COCA is a self-banking super app offering a non-custodial Visa debit card (not a credit card) issued by Wirex, with up to 8% stablecoin cashback within monthly allowance (1% after) across six staking tiers (Starter through Elite), 0% FX fees, 6% APY on stablecoin balances via Morpho lending markets (tier-based caps from $5K to unlimited), 50% subscription rebates across four categories (Video Streaming, AI Assistants, Music, Marketplaces) scaling by tier with $70/mo cap per service, personal IBAN with SEPA transfers, $200/month free ATM withdrawals, and smart contract wallet security powered by Privy (ERC-4337/EIP-7702), available in 70 countries with 1M+ users globally.

Curve Integration Update (Feb 2026): COCA is continuing to support Curve and is not discontinuing the integration. Until March 31, Curve transactions remain eligible for full cashback under your current tier. Starting April 1, cashback on Curve transactions moves to 1% for all users regardless of tier, with no limits.

COCA Visa Card - Non-custodial Visa debit with up to 8% cashback, 50% subscription rebates, and 6% APY via Morpho. Issued by Wirex, available in 70 countries.

The Self-Banking Challenger With the Deepest Feature Set

We verified the claims against every crypto card program in 2026, and COCA's "self-banking super app" label - the feature list backs it up. Up to 8% cashback within monthly allowance ($1K-$10K by tier, 1% after), 0% FX fees, 6% APY on stablecoin balances, 50% subscription rebates across four categories scaling by tier, up to 50% hotel discounts, personal IBAN with SEPA transfers, and Apple Pay/Google Pay - all from a single non-custodial wallet. No other crypto card in 2026 combines this many reward streams in one product.

The architecture is genuinely different from exchange-linked cards. COCA uses Privy-powered smart contract wallets (ERC-4337/EIP-7702) where you control your funds. The yield comes from Morpho lending markets managed by Gauntlet, not from COCA subsidizing rates. The card is issued by Wirex (FCA-regulated UK, licensed EEA). Over 1M users globally across 70 countries.

The catch remains the $COCA token. Maximum benefits require staking 30,000 $COCA for Elite tier, a small-cap token trading on MEXC, BitMart, and DEXes. Staked tokens are locked for the duration of your tier membership, and unstaking requires cancelling your tier followed by a 30-day cooldown. We recommend starting at Starter tier (zero staking needed): 1% cashback, 0% FX, and 6% APY on balances up to $5K is a competitive baseline. The gap between Starter and Elite is where the risk-reward calculation lives.

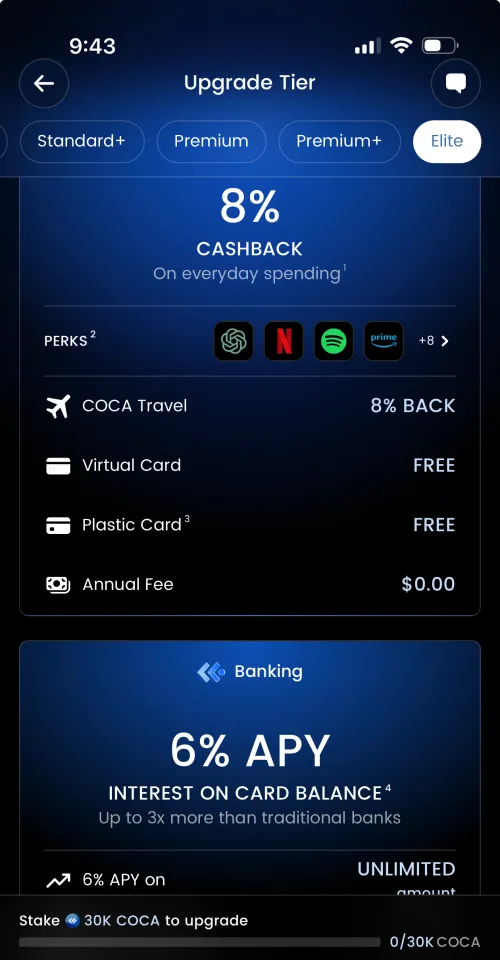

The Card: One Product, Six Tiers

COCA Visa Card - Non-custodial Visa debit card. Tiers require staking $COCA tokens (locked during membership, 30-day cooldown to unstake after cancellation). Card issued by Wirex.

