Plasma One Crypto Cards Review 2026

Compare Plasma One crypto cards and review issuer terms, fees, and availability.

Prefer mobile? Scan to continue

Opens the mobile signup with your SpendNode link, code SPESPE.

SpendNode Rating for Plasma One

Plasma One is the consumer product on top of the Plasma chain, a layer-1 built for stablecoin payments. The card spends from a self-custodial smart wallet, pays cashback in XPL, and an in-app vault earns yield on idle balance. In our testing cashback credited within 48 hours.

The combination of self-custody, a Visa Principal Member issuer (Rain), regulated fiat rails (Bridge), and an on-chain yield vault (Veda) is a coherent design that keeps the trust story clean. The app now lays out every fee in two places, as a preview before you confirm a purchase and again on the receipt afterward, so spenders see the real cost up front instead of guessing. The lineup spans three live tiers (Lite, Core, Platinum), and cashback paid in XPL exposes rewards to token price volatility.

Issuer Snapshot

Editorial vendor score stays separate from user reviews. Methodology

Product Quality

4.3

Trust & Custody

4.4

Fee Transparency

4.3

Operational Reliability

4.2

Market Relevance

4.3

On This Page

Plasma One is the consumer fintech brand operated by Plasma, a layer-1 blockchain purpose-built for stablecoin payments. The Plasma One app bundles a self-custodial Visa card lineup, a yield vault (Earn), and a chain-native rewards program (XPL cashback) into one consumer surface. The card lineup has three live tiers: Lite (free), Core, and Platinum.

Plasma is incorporated in the Cayman Islands with subsidiaries in the UK, US, and the Netherlands. The cards are issued by Rain, a Visa Principal Member, under a license from Visa, with account services powered by Bridge. The products went to public launch in June 2026.

What Is Plasma One?

Plasma is a layer-1 blockchain whose only purpose is moving stablecoins. Most layer-1s are general-purpose. Plasma is the opposite: a chain narrowed to one job, with native USD₮ transfers as a first-class operation and a chain-native token (XPL) as its economic backbone. Plasma One is the consumer fintech app built on top of that chain, the part most users actually touch.

The app has three surfaces:

