SpendNode Rating

Kolo stands out because the proposition is still easy to understand. The harder question is how much trust to place in a rewards story that has shifted over time.

Kolo's current public story is 2% BTC cashback, $0 annual, and 0% FX on stablecoins. That still makes it interesting as a free global spend card, but it is no longer the easy outlier the old 5% framing suggested. Where Kolo still needs to grow is on the trust and operational side, especially after the public rewards positioning changed.

Also relevant for Rewards / Cashback.

Cost Efficiency

4.2

Product Utility

4.0

Custody & Trust

3.6

Reliability & UX

3.7

Transparency

3.7

CASHBACK

Verified

NO ANNUAL FEE

Verified

NO FX FEE

Verified

Our Official Verdict

Earn Bitcoin on Purchases: 2% BTC Cashback + Visa Platinum + 170+ Countries

The Kolo Card currently markets 2% cashback in Bitcoin with Free annual fee. With 0% FX on stablecoins and Visa Platinum acceptance in 170+ countries, it is positioned as a simple spend-and-stack-Bitcoin card. Public reward details have shifted over time, so the live headline should carry more weight than older marketing captures.

Fees & Charges

Annual Fee

Free

FX Fee

0%

ATM Fee

TBD

Requirements

Supported Regions

GLOBAL

Spendable Assets

USDT, USDC, DAI, EURC, EURI, BTC, ETH, SOL, BNB, LTC, DOGE, TRX, ARB, PEPE

On This Page

What Is the Kolo Card?

The Kolo Card is a custodial virtual prepaid Visa Platinum card designed for crypto-funded spending. It supports Apple Pay and Google Pay, stablecoin spending with 0% Kolo markup on USDT, USDC, and EURC, and broad availability across 170+ countries outside the US and sanctioned jurisdictions. Kolo's homepage cites 10 million users worldwide.

Card services are provided by Hardline Holdings Limited (Kazakhstan, Astana Financial Services Authority) in collaboration with Signify Holdings Inc. and Raincards. Crypto-asset services migrated to BURVIX SP. Z O. O. (Poland) on 1 January 2026, replacing the previous Cryppo UAB Lithuanian VASP arrangement. Kolo is marketed as MiCA-ready and Travel Rule aligned.

The key correction is rewards. Kolo's current public homepage markets 2% BTC cashback. Older app captures and older SpendNode copy used a richer 5% BTC framing, but that no longer matches the live homepage. Since Kolo's Terms of Use (v2.1, 31 December 2025) also reserve the right to change reward rates and limits at any time, the current 2% public claim is the safest figure to use.

SpendNode app screenshot

Current positioning: Visa Platinum, Apple Pay and Google Pay, exchange-level rates, SEPA transfers, and broad country coverage.

