Plutus Visa Card Review 2026

3-9% PLU cashback on eligible spend (Starter £250, Everyday £500, Premium £1,000/month). 50+ perks (£10 rebates). 2.5% FX. Non-custodial stacking. UK/EEA only.

CASHBACK

Verified

APPLE PAY

Verified

GOOGLE PAY

Verified

Our Official Verdict

Non-Custodial PLU Rewards on Eligible Spend + Lifestyle Perks

A Visa debit card for dedicated perk optimizers in the UK/EEA. The 3-9% PLU rewards and 50+ perks remain strong, but the 2026 pricing changes (£6.99-£19.99/month subscriptions, 2.5% non-domestic FX fee) mean you need to maximize eligible spend and domestic perks to break even. Best suited for domestic spenders who actively manage their perk selections - not a travel card.

Fees & Charges

Annual Fee

$240

FX Fee

2.5%

ATM Fee

2.5%

Requirements

Supported Regions

UK, EEA

Spendable Assets

GBP, EUR, PLU

Plutus Visa Card Review

The Plutus Visa Card is a card that functions as a standard Visa debit for fiat spending while connecting to your self-custodial crypto wallet to calculate and distribute PLU rewards based on your stacking tier and perk selections.

Your Daily Crypto Rewards Driver

The Plutus Visa Card is the physical manifestation of Plutus's non-custodial rewards ecosystem. Unlike exchange cards that require you to hold funds on a centralized platform, the Plutus Visa operates on a hybrid model: your spending balance is held as GBP/EUR in a regulated e-money account, while your PLU rewards accumulate based on holdings in your own self-custody wallet.

What this means practically: You load fiat onto the card like any prepaid debit, spend at any Visa merchant, and earn PLU tokens distributed monthly to your