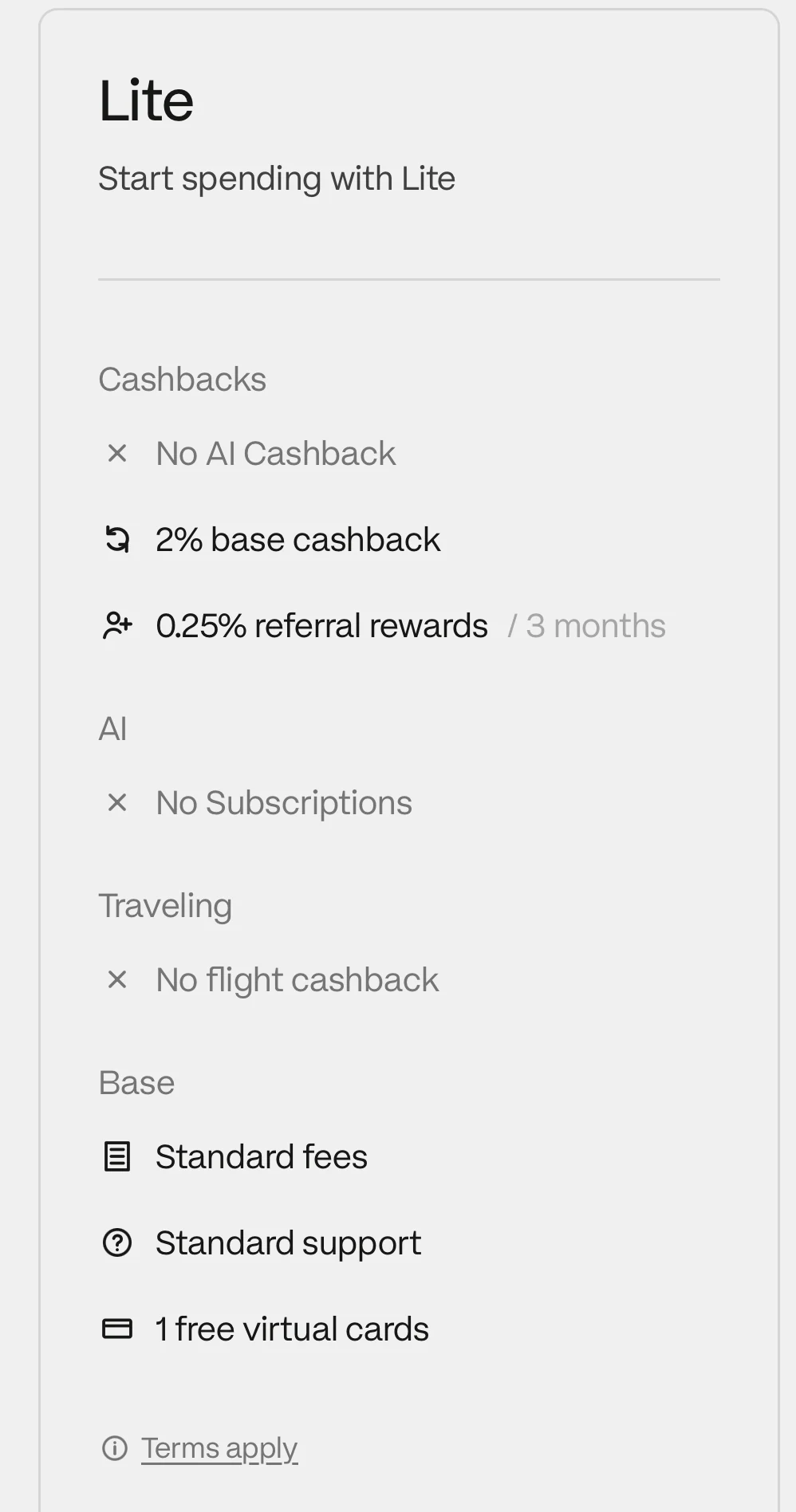

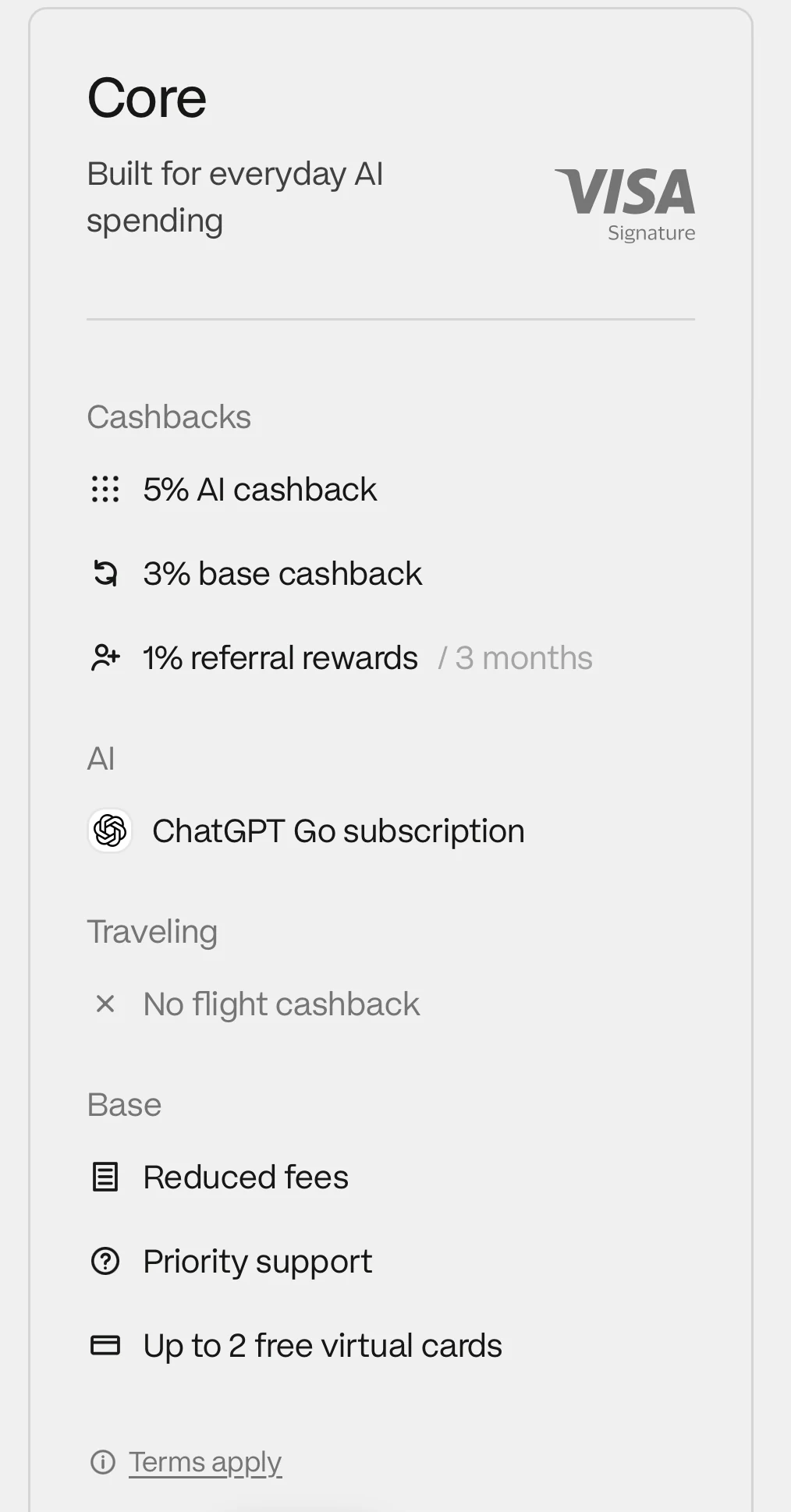

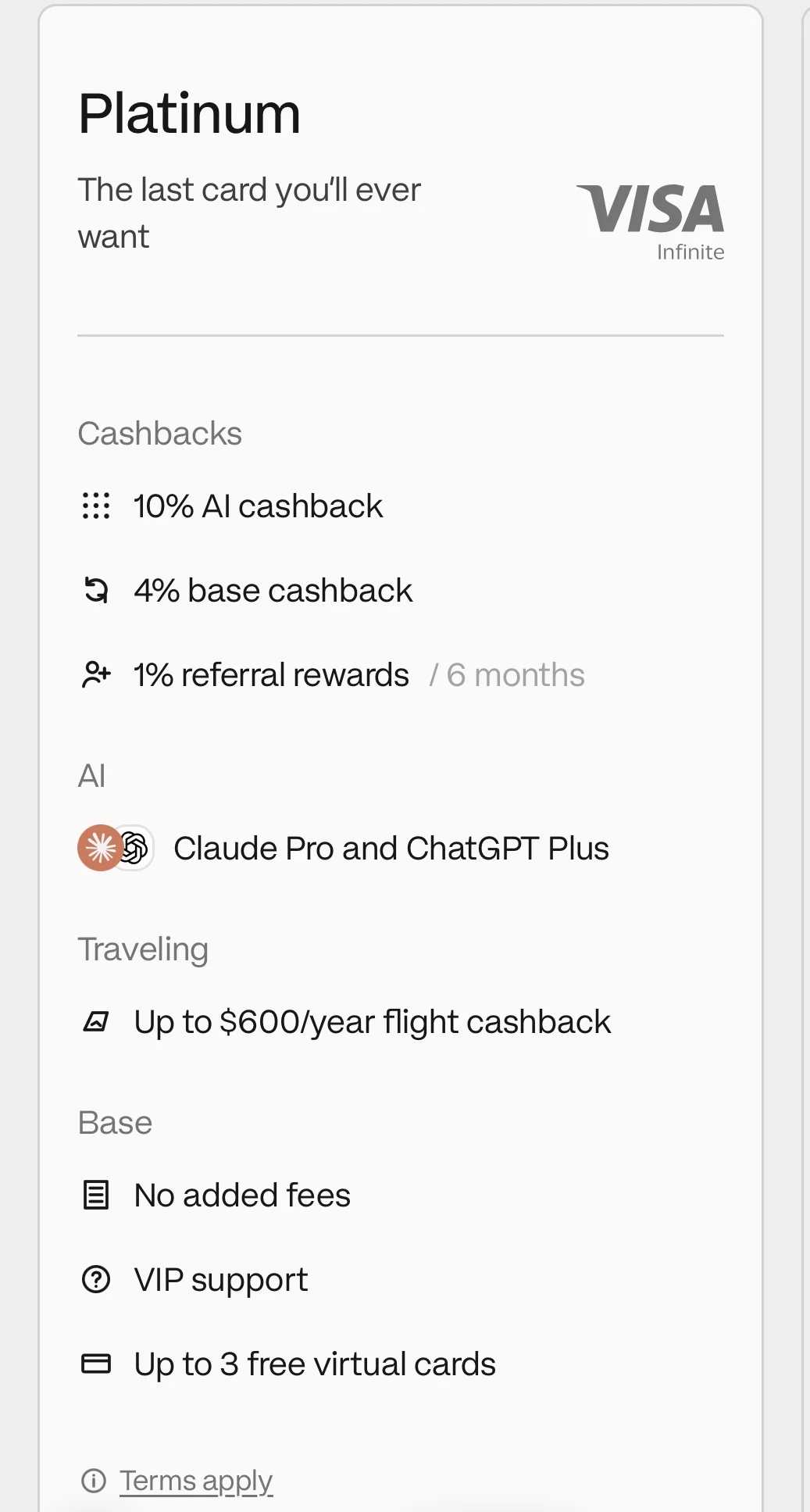

- Card - The Plasma One Card lineup, now in three live tiers. The Lite tier is the free entry point at 2% on the first $500/month, Core adds AI-spend cashback and a ChatGPT Go rebate, and Platinum reaches the top rates with travel perks and a boosted yield.

- Earn - A yield vault operated by Veda Tech Limited that pays variable APY on idle stablecoin balance with no lockup.

