When Tria opened Season 3 on June 1, 2026, its community split into two camps within hours, on Discord and on X. One side is angry: the cashback that made the card worth carrying just got capped, and the staking boost that once pushed rates toward 8% no longer drives the headline. The other side is shrugging, or even cheering, pointing at the new points-and-mystery-box program and a model that might actually survive past next quarter.

We have a foot in both camps. The downgrade is real and it stings for anyone spending more than a grand a month. But uncapped 4.5% to 6% cashback, funded the way it was, was never a forever number. The real question for existing holders is simple: is Tria still worth keeping in your wallet?

Tria Flips the Switch on Season 3

Season 3 went live on June 1, 2026, and it rewrites the card's core economics. Cashback is no longer a flat rate on everything you spend. It is now capped to a monthly spend threshold per tier, after which it drops to a 1% floor. The TRIA staking mechanic that previously lifted rates is no longer part of the Season 3 rate structure. And the headline attraction is no longer the cashback at all, it is a season-long points race feeding into a set of mystery boxes.

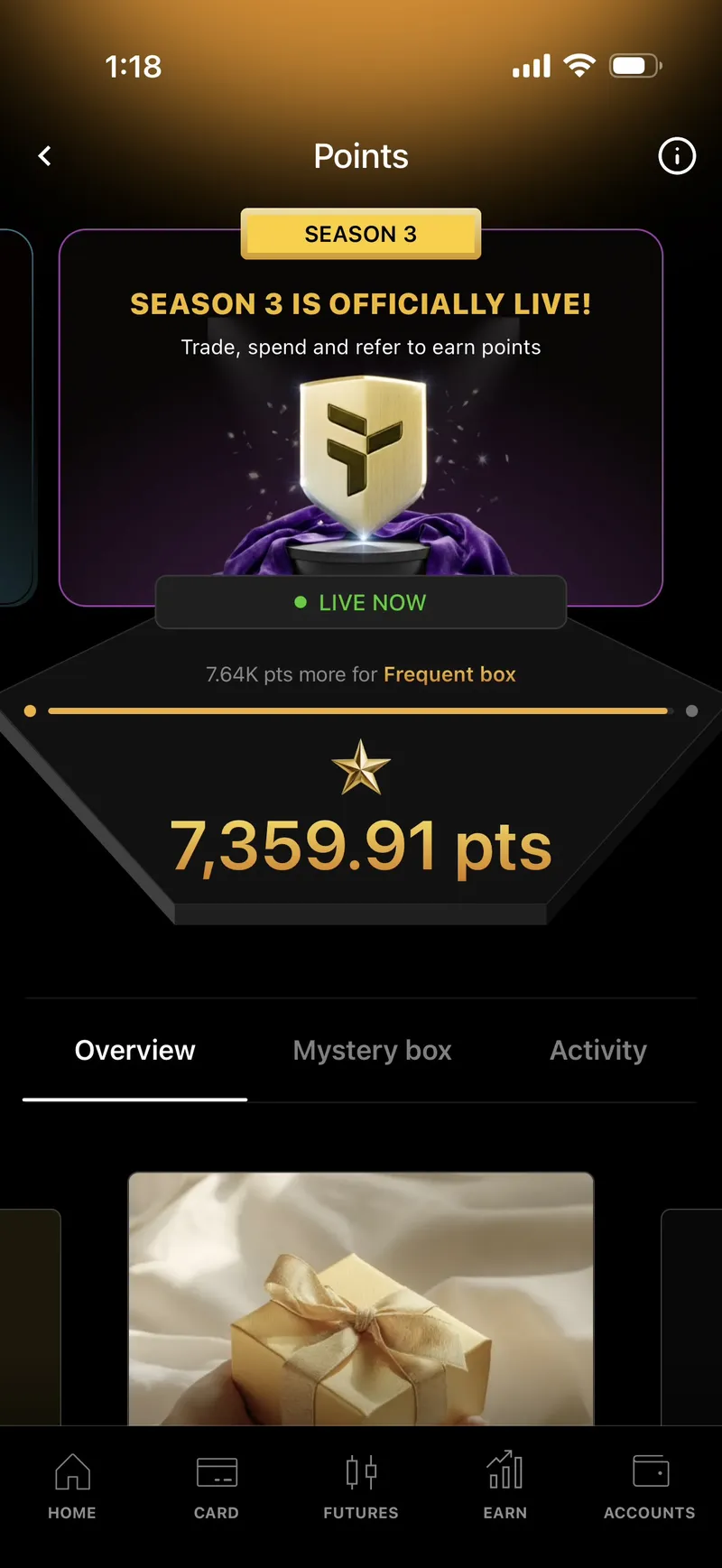

SpendNode app screenshot

Season 3 is open. The app now tracks Season 3 points on every card swipe, with the points-and-mystery-box program front and center where the staking dashboard used to be.

