those, which is exactly what makes the $1 entry worth taking.

Sources and Verification

- Rizon official site

- US Spend Card Terms

- Non-US Spend Card Terms

- Eligibility: supported nationalities

- Plans & RizPoints (rates and cashback cap)

- MCC cashback exclusions

Plan pricing, fees, and card mechanics confirmed against Rizon's help documentation and in-app plan screens, July 2026. Signup, KYC, funding, and the spendnode discount code verified by hands-on testing of the Rizon app, July 2026.

Written by Aleksandar Dukic

Frequently Asked Questions

Are Rizon crypto cards available in the United States?

Yes. Rizon crypto cards are available in the United States.

Does Rizon have a promo code or discount?

Yes. SpendNode's Rizon code is spendnode, entered at the card purchase step for 90% off the virtual card: $1 instead of $10, a deeper cut than the rotating discounts the app shows by default. Sign up through SpendNode's Rizon link and apply the code when you buy the card. We tested the signup flow ourselves in July 2026.

Is the Rizon card a credit card or a debit card?

Legally it is a collateralized charge card issued by Third National with 0% APR: your own stablecoin balance secures what you spend, held in a smart-contract wallet you control. In practice it behaves like a prepaid card funded from your wallet. There is no credit check, no interest, and no borrowing beyond your collateral.

Who can get a Rizon card?

Eligibility follows your passport, not your address. Rizon supports 49 nationalities, including the US, Pakistan, Bangladesh, Egypt, Morocco, the Philippines, Malaysia, Thailand, most of Latin America and the Caribbean, and several African countries. An eligible passport holder living anywhere (for example, a Pakistani national in Saudi Arabia) can register; residents of unsupported-passport countries cannot, including all of Europe.

What is the difference between Rizon Standard, Gold, and Emerald?

Standard is free: full 1.7% international fees, no cashback, physical card at $49.99. Gold ($3.99/month) adds 25% off transaction fees, 1% cashback (capped at the plan fee), a free virtual card, and a $24.99 physical card. Emerald ($6.99/month) carries the deepest fee discounts (international ~1.02%, trading 0.85%), 2.5% cashback (same fee-sized cap), and includes both cards free. Paid plans carry a minimum 3-month commitment. The card and account underneath are the same on every plan.

User Reviews

Reviews are moderated and may take a moment to appear.