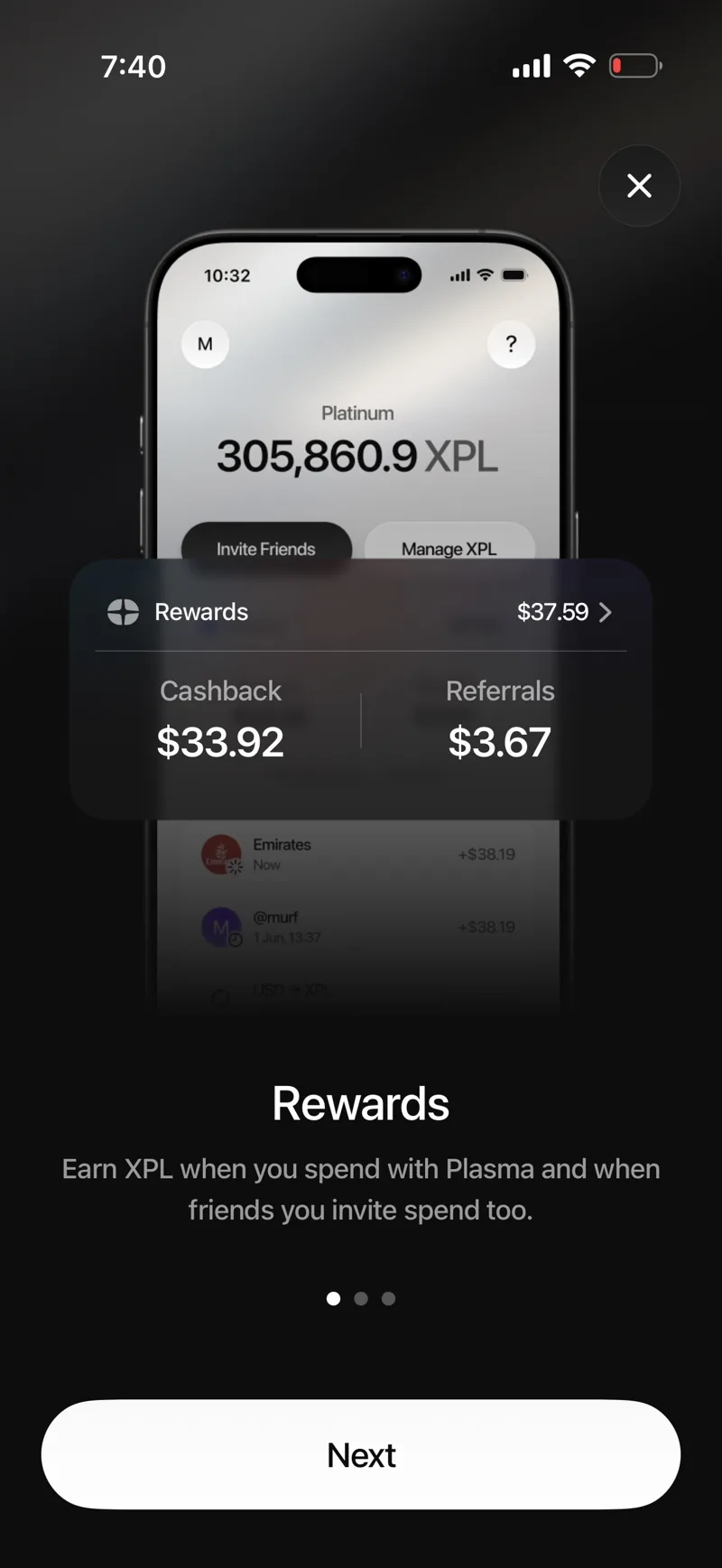

- Rewards - The XPL cashback ledger. Card spend earns 2% to 4% base depending on tier, plus AI and flight boosts on the paid tiers, all paid in XPL on the Plasma chain.

SpendNode app screenshot

The three-surface app - Home for the card, Earn for the yield vault, Rewards for XPL cashback. One app, three sibling products, all backed by the same self-custodial stablecoin wallet on the Plasma chain.

The structural choice that makes Plasma One distinct: the same company gives you the rails (the chain), the spending instrument (the card), and a savings product (the vault), while keeping custody on your side. Most crypto-fintech competitors do one of those three. The closest companies that try to do all three, Crypto.com and Coinbase, take custody. Plasma does not.

We tested Plasma One during early access. The product worked in our hands-on testing: USDT funding on the Plasma chain settled in minutes, card cashback pays out in XPL weekly (on Thursdays), and the Earn vault ran at 3.93% APY with on-demand withdrawals.

Available crypto cards by Plasma One in August 2026

1. Plasma One Lite Card

Free Self-Custodial Visa - 2% XPL Cashback, 0% APR, Up to 5% Variable Yield on Idle Balance

2. Plasma One Core Card

Self-Custodial Visa for AI Spenders - 3% Base, 5% on AI Spend, ChatGPT Go Rebate

3. Plasma One Platinum Card

Premium Self-Custodial Visa - 4% Base, 10% AI, 10% Flights, Lounge Access, Boosted 5% Yield

The Plasma Blockchain

Plasma is the load-bearing piece of the Plasma One story. The card is the visible product, but the chain is what gives the cashback denomination meaning and the funding routes their zero-fee economics.

What it is. A standalone layer-1, independent of Ethereum, Base, Arbitrum, Solana, or any other major chain. Its design optimizes for stablecoin transfers: low-cost and fast, with native USD₮ support that does not depend on a contract-level token like USDT-on-Ethereum or USDC-on-Polygon.

Why it exists. Stablecoin settlement volume has grown into the multi-trillion-dollar range annually and continues to climb. Most of that volume sits on general-purpose chains where it competes with NFTs, DeFi, and trading for blockspace.

A chain built only for stablecoin movement removes that congestion tax and lets payments processors offer routes the user-facing app can credibly call "zero fee" (true for USD₮ on Plasma routes; not true on competing general-purpose chains, where network fees apply).

The XPL token. XPL is the chain's native asset. It pays for transaction costs on the chain (the equivalent of ETH on Ethereum or SOL on Solana), and it is the cashback denomination for the Plasma One Card. That tight loop matters: every dollar of card spend mints demand for XPL via the cashback program, and every dollar of stablecoin transfer on the chain pays in XPL. The card is one of the chain's most visible value-accrual channels.

The token comes with its own risk: XPL price is volatile, and the dollar value of your cashback is determined at the moment of credit, not the moment of spend. We cover the cashback economics in detail on the Lite Card, Core Card, and Platinum Card pages.

SpendNode app screenshot

The XPL rewards ledger - Card spend and referrals both pay out in XPL on the Plasma chain. The Rewards tab splits earnings into cashback and referral lines and lists each credit as it lands.