The cashback itself still pays in USDT on Arbitrum, and the self-custody model is unchanged: your keys, account-abstraction wallet, up to 15% APY on idle USDC, 0% FX, and the Visa Signature perks on the paid tiers. What changed is how much of your spend earns the headline rate.

What Actually Got Cut

Three things moved, and only one of them is the part people are mad about.

- Cashback is now capped. Each tier earns its headline rate only up to a monthly spend ceiling, then 1% above it.

- The staking boost has stepped back. Season 3 leads with a flat base rate rather than a "stake TRIA to push your rate higher" kicker, so plan around the base rate.

- The Virtual tier price moved from $20 to $25 a year, though Tria is waiving it for a limited time, so the entry card is effectively free right now.

The new structure by tier:

| Tier | Headline rate | Applies to | Above the cap | Annual fee | Break-even spend |

|---|---|---|---|---|---|

| Virtual | 1.5% | First $100/mo | 0.5% | $25 (free for now) | n/a while free |

| Tria Signature | 4.5% | First $1,000/mo | 1% | $109 | ~$202/mo |

| Tria Premium | 6% | First $2,000/mo | 1% | $250 | ~$347/mo |

The cap is the whole story. If you spend at or under your tier's ceiling, nothing changed: a $1,000/month Signature spender still earns a flat 4.5%. Push past the ceiling and your marginal rate collapses to 1%, which is where the complaints come from. A $5,000/month Premium spender used to earn 6% on the full amount. Now they earn 6% on the first $2,000 and 1% on the remaining $3,000.