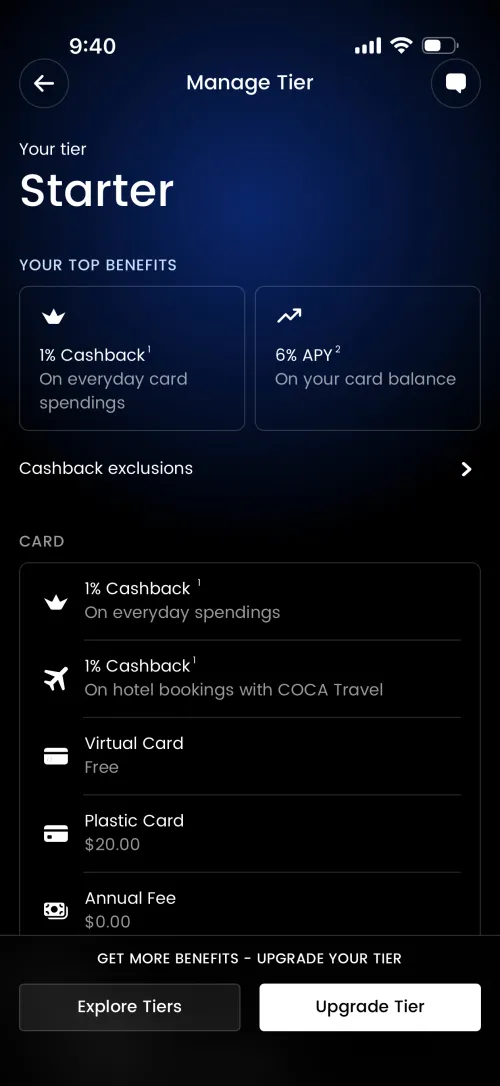

Starter Tier - No tokens required. 1% cashback, 6% APY, free virtual card. The baseline tier for testing COCA's card, IBAN, and yield stack without adding token exposure.

| Tier | $COCA Staked | Cashback | Monthly Allowance | APY Cap | Plastic Card |

|---|---|---|---|---|---|

| Starter | 0 | 1% | - | $5K | $20 |

| Standard | 300 | 3% | $1,000 | $50K | $20 |

| Standard+ | 1,000 | 4% | $1,750 | $250K | $20 |

| Premium | 3,000 | 5% | $2,500 | $500K | Free |

| Premium+ | 10,000 | 6% | $5,000 | Unlimited | Free |

| Elite | 30,000 | 8% | $10,000 | Unlimited | Free |

All tiers: $0 annual fee, free virtual card, 6% APY up to tier cap (2% above cap), 0% FX fees, 0% trading fees, free cross-chain swaps. Above monthly allowance, all purchases earn 1%. Premium/Premium+/Elite get 100% card issue fee rebate (delivery not included).

Elite Tier - 8% cashback on first $10,000/mo, all subscription rebates across 4 categories, unlimited 6% APY. Requires staking 30,000 $COCA tokens (30-day cooldown to unstake).

Subscription rebates scale by tier and category. Standard gets 1 service from Video Streaming (Netflix, Disney+, Paramount+, YouTube Premium). Standard+ and Premium add AI Assistants. Premium+ adds Music. Elite adds Marketplaces. Each category allows one subscription at 50% back, $70/mo cap per service. Starter gets none.

Fee Structure: The Numbers

| Fee | Cost | Notes |

|---|---|---|

| Annual fee | $0 | All tiers |

| FX fee | 0% | Zero FX fees on all currencies |

| ATM withdrawals | $200/month free | 2% on amounts above $200 |

| ATM daily limit | 850 EUR | Max 5 transactions/day |

| ATM monthly limit | 5,000 EUR | |

| Virtual card | Free | All tiers |

| Physical card | $20 | Free for Premium/Premium+/Elite |

| Trading fee | 0% | Commission-free |

| Cross-chain swaps | Free |

Purchase limits: 30,000 EUR per transaction, 30,000 EUR/day, 30,000 EUR/month, 75,000 EUR/quarter, 100,000 EUR semi-annually.