What We Can Still Verify Cleanly

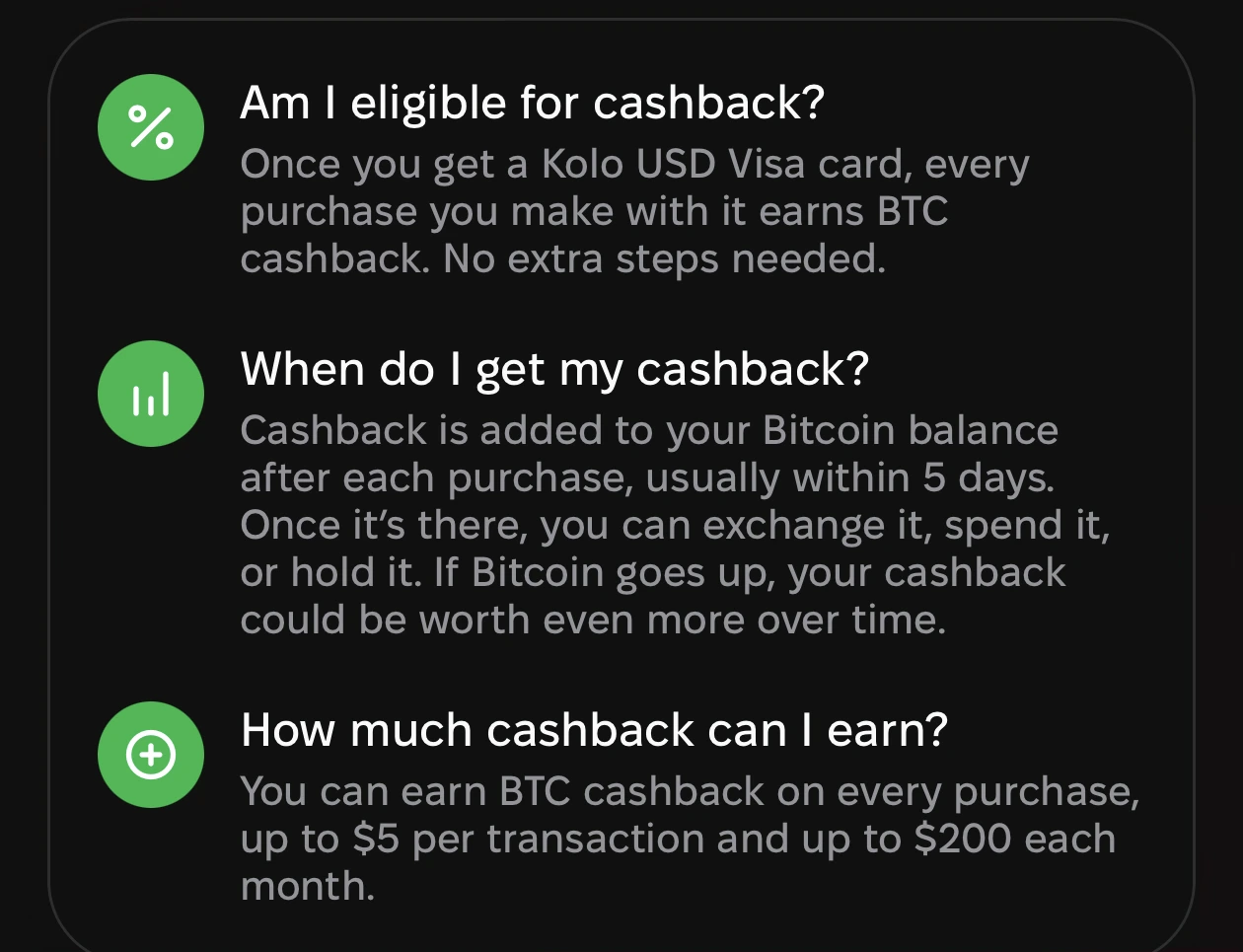

- Reward headline: 2% BTC cashback on the live homepage

- Annual fee: $0

- Activation: 10 USDC, returned back to card balance

- Stablecoin markup: 0% on USDT, USDC, and EURC

- Card type: virtual prepaid Visa Platinum

- Wallet rails: 7 blockchain networks (Ethereum, BNB Chain, Arbitrum, Base, Solana, Stellar, Polygon)

- Onboarding: Telegram mini-app or mobile app with Sumsub KYC

- SEPA bank send: direct crypto-to-fiat send from wallet to Revolut, Wise, N26, or any SEPA bank account

- Regulatory: MiCA-ready, Travel Rule aligned, Polish VASP via BURVIX SP. Z O. O. from 1 January 2026

Fees and Rates

| Fee | Current Positioning |

|---|---|

| Annual fee | $0 |

| Monthly fee | $0 |

| Activation fee | 10 USDC returned to balance |

| USDT / USDC / EURC conversion | 0% Kolo markup |

| Other crypto conversion | spread applies |

| Non-USD purchases | network FX rate still applies |

| ATM withdrawal | N/A (virtual card) |

This means Kolo still works best as a stablecoin spending card first and a BTC reward card second. Once the cashback rate dropped from the old 5% story to the current 2% headline, the spend-rail economics became more important than the reward headline.

The SEPA bank send feature is the other piece that holds up at 2%. Being able to move EUR from a crypto wallet directly to a European bank account without routing through an exchange is not something most free prepaid crypto cards offer. For EEA users and anyone sending money to euro-bank recipients, that rail is a real reason to keep Kolo in the toolkit even if the cashback is no longer market-leading.

Rewards on This Tier

The current public story is simple:

- Current homepage claim: 2% BTC cashback

- Reward asset: BTC

- Terms: Kolo may modify or discontinue reward rates, eligible transactions, and limits at its discretion

What we are not doing anymore is presenting the older 5% structure as the active default. Earlier in-app captures may still reflect a previous reward design, but the homepage is the freshest public source.

SpendNode app screenshot

Important context: this older capture does not override the newer public homepage claim.

How This Tier Compares

- vs Bleap: Bleap is cleaner for self-custody users. Kolo remains broader geographically and simpler if you just want a prepaid card that works.

- vs Crypto.com: Crypto.com still ties stronger rewards to deeper ecosystem commitment. Kolo is lower-friction, but the current 2% rate means the comparison is now closer.

- vs KAST: KAST remains more points-oriented. Kolo is easier to understand if you want direct BTC rewards.

- vs RedotPay: RedotPay is still more about utility rails than BTC accumulation. Kolo still has the cleaner Bitcoin reward angle.

Who Should Choose This Tier

Use Kolo Card if:

- you want a global prepaid crypto card with low stablecoin spend friction

- you want BTC rewards without a paid plan

- you value Apple Pay / Google Pay and broad country coverage

- you are comfortable using a custodial wallet for day-to-day spend balances

Skip Kolo Card if:

- you want self-custody

- you want a physical card or ATM usage

- you only considered it because of old 5% cashback references

- you need a reward program with clearer long-term public consistency

Safety and Trust

Kolo still carries the same trust tradeoffs it had before:

- custodial setup

- smaller operator footprint than top-tier exchange brands

- rewards program terms written with broad operator discretion

So the sensible posture is unchanged:

keep only active spending balances here, not long-term holdings.

Bottom Line

The Kolo Card remains relevant, but the thesis is narrower than our old copy suggested.

The strongest current case is:

- zero annual fee

- broad global coverage

- stablecoin-friendly spending

- BTC rewards without staking

The weaker case is the one we are retiring:

- treating Kolo as a live verified 5% BTC cashback product

Until Kolo publishes a richer reward structure again, the current public figure to trust is 2% BTC cashback.

Sources and Verification

- Kolo Official Site

- Kolo Terms of Use

- Internal homepage and app captures reviewed on April 10, 2026

FAQ

How do you choose Kolo Card crypto cards?

We compare verified issuer sources, fees, and eligibility. Availability can change, so confirm with the issuer before applying.

Do all cards in this list offer the same benefits?

No. Each issuer defines its own program terms. Review the sources on each card profile.

Are these rankings or recommendations?

No. Lists are filtered views of cards in our database and do not imply rankings.

This is a prepaid card. Merchants that require pre-authorization holds (gas stations, hotels, car rentals, toll booths) may decline it. Fund only what you plan to spend.

Your funds are held by Kolo. If the provider faces insolvency, your balance may be at risk. This card does not offer self-custody protection.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?

User Reviews

Reviews are moderated and may take a moment to appear.

Recent Updates to Kolo Card

- Corrected the stale Kolo reward framing to the current public 2% BTC cashback headline instead of the older 5% positioning

- Rewrote the card review around current public claims and removed the old capped-5%-BTC comparison logic