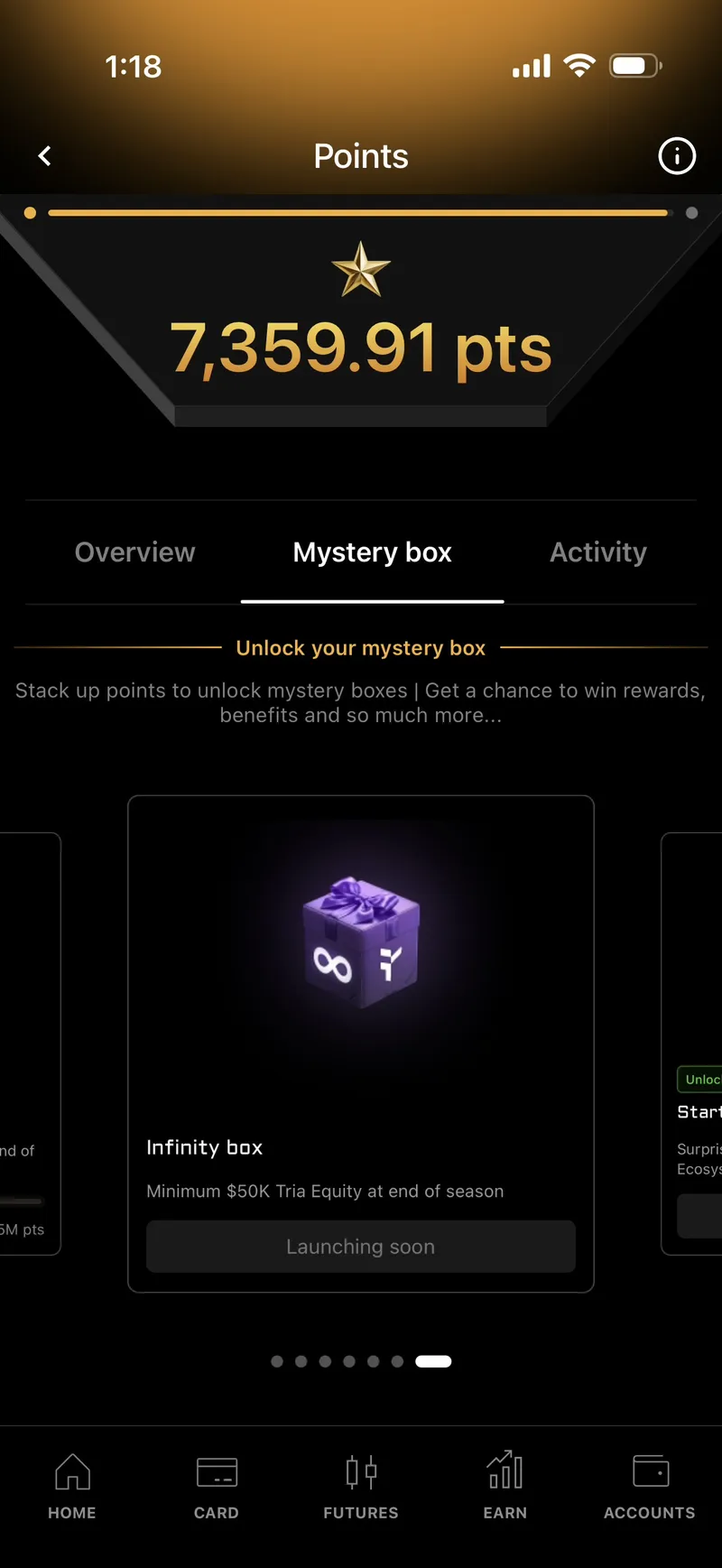

The New Carrot: Points and Mystery Boxes

Season 3's headline mechanic is a points program rather than the old staking boost. Card spend earns points (1 per dollar on Virtual, 1.5 per dollar on Signature and Premium), and points trade nothing until they unlock one of seven ascending mystery boxes. Points are also earnable by trading Decibel or Hyperliquid perps inside the app, separate from card spend.

The lower boxes hold vague surprise rewards: cashback credits, travel credits, ecosystem perks. The higher boxes promise a minimum reward floor plus a draw on Tria equity at season end. The top two are where the lottery framing becomes obvious:

| Box level | What it holds | How you reach it |

|---|---|---|

| Lower boxes | Surprise rewards (cashback, travel, ecosystem) | Modest point totals |

| Higher boxes | Minimum reward floor + Tria equity draw | Heavy spend or perps volume |

| Legendary | Unlocks at 5,000,000 points | Roughly $3.3M of card spend at 1.5 pts/$1 |

| Infinity | Minimum $50,000 in Tria equity at season end | Point threshold undisclosed, whale territory |

Boxes open monthly starting August 31, 2026. For a normal spender, this is a thin lottery ticket layered on top of the cashback. The real economics are still the capped cashback rate, not the boxes. Treat the equity draw as an airdrop-style bonus you do not plan your finances around.

Why We Think the Old Model Was Living on Borrowed Time

Our unpopular opinion: the uncapped rates were a problem waiting to happen.

A self-custody card paying 4.5% to 6% on unlimited spend, with a token-staking kicker on top, is paying out more than the interchange and yield underneath it can sustainably fund. That gap gets covered by token emissions and runway, not by a durable revenue model. Cards that price rewards above their unit economics tend to do exactly what Tria just did: cut, and usually with less warning and worse communication than this.