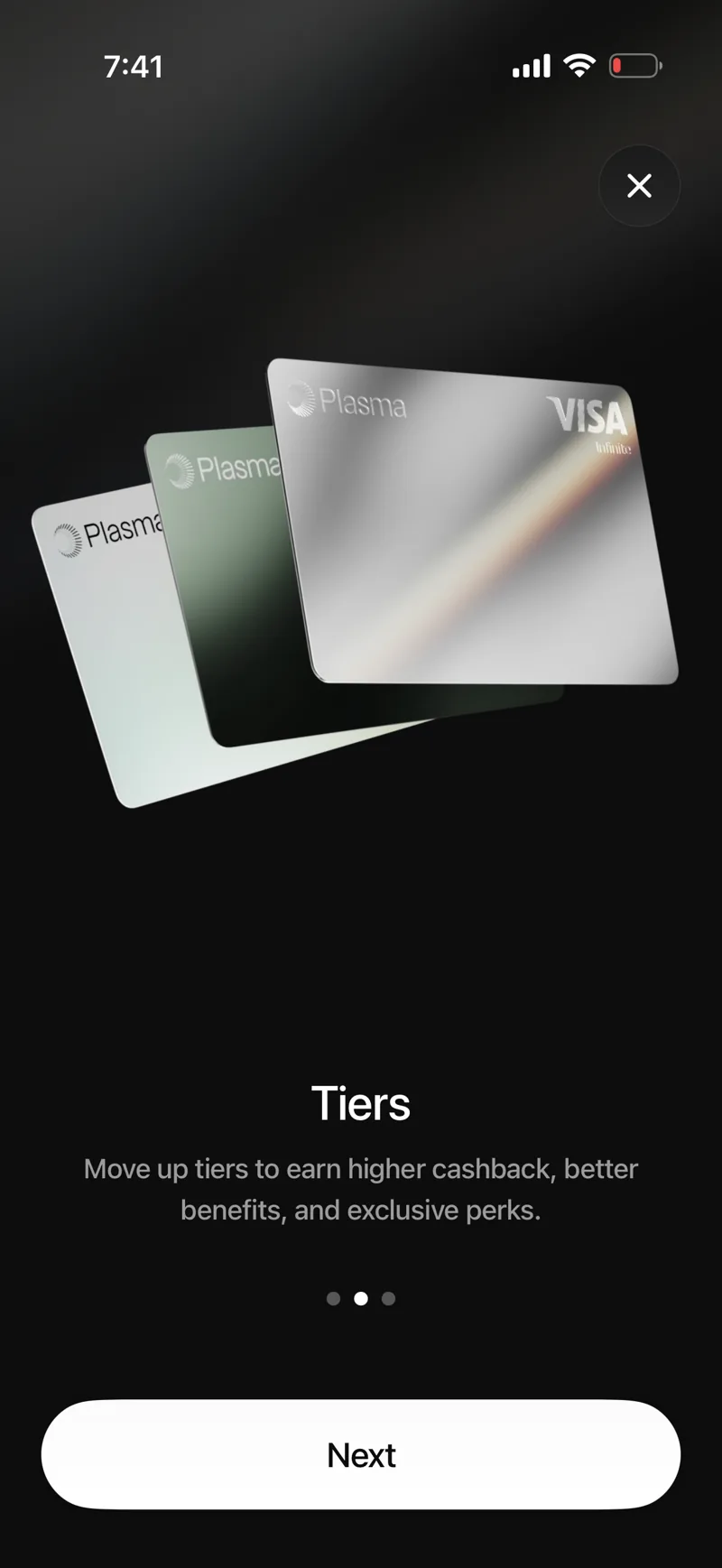

The Card Lineup

Plasma One Cards launched as a three-tier lineup. All three share the self-custodial architecture, Visa rails, XPL cashback, and the Earn vault; they differ on rate, perks, support, and price.

SpendNode app screenshot

The three-tier lineup - Lite is the free white card, Core the green Visa Signature, and Platinum the 16g metal Visa Infinite. Moving up tiers raises cashback and unlocks AI and travel perks.

Plasma One Lite (free). The entry tier on a standard Visa. No annual fee and no token lock, 0% APR, and a 1% FX fee on non-USD spend. Earns 2% cashback on the first $500/month (then 0.1%) in XPL and includes one free virtual card; Lite has no physical card. Best for stablecoin spenders who want a free self-custodial card.

Plasma One Core (Visa Signature, $199/year or a 20,000 XPL twelve-month lock). Earns 3% base (tapering to 2%, then 1%, then 0.25% on higher monthly spend bands) with up to 5% on AI spend (5% to $250/month, then 4%), rebates up to $8/month toward ChatGPT Go when you pay with the card, and adds lower fees (a 0.5% FX fee on non-USD spend, half Lite's rate), priority support, up to two virtual cards, and one physical card.

Plasma One Platinum (Visa Infinite, access by locking 100,000 XPL for 12 months). The top tier earns 4% base, 10% on AI spend, and 10% on eligible flights (up to $600/year back). It rebates up to $20/month each toward Claude Pro and ChatGPT Plus, charges no FX fee on non-USD spend, and ships a 16g metal Visa Infinite card alongside up to three virtual cards.

It adds a full travel stack (discounted Visa Airport Companion lounge access, Visa concierge, travel and rental insurance, baggage protection, a global eSIM, and VIP support), and pays a boosted, fixed 5% yield on the first $500,000 of stablecoin balance. Plasma has not published a fiat subscription price for the tier; the XPL lock is the access path.

For card mechanics, fees, transaction flow, and the full feature deep-dive on each tier, see the Lite, Core, and Platinum reviews.

The Earn Vault

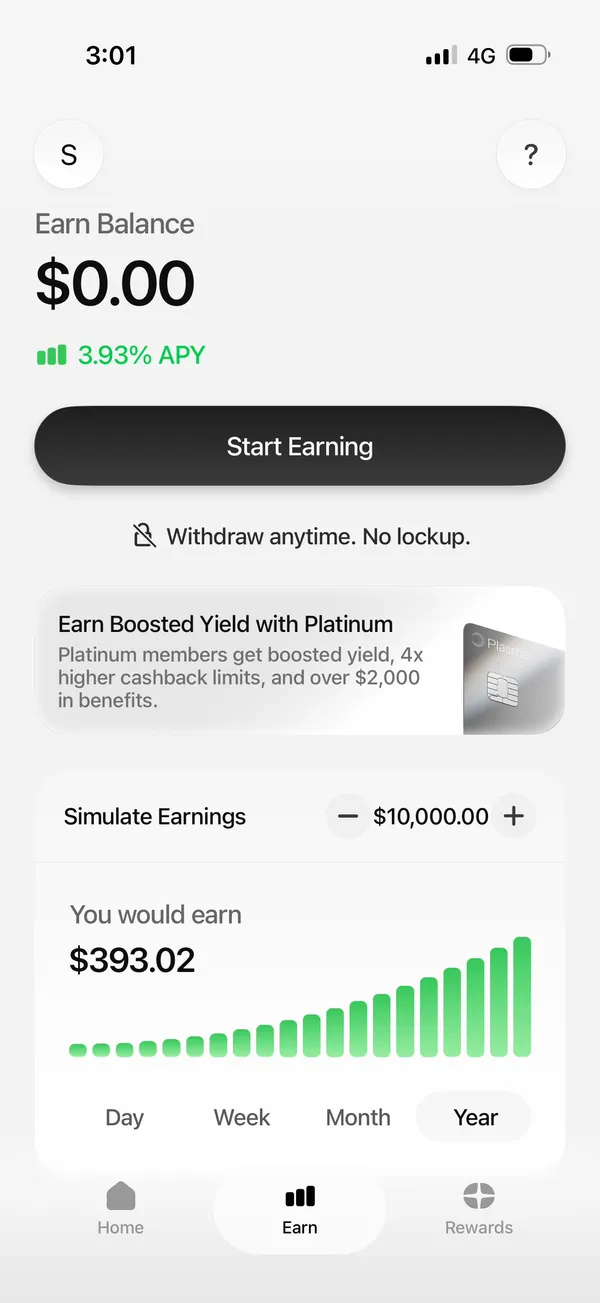

Earn is a separate product inside the same app, built by Veda Tech Limited rather than Plasma directly. Allocate stablecoins to Earn, the app shows a live APY, and the vault accrues yield in real time.

The marketed headline is "up to 5%." The live rate during our testing was 3.93% APY; the fixed 5% is the Platinum tier's "Boosted Yield" benefit, paid on the first $500,000 of balance for active Platinum holders. There is no lockup; withdrawals are atomic and on-demand. Yield comes from on-chain DeFi strategies that Veda curates and routes through audited protocols. It is not a deposit interest rate. It floats with on-chain conditions.

SpendNode app screenshot

Earn vault - The 3.93% APY is the live rate at the time of testing, not the marketing "up to 5%" figure. The simulator projects $393.02 on $10,000 over a year at the current rate. No lockup, withdraw on demand.

The reason this matters at the brand level (not just the card level) is that bundling yield inside a card app is rare. Available self-custodial Visa products such as Tuyo, Avici, and Gnosis Pay require you to leave the app, deploy stablecoins manually to a third-party vault, and accept worse UX. Plasma One ships yield as a button.

The trade-off: Veda is a separate counterparty (BVI-domiciled), and the vault is not available in New York State or other restricted jurisdictions. Smart-contract risk lives at Veda's level, not Plasma's.