COCA charges 0% FX on all currencies. Combined with $0 annual fee, free virtual card, and $200/month free ATM withdrawals, COCA has one of the cleanest fee structures in the crypto card space. The zero FX model means cashback rate equals net return regardless of which currency you spend in.

Technology: Privy Smart Wallets + Morpho Yield

COCA's architecture is built on three pillars:

1. Privy Non-Custodial Wallets (ERC-4337/EIP-7702)

- Smart contract wallets where you control the keys - COCA cannot move your funds

- Privy handles key management: SOC 2 Type I and Type II certified, audited by Cure53, Zellic, and Doyensec

- Biometric recovery (no seed phrase needed, though private key export is available)

- Card payments use authorization-based spending: each transaction approves only the specific amount for that specific merchant

- Apple Pay and Google Pay integration

2. Morpho + Gauntlet APY Engine

- 6% APY generated from Morpho on-chain lending markets (not COCA subsidizing rates)

- Gauntlet provides risk management: curated allocations, supply caps, ongoing monitoring

- Interest calculated on minimum monthly card balance (minimum $1 required), paid by the 10th of the following month in stablecoins

- This is real DeFi yield from borrowing demand, not promotional rates

3. IBAN Banking Layer

- Personal IBAN for SEPA bank transfers in EUR (USD where available)

- Receive salary directly to COCA

- Send/receive money like a regular bank account

- Top up via bank transfer, debit/credit card, or stablecoins

Supported assets: USDC, USDT, ETH, BTC, plus popular coins via the Crypto Account.

Trust, Security, and Regulation

Card issuer: Wirex Limited (FCA-regulated, UK) and UAB Wirex (licensed, EEA). Prepaid card program with Visa network. PCI DSS and ISO compliant. 3DS for online transactions. Freeze/unfreeze in-app.

Wallet security: Privy non-custodial infrastructure. SOC 2 Type I and Type II certified. Third-party audits by Cure53, Zellic, and Doyensec. Bug bounty program. Private key export available (irreversible - you lose COCA wallet access).

Self-banking model: COCA cannot access, freeze, or move your funds. Each card transaction requires your wallet's authorization for the specific amount. This is fundamentally different from custodial exchange cards (Crypto.com, Bybit) where the exchange holds your balance.

What is NOT protected:

- $COCA token value (small-cap, volatile)

- APY rates (DeFi market-dependent, adjusted to stay sustainable)

- Subscription rebates (subject to COCA's partnerships)

- Platform risk: if COCA shuts down, Privy key reconstruction may be complex (you can export private keys as a precaution)

COCA stability indicators (reviewing as of 2026):

- 1M+ users globally

- Product Hunt #1 Product of the Day

- CONF3RENCE 2024 "Next Financial Revolution" winner

- Card issued through Wirex (established 2014)

- No App Store native app listing yet (web/PWA)

Availability: 70 Countries

UK and Europe (40): Andorra, Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Germany, Gibraltar, Greece, Guernsey, Hungary, Iceland, Ireland, Isle of Man, Italy, Jersey, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Moldova, Monaco, Montenegro, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Switzerland, United Kingdom.

Asia-Pacific (16): Australia, Azerbaijan, Georgia, Hong Kong, Indonesia, Japan, Kazakhstan, Macao, Malaysia, New Zealand, Philippines, South Korea, Taiwan, Thailand, Uzbekistan, Vietnam.

Middle East and Africa (6): Bahrain, Ghana, Kenya, Nigeria, Saudi Arabia, UAE.

Latin America (8): Argentina, Brazil, Chile, Colombia, Ecuador, El Salvador, Mexico, Peru.

Passport from almost any country accepted for card ordering; availability depends on residence in one of the 70 supported countries.