Capping the headline rate to a monthly threshold is how you keep a rewards program solvent. It concentrates the generous rate on the spend that matters most to a typical user (the first $1,000 to $2,000 a month covers most people's card-eligible spending) while protecting the program from whales who would otherwise drain it on six-figure annual volume. We would rather hold a card that pays 4.5% on the first $1,000 every month for years than one that pays 6% on everything for three more months and then collapses.

That does not make the rollout painless. High spenders are worse off, and "this is healthier for the ecosystem" is cold comfort if you were routing $8,000 a month through a Premium card. But on the structural question, capping was the right call.

So Is Tria Still Worth Carrying?

The answer depends entirely on how much you spend.

At or below the cap, Tria is barely touched. Watch what the cap does to net cashback on Signature as spend climbs:

| Monthly spend | Old (uncapped 4.5%) | New (capped) | Net after $109 fee |

|---|---|---|---|

| $1,000 | $540/yr | $540/yr | $431 |

| $1,500 | $810/yr | $600/yr | $491 |

| $3,000 | $1,620/yr | $780/yr | $671 |

| $5,000 | $2,700/yr | $1,140/yr | $1,031 |

The first row does not move. The gap only opens once you spend past $1,000 a month, and it widens fast. The same pattern holds on Premium past $2,000 a month.

Now the competitive question. At a moderate spend that sits inside the cap, how does Tria stack up against the cards people actually cross-shop it against? Take a $1,000/month spender:

| Card | Rate at $1,000/mo | Annual fee | Net cashback | Edge |

|---|---|---|---|---|

| Tria Signature | 4.5% = $540 | $109 | $431 | 15% APY, 0% FX, Visa Signature perks, self-custody |

| Jupiter Global | 4% = $480 | $0 | $480 | Free, virtual, USDC-native |

| ether.fi Core | 3% = $360 | $0 | $300 (after 1% FX) | Free, borrow-to-spend |

| COCA | 1% free, up to 8% staked | $0 | $120 to $960 | Higher ceiling, but needs token staking |

Read that table honestly and Tria does not win on raw net cashback at moderate spend. A free card like Jupiter Global edges it once you subtract the $109 fee. Where Tria earns its keep is the stack around the rate: up to 15% APY on idle USDC, self-custody, 0% FX, and Visa Signature protections that free cards do not carry. If you value those, the fee is easy to justify. If you only care about the cashback percentage, the cap has made Tria a harder sell than it was a week ago.

The clearest losers are high spenders. Above the cap, the 1% floor puts Tria behind uncapped cards like COCA, Bitget, and ether.fi, which keep paying their full rate on every dollar. If your card spend runs well into five figures a year, Tria is no longer the cashback leader for you, and we would not pretend otherwise.

What Cardholders Should Do Now

A few practical moves depending on where you land:

- Spending under $1,000 a month on Signature (or under $2,000 on Premium)? Do nothing. Your rate did not change, and you keep the self-custody and yield features.

- A heavy spender who chased the old uncapped rate? Run the new math against an uncapped competitor before your next renewal. Past the cap, the 1% floor is beatable.

- Holding for the mystery boxes? Size your expectations. The meaningful boxes are whale-gated, and the equity draw is a lottery, not a yield. Spend for the cashback and treat any box as upside.

- On the Virtual tier? It is free right now. There is little reason to drop it while Tria waives the fee, but understand the 1.5% only covers your first $100 of monthly spend.

Overview

Tria Season 3, live since June 1, 2026, caps cashback to a monthly spend threshold per tier (1.5% on the first $100 for Virtual, 4.5% on the first $1,000 for Signature, 6% on the first $2,000 for Premium), drops to 1% above the cap, steps back from the TRIA staking boost, and adds a points-and-mystery-box program with a season-end Tria equity draw. The Virtual price moved to $25 but is currently waived. Spenders within their cap are unaffected and keep self-custody, up to 15% APY, 0% FX, and Visa perks. High spenders lose the most and should compare against uncapped cards. We think the uncapped model was financially unsustainable, so the cap is a healthier long-term structure even though it lowers the ceiling.