Fees and Rates

Headline rates at the brand level across the three tiers. Cashback is paid in XPL on every tier; per-tier mechanics and break-even math sit on each card page.

| Item | Lite | Core | Platinum |

|---|---|---|---|

| Price | Free | $199/yr or 20,000 XPL lock | Lock 100,000 XPL for 12 months |

| Base cashback | 2% | 3% | 4% |

| AI-spend cashback | None | 5% | 10% |

| Flight cashback | None | None | 10% (up to $600/yr) |

| APR on purchases | 0% | 0% | 0% |

| Foreign exchange fee | 1% | 0.5% | None |

| Bank withdrawal fee | 0.75-1% | 0.25-0.35% | Under 0.1% |

| AI subscription rebate | None | Up to $8/mo ChatGPT Go (~$96/yr) | Up to $20/mo each ChatGPT Plus + Claude Pro (~$480/yr) |

| Earn yield | Up to 5% variable | Up to 5% variable | Boosted fixed 5% on first $500k |

| Virtual cards | 1 | Up to 2 | Up to 3 |

| Physical card | None | Up to 1 | Metal Visa Infinite (16g) |

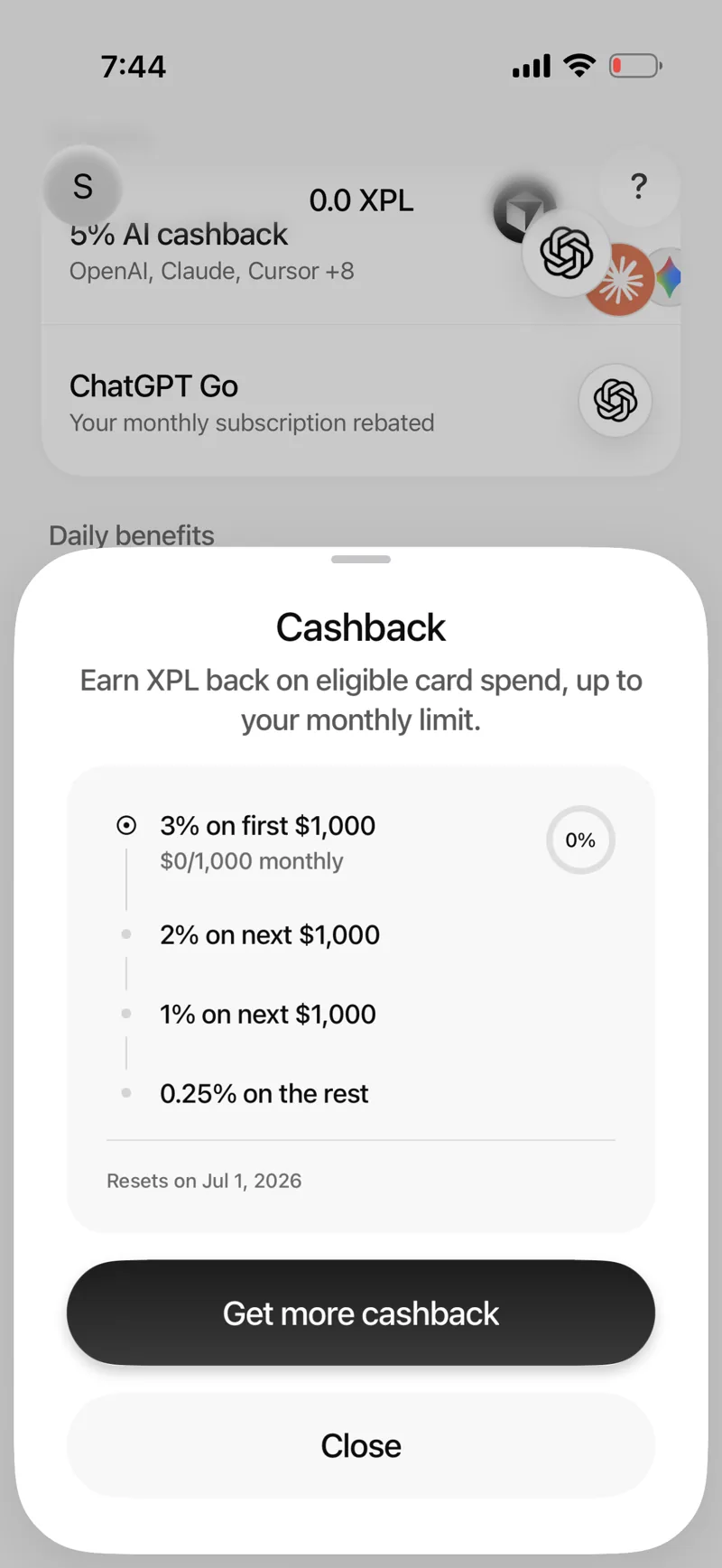

SpendNode app screenshot

Cashback tapers by monthly spend - Rather than a flat rate with a hard dollar cap, XPL cashback steps down as monthly spend rises. On Core it pays 3% on the first $1,000, then 2%, 1%, and 0.25% on the rest; Platinum runs higher and further, at 4% on the first $3,000, then 3% to $10,000, 2% to $15,000, and 1% above. Both reset monthly.

The eligibility net is wider than most issuers'. We paid a monthly insurance premium with our Plasma One card and it earned cashback, the same field test that paid on Tria but earned nothing on Jupiter or xPlace, both of which exclude financial-services merchants. If insurance, subscriptions, or other bill-type payments make up part of your monthly spend, Plasma One counts them.

Plasma does not itemize the FX fee on receipts; it is collected in the conversion rate rather than shown as a labeled line. The per-tier rates above (1% on Lite, 0.5% on Core, none on Platinum) are what applies on non-USD spend.

USDT funding is free on Plasma, Polygon, Ethereum, and Arbitrum; USDC is free up to $30,000 on Polygon, Ethereum, and Arbitrum; USD ACH and wire deposits are free via Bridge.

Lite is virtual-only; Core adds one physical card and Platinum ships a 16g metal Visa Infinite card. Cash advances and balance transfers are excluded in the Card Terms, and ATM withdrawal terms are not published. The full fee deep-dive for each tier sits on the Lite, Core, and Platinum pages.

How to Apply for the Plasma One Crypto Card

Plasma One is live. The path from interested user to first transaction is roughly six steps.