How COCA Compares

| Feature | COCA | Crypto.com | Plutus | KAST |

|---|---|---|---|---|

| Max Cashback | 8% (Elite) | 5% CRO (Private) | 9% PLU | 4% MOVE |

| Free Tier Rate | 1% | 0% | 3% | 2% |

| FX Fee | 0% | 0-2% | 0% | 0% |

| Token Requirement | Stake (30-day cooldown) | Stake (180 days) | Stacking | None |

| APY on Balance | 6% (Morpho) | 0% | 0% | 0% |

| Sub Rebates | 50% (4 categories, by tier) | 100% (select) | 100% (select) | None |

| IBAN/Banking | Yes (SEPA) | Yes | No | No |

| Custody | Non-custodial (Privy) | Custodial | Non-custodial | Custodial |

| Countries | 70 | 70+ | 31 (EEA/UK) | 170+ |

After comparing every alternative:

COCA wins on: High cashback (up to 8% within monthly allowance) with 0% FX fees, 6% APY on balances (unique among card programs), personal IBAN/SEPA banking, category-based subscription rebates (up to 4 categories at Elite), and non-custodial architecture with audited security.

COCA loses on: $COCA is a small-cap token (higher token risk than CRO or PLU), staked tokens are locked with 30-day cooldown (not instantly liquid like claimed previously), no native App Store listing yet, newer platform with shorter track record, monthly allowance caps limit cashback at higher spend levels, and Privy key recovery depends on COCA infrastructure (not fully self-sovereign like Gnosis Pay).

Who Should Use COCA in 2026?

Ideal user profile:

- Wants a crypto-native bank replacement (card + IBAN + yield + swaps in one app)

- Values non-custodial control with bank-grade UX (no seed phrase hassle)

- Holds stablecoin balances and wants 6% APY alongside card rewards

- Uses eligible subscription services (Netflix, ChatGPT, Spotify, Amazon depending on tier)

- Spends in any currency with 0% FX fees

- Lives in one of the 70 supported countries

Who should avoid:

- Risk-averse users uncomfortable with small-cap $COCA token exposure at higher tiers

- Users who want established, battle-tested platforms - use Crypto.com (8+ years) or Plutus (6+ years)

- Users who need true seed-phrase self-custody - use Gnosis Pay (Safe wallet) or Ledger CL

- Users in countries outside the 70 supported markets

Final take: Our review finds that COCA remains the most feature-dense crypto card available in 2026. Up to 8% cashback (within monthly allowance) + 0% FX + 6% APY + subscription rebates + IBAN banking + non-custodial wallet is unmatched by any single competitor. At Starter tier (zero staking), you get 1% cashback, 0% FX, and 6% APY on up to $5K - competitive with most cards. At Elite tier, 8% cashback on first $10,000/mo delivers the full 8% net on all spending within the allowance. Above the allowance, all tiers drop to 1%. The entire risk-reward calculation hinges on $COCA token exposure: stake zero tokens at Starter and get solid baseline features, or stake $COCA (locked during membership, 30-day cooldown to unstake) and unlock one of the strongest reward packages in crypto.

Fees and ROI framework

$0 annual fee. 0% FX on all currencies. $200/month free ATM (2% above). Six staking tiers: Starter (0) 1%, Standard (stake 300) 3%/$1K allowance, Standard+ (stake 1K) 4%/$1.75K, Premium (stake 3K) 5%/$2.5K, Premium+ (stake 10K) 6%/$5K, Elite (stake 30K) 8%/$10K. Above monthly allowance, 1% cashback. Staked tokens locked during membership, 30-day cooldown to unstake. 6% APY on stablecoin balance up to tier cap ($5K-unlimited, 2% above). 50% subscription rebates by category (Video/AI/Music/Marketplaces) scaling by tier, $70/mo cap per service. At Elite with $3,000/month (within $10K allowance): $2,880 cashback + APY + sub rebates = approx. $3,300+/year. Break-even on token risk depends on $COCA price stability.