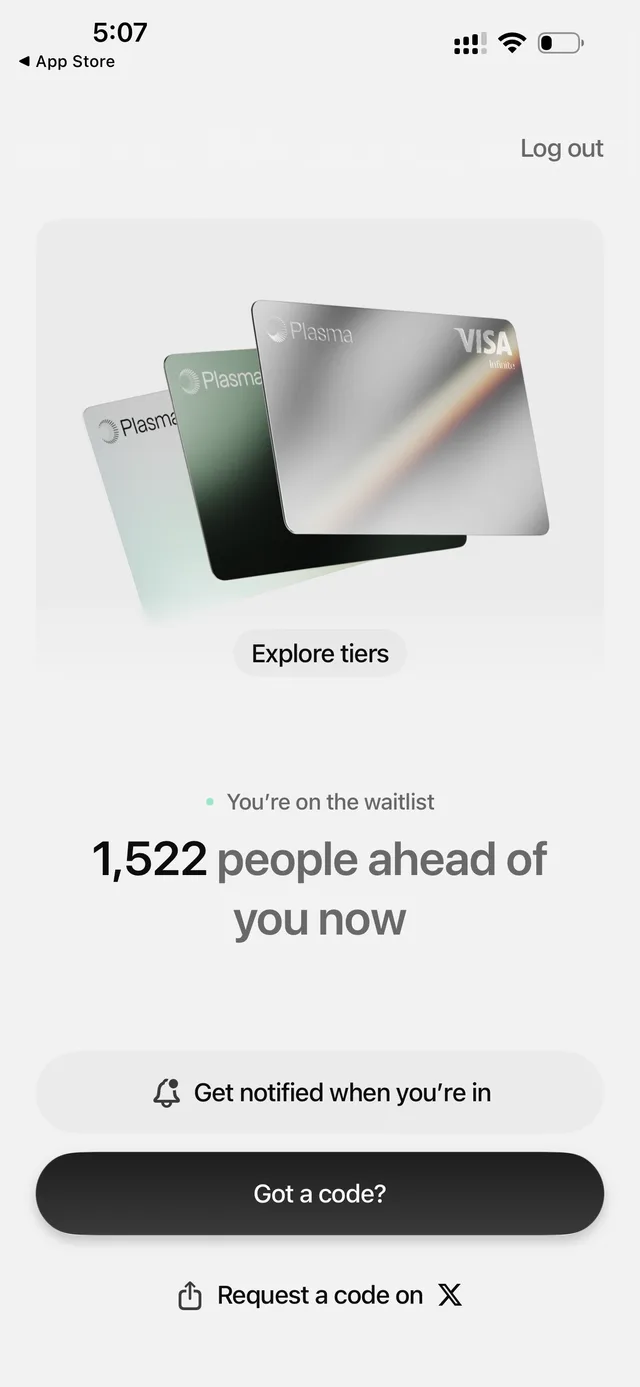

Step 1. Enter the access code. Download the Plasma One app from the App Store or Google Play and enter the code SPESPE at signup. Plasma One still runs a waitlist, and without a code you sit in it. SPESPE skips the queue and takes you straight into onboarding. Core is no longer free; its Google Play launch promotion ended July 18, 2026.

SpendNode app screenshot

This is what a fresh account without a code sees: we signed up in July 2026 and landed 1,522nd in line, with the app offering to notify us "when you're in." Tapping "Got a code?" and entering SPESPE skips the entire queue and drops you straight into onboarding.

Step 2. Install the Plasma One app. The app launched on iOS first, and the Android app went live on Google Play in July 2026. Any modern iPhone, iPad, or Android phone works.

Step 3. Complete KYC. Plasma uses SumSub for identity verification. Expect a standard flow: government-issued ID, selfie liveness check, and address confirmation. Processing time is usually under 30 minutes for clean cases.

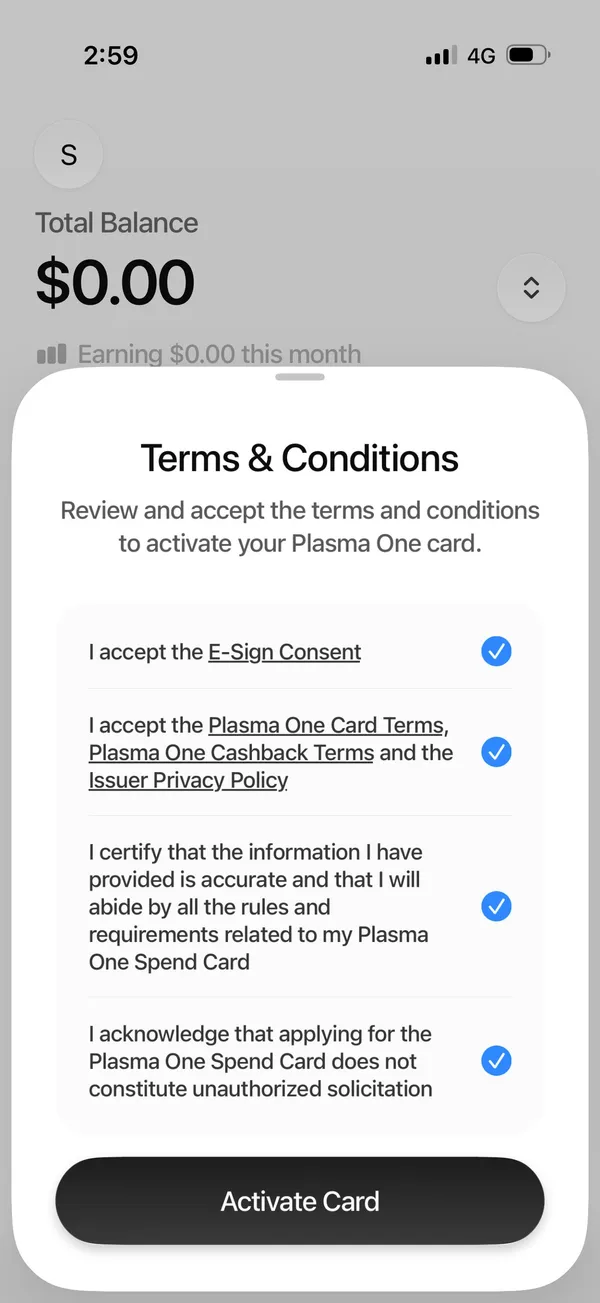

Step 4. Accept the card terms and activate. On the Card tab, tap "Activate Card." Review and accept the E-Sign Consent, the Plasma One Card Terms, the Plasma One Cashback Terms, and the Issuer Privacy Policy. Confirm with "Activate Card" at the bottom of the modal. The virtual card is created instantly.

SpendNode app screenshot

Activation modal - All four toggles must be accepted before the virtual card is issued. The "Plasma One Spend Card" label confirms the legal product name in the Card Terms is "Plasma Spend Card" even though the marketing name is "Plasma One Card."

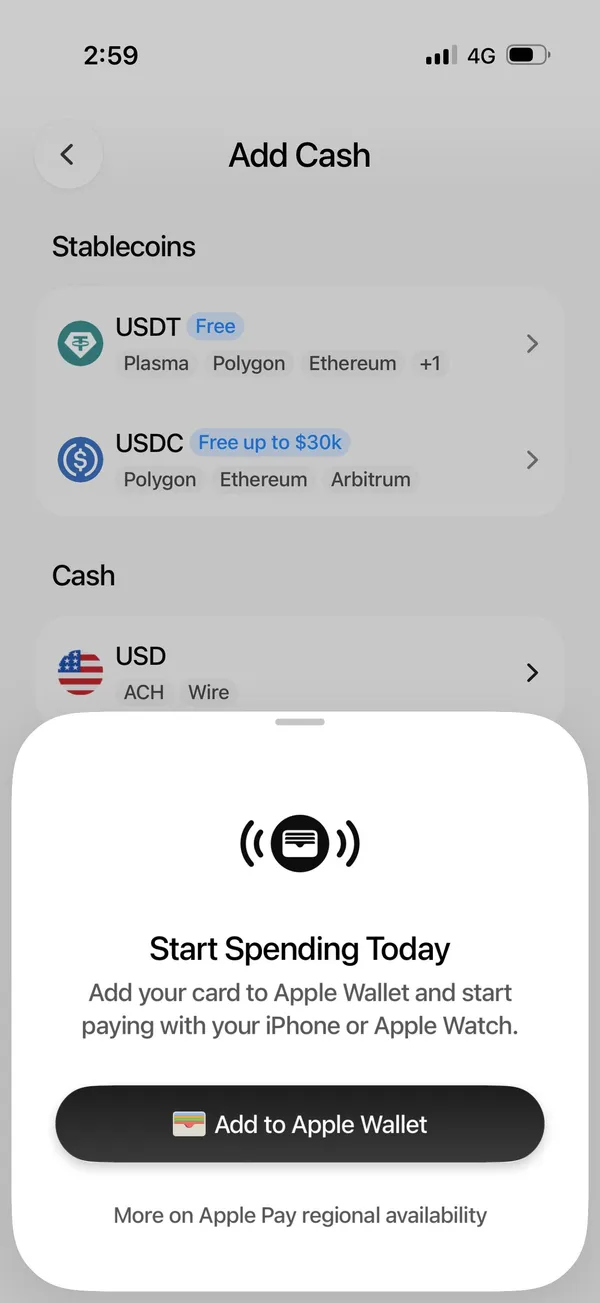

Step 5. Add to Apple Wallet (and fund). A prompt offers to add the virtual card to Apple Wallet for tap-to-pay on iPhone and Apple Watch. Then go to "Add Cash" to fund the wallet. The cleanest free option is USDT on the Plasma chain (free) or USDC on Polygon/Ethereum/Arbitrum (free up to $30,000). USD ACH and wire deposits are also supported.

SpendNode app screenshot

Add Cash funding routes - USDT funding is free across four chains. USDC is free up to $30,000 on three chains. USD ACH and wire deposits are also available. The Apple Wallet prompt provisions the virtual card directly for tap-to-pay.

Step 6. Set your daily limit and start spending. Open the in-app daily limit setting and choose $1,000, $5,000, $10,000, or Custom. The default is $5,000. Cashback in XPL is paid weekly, on Thursdays, visible on the Rewards tab. Optionally, allocate idle stablecoin balance to the Earn vault, which displays the live APY and accrues yield in real time with no lockup.

Countries and Availability

Plasma One is available in 166 countries as of August 2026. We count a country here when at least one active Plasma One card variant lists it, so individual product pages may be narrower.

Available Regions

Africa

Algeria (DZ), Angola (AO), Benin (BJ), Botswana (BW), Burkina Faso (BF), Burundi (BI), Cameroon (CM), Cape Verde (CV), Chad (TD), Comoros (KM), Congo (CG), Djibouti (DJ), Egypt (EG), Equatorial Guinea (GQ), Eswatini (SZ), Ethiopia (ET), Gabon (GA), Gambia (GM), Ghana (GH), Kenya (KE), Lesotho (LS), Madagascar (MG), Malawi (MW), Mauritania (MR), Mauritius (MU), Morocco (MA), Mozambique (MZ), Namibia (NA), Niger (NE), Nigeria (NG), Rwanda (RW), Sao Tome and Principe (ST), Senegal (SN), Seychelles (SC), Sierra Leone (SL), South Africa (ZA), Tanzania (TZ), Togo (TG), Tunisia (TN), Uganda (UG), Zambia (ZM)

Americas

Antigua and Barbuda (AG), Argentina (AR), Bahamas (BS), Barbados (BB), Belize (BZ), Bolivia (BO), Brazil (BR), Canada (CA), Cayman Islands (KY), Chile (CL), Colombia (CO), Costa Rica (CR), Dominica (DM), Dominican Republic (DO), Ecuador (EC), El Salvador (SV), Grenada (GD), Guatemala (GT), Guyana (GY), Honduras (HN), Jamaica (JM), Mexico (MX), Panama (PA), Paraguay (PY), Peru (PE), Puerto Rico (PR), Saint Kitts and Nevis (KN), Saint Lucia (LC), Saint Vincent and the Grenadines (VC), Suriname (SR), Trinidad and Tobago (TT), Turks and Caicos Islands (TC), United States (US), Uruguay (UY)

Asia

Armenia (AM), Azerbaijan (AZ), Bahrain (BH), Bhutan (BT), Brunei (BN), Cambodia (KH), Georgia (GE), Hong Kong (HK), Indonesia (ID), Japan (JP), Jordan (JO), Kazakhstan (KZ), Kuwait (KW), Kyrgyzstan (KG), Laos (LA), Macau (MO), Malaysia (MY), Maldives (MV), Mongolia (MN), Oman (OM), Pakistan (PK), Philippines (PH), Qatar (QA), Saudi Arabia (SA), Singapore (SG), South Korea (KR), Sri Lanka (LK), Taiwan (TW), Tajikistan (TJ), Thailand (TH), Timor-Leste (TL), Turkmenistan (TM), United Arab Emirates (AE), Uzbekistan (UZ)

Europe

Albania (AL), Andorra (AD), Austria (AT), Belgium (BE), Bulgaria (BG), Croatia (HR), Cyprus (CY), Czech Republic (CZ), Denmark (DK), Estonia (EE), Finland (FI), France (FR), Germany (DE), Gibraltar (GI), Greece (GR), Guernsey (GG), Hungary (HU), Iceland (IS), Ireland (IE), Isle of Man (IM), Italy (IT), Jersey (JE), Latvia (LV), Liechtenstein (LI), Lithuania (LT), Luxembourg (LU), Malta (MT), Moldova (MD), Monaco (MC), Montenegro (ME), Netherlands (NL), North Macedonia (MK), Norway (NO), Poland (PL), Portugal (PT), Romania (RO), Serbia (RS), Slovakia (SK), Slovenia (SI), Spain (ES), Sweden (SE), Switzerland (CH), United Kingdom (GB)

Oceania

Australia (AU), Fiji (FJ), Kiribati (KI), Marshall Islands (MH), Micronesia (FM), Nauru (NR), New Zealand (NZ), Palau (PW), Papua New Guinea (PG), Samoa (WS), Solomon Islands (SB), Tonga (TO), Tuvalu (TV), Vanuatu (VU)

Major Restricted Markets

These major markets are not currently listed for this vendor. Confirm eligibility with the issuer before applying, especially where card tiers have different country rules.

Asia

China (CN), India (IN), Turkey (TR)

Plasma does not publish a single fixed country eligibility list for opening an account. Eligibility is confirmed at signup through SumSub KYC, and the service is unavailable to OFAC-sanctioned individuals and entities.

Some app features have their own geographic limits: the Earn vault is not available to New York State residents or other restricted jurisdictions, independent of card eligibility. Because terms can vary by region, the activation screens at signup are the authoritative source for your jurisdiction.

Plasma One vs Other Cards

Plasma One is one of the more credible self-custodial Visa lineups in 2026. Each competitor tackles the same architecture from a different angle.

-

vs Tuyo: Same wallet-collateral / Visa-rails model. Tuyo runs on Base only with no live cashback rate (TUYO points toward a 2026 TGE). Plasma One runs on its own purpose-built chain with live cashback today across three tiers and seven funding routes against Tuyo's one. Tuyo is further along on operational maturity; Plasma One is earlier but has a more aggressive token-rewards story.

-

vs Avici: Avici is the same secured-credit architecture (USDC collateral, Visa issuer) but offers no cashback. The value proposition is pure self-custody with Visa Signature lounge perks on the upper tier. Plasma One ships actual cashback. Different product priorities.

-

vs Gnosis Pay: EUR-settled, EEA/UK-only, on Gnosis Chain. Plasma One is USD-settled, global Visa acceptance, on Plasma chain. Different geographies, different stablecoin denominations, similar self-custody trust story.

-

vs Jupiter Global: Jupiter is custodial-rails with 4% USDC cashback. Plasma One is self-custodial with 2-4% volatile XPL cashback. Choose Jupiter for stability; Plasma for chain-native exposure.

-

vs Crypto.com and Coinbase: These are custodial alternatives. Both offer more polished apps and stronger fee transparency. Plasma One offers self-custody, which is the entire point of the product category for users who care about it. Crypto.com's top tiers also gate high cashback behind large token stakes, much as Platinum does, but hold your balance custodially.

Is Plasma One Safe?

Plasma One distributes risk across several named counterparties, each with its own terms and its own failure profile. Understanding which one holds what is the right way to think about safety here.

Plasma (Cayman Islands) with subsidiaries Plasma Labs UK Ltd., Plasma US Inc., and Plasma Nederland BV. Operator of the chain and the app. Per its own T&Cs: not a bank, not a money services business, not a virtual asset service provider. Plasma does not custody funds. Cayman governing law applies to disputes.

The card issuer. The cards are issued by Rain, a Visa Principal Member, under a license from Visa. Rain holds the issuing relationship that puts the card on Visa rails; the binding consumer contract for card mechanics is the Plasma One Card Terms.

Bridge. Account-services and fiat on- and off-ramp partner: Bridge Building Inc. for US residents, Bridge Building Sp. z o.o. for the EEA, and Bridge Building Limited elsewhere. Handles ACH, wires, and fiat-stablecoin conversion at the boundary.

Veda Tech Limited (BVI). Earn vault operator. Smart-contract risk lives here. Vault Services have their own terms and are not available in New York State or other restricted jurisdictions.

What happens if any of these fail?

- If Plasma the company shuts down. Your stablecoin balance is in a self-custodial wallet on the Plasma chain. You retain ownership. You would need an alternative interface to interact with the chain, since the chain itself is decentralized and survives. The card stops working immediately.

- If the card issuer terminates the program. The card stops working. Your wallet is unaffected. This is the most common failure mode in crypto-card history: the card program ends, the wallet survives.

- If Bridge has an outage. Fiat deposits and withdrawals pause. Card spending continues. Crypto-only funding routes still work.

- If the Veda vault is exploited. Your Earn allocation is at risk. Stablecoin balance held outside Earn is unaffected.

There is one more exposure unique to the paid tiers: the XPL you lock for Core or Platinum (20,000 or 100,000 XPL) is returned after the term, but you carry full token price risk during the lock. Size it as a token position, not a fee.

The trust math: only Earn-allocated balance, unpaid XPL cashback, and any locked XPL are at real risk in a failure or downturn scenario. Card-spend balance survives because it sits in a self-custodial wallet that no single counterparty can move. That is the structural advantage of the self-custody architecture and the reason this category of product exists.

Is Plasma One a Scam?

No. The signals that a crypto fintech is a scam typically include unverifiable corporate structure, no regulated payment partners, no real KYC, made-up "team" pages, and pump-and-dump token timing. Plasma One has none of those markers.

The corporate structure is verifiable: Plasma is incorporated in the Cayman Islands with named subsidiaries in the UK (Plasma Labs UK Ltd.), the US (Plasma US, Inc.), and the Netherlands (Plasma Nederland BV). The cards are issued by Rain, a Visa Principal Member, under a license from Visa. The fiat and account rails are operated by Bridge, and KYC is handled by SumSub, an established identity-verification vendor.

The card itself works as advertised. In our hands-on testing, USDT funding settled in minutes, card transactions ran cleanly over Visa rails, and cashback in XPL pays weekly, on Thursdays. The Earn vault ran at 3.93% APY against the marketed "up to 5%" and let us withdraw on demand.

Real risks exist, but they are different from scam risks. XPL is a volatile token, and the dollar value of cashback drops if XPL drops. The Earn vault carries smart-contract risk at Veda's level. The paid tiers require locking XPL for a year. The chain is young. These are product and counterparty risks, not scam markers, and the page assumes a reader who can weigh them.

Who Should Use Plasma One?

Plasma One fits you if you hold USDT or USDC across multiple chains and want a card you can fund from any of them without bridging first, and if you want a self-custodial Visa where idle balance earns yield and spending earns chain-native cashback in the same app. It suits people who are comfortable holding XPL as the denomination for their rewards and who want exposure to the Plasma chain through a useful spending product rather than through token-buying alone.

The free Lite tier fits moderate everyday spenders; Core fits AI-heavy spenders who would use the ChatGPT Go rebate; and Platinum fits XPL holders and high or travel-heavy spenders who can lock 100,000 XPL for a year.

It is a weaker fit if you need stable USD-equivalent cashback, where Jupiter Global pays 2% in USDC (4% via referrals) with no token risk; if you rely on ATM access, since Plasma One does not publish ATM withdrawal terms (Core and Platinum now include a physical card, while Lite stays virtual-only); or if you require a single published country eligibility list before applying.

The distinctive part is the token loop: card spending pays cashback in XPL, and stablecoin transfers on the chain settle in XPL, so retail use feeds ongoing demand for the asset the chain runs on. If you want exposure to that loop through a card you actually spend with, Plasma One is built for it.

Sources and Verification

Tier specifications confirmed against Plasma's official site, June 2026. Card mechanics, fees, limits, and product flow verified via the Plasma One Card Terms and hands-on testing of the Plasma One platform. Cashback pays weekly (on Thursdays) per Plasma's terms; Earn yield (3.93% at observation) was observed in testing.

Plasma One Crypto Card Monthly Volume

Real card activity measured from onchain settlement data. Not self-reported.

- Card spend (Jul 2026)

- $15.2M

- Card transactions

- 109.4K

- Active wallets

- 16.4K

- Month over month

- +69.1%

| Month | Card spend | Card transactions | |

|---|---|---|---|

| Aug 2026partial | $2.2M | 18.6K | |

| Jul 2026 | $15.2M | 109.4K | |

| Jun 2026 | $9.0M | 71.4K | |

| May 2026 | $3.4M | 16.4K | |

| Apr 2026 | $766K | 3.8K | |

| Mar 2026 | $1.1M | 851 | |

| Feb 2026 | $259K | 290 | |

| Jan 2026 | $128K | 369 |

Our read: July 2026 finished at $15.2M, up sharply from June's $9.0M, continuing the compounding that started with the June 16 public launch. August is near $2.2M across about 10,000 settling accounts in its opening days.

How this is measured: Daily card-spend settlement batches (USDT0) from Plasma One user accounts into the program settlement address on Plasma chain, read from the chain's public explorer. Each user account settles its cleared card spend in a daily batch, so this measures actual card spend. Months before the June 16, 2026 public launch reflect beta usage. Active wallets are distinct Plasma One user accounts settling card spend per month.

Chains: plasma - Source: onchain data via Dune, analysis by spendnode.io - Updated 2026-08-05

Written by Aleksandar Dukic

Frequently Asked Questions

Are Plasma One crypto cards available in the United States?

Yes. Plasma One crypto cards are available in the United States.

Does Plasma One have an invite code?

Yes. Enter the code SPESPE in the Plasma One app (iOS or Android) at signup. Download the app through SpendNode's Plasma One link and apply the code when you create your account. The code skips the waitlist.

Is the SPESPE code for Plasma One working in August 2026?

Yes. SPESPE is still a working Plasma One code as of August 11, 2026 - we re-verify it daily. It skips the waitlist.

Is Plasma One a bank?

No. Plasma is a financial technology company, not a regulated bank or money services business. The card is issued by Rain, a Visa Principal Member, under a license from Visa. Global account services are powered by Bridge (Bridge Building Inc. for US residents, Bridge Building Sp. z o.o. for the EEA, and Bridge Building Limited elsewhere).

Your stablecoin balance is owned and custodied by you, not by Plasma. Stablecoin balances are not bank deposits and are not FDIC insured.

What are the three Plasma One tiers?

Lite is free and earns 2% base cashback. Core costs $199/year or a 20,000 XPL twelve-month lock and earns 3% base, with 5% on AI spend, plus a ChatGPT Go rebate of up to $8/month. Platinum requires locking 100,000 XPL for 12 months and earns 4% base, 10% on AI spend, and 10% on eligible flights, plus travel perks and a boosted 5% yield on the first $500,000 of balance.

All cashback is paid in XPL; the base rate tapers by monthly spend band (Core: 3% on the first $1,000, then 2%, 1%, and 0.25%; Platinum: 4% on the first $3,000, then 3%, 2%, and 1%) rather than a flat cap.

User Reviews

Reviews are moderated and may take a moment to appear.

Latest Page Changes to the Plasma One Review

- Plasma One repriced the Core tier: $199/year (up from $120) or a 20,000 XPL twelve-month lock (up from 10,000 XPL). The launch-window free first year has ended

- Plasma One went live with a three-tier card lineup: Lite (free), Core, and Platinum, replacing the single card. Each step up raises cashback and adds perks

App Store (60 ratings)

Source: Apple App Store - Updated Jul 2026