Competitor comparison

- vs Crypto.com: Crypto.com offers up to 5% CRO with 180-day staking lockup. COCA offers up to 8% within monthly allowance with staking (30-day cooldown to unstake). COCA wins on higher max cashback, 0% FX, and 6% APY. Crypto.com wins on track record, 100% subscription rebates, airport lounges, and native app.

- vs Plutus: Plutus offers 3-9% PLU with subscription (GBP 6.99-19.99/month, no free tier) and 2.5% FX on non-domestic (EEA/UK only). COCA offers 1-8% within monthly allowance with 0% FX across 70 countries. COCA wins on FX, availability, IBAN, APY, and no subscription fees. Plutus wins on max cashback rate for domestic perk optimizers.

- vs KAST: KAST offers 2-4% MOVE with no token requirement and 0.5-1.75% FX. COCA offers 1-8% within allowance with $COCA staking and 0% FX. KAST wins on zero token requirement and 170+ countries. COCA wins on max cashback, lower FX (0% vs 0.5%), APY, subscription rebates, and IBAN.

- vs Gnosis Pay: Gnosis Pay offers 1-5% GNO with true Safe self-custody and 0% FX. COCA offers 1-8% within allowance with Privy non-custodial and 0% FX. Gnosis wins on true seed-phrase self-custody. COCA wins on higher max cashback (8%), APY, subscription rebates, and IBAN.

Availability and compliance notes

70 countries: Europe (40), APAC (16), MENA (6), LATAM (8). Card issued by Wirex (FCA UK, EEA licensed). Visa network. 0% FX on all currencies. Non-custodial smart wallet powered by Privy (ERC-4337/EIP-7702, SOC 2 certified, audited by Cure53/Zellic/Doyensec). Tiers require staking $COCA (30-day cooldown to unstake). APY via Morpho + Gauntlet. Personal IBAN with SEPA. Apple Pay and Google Pay. PCI DSS and ISO compliant. 3DS for online payments.

Sources and Verification

Frequently Asked Questions

How does $COCA staking work?

Yes, tiers above Starter require staking $COCA tokens. Staked tokens are locked for the duration of your tier membership. To unstake, you must cancel your tier (which downgrades you to Starter), then wait 30 days before claiming your tokens. No partial unstaking is allowed. Starter tier requires zero staking.

What are the 6 tiers and their requirements?

Starter (0 COCA, 1% cashback), Standard (stake 300 COCA, 3%, $1K/mo allowance), Standard+ (stake 1K COCA, 4%, $1.75K/mo), Premium (stake 3K COCA, 5%, $2.5K/mo), Premium+ (stake 10K COCA, 6%, $5K/mo), Elite (stake 30K COCA, 8%, $10K/mo). After the monthly allowance, all purchases earn 1%. All tiers earn 6% APY up to tier cap (2% above).

Who issues the COCA card?

The COCA Visa card is issued in partnership with Wirex. Wirex Limited is FCA-regulated in the UK; UAB Wirex is licensed in the EEA.

Where can I buy $COCA?

Available on MEXC, BitMart, and decentralized exchanges like Uniswap and 1inch via WalletConnect in the COCA app.

How does the APY work?

You earn 6% APY on your stablecoin card balance up to your tier cap (Starter $5K, Standard $50K, Standard+ $250K, Premium $500K, Premium+/Elite unlimited), and 2% APY on any amount above the cap. Interest is calculated on your minimum monthly card balance (minimum $1 required) and paid by the 10th of the following month in stablecoins. Yield is generated via Morpho lending markets with Gauntlet risk management.

Is there an IBAN?

Yes. COCA provides a personal IBAN for SEPA bank transfers in EUR. You can receive salary, send/receive money, and top up your card balance via bank transfer, card top-up, or stablecoins.

Is the COCA Card a credit card?

No. The COCA Card is a non-custodial Visa debit card, not a credit card. You spend from your smart wallet balance - there is no credit line, no APR, and no credit check. For crypto-backed credit card options, see our reviews of Gemini, ether.fi, Nexo, and Avici.

Recent Data Updates for COCA Cards

- 2026-03-21 - COCA: International transaction fees adjusted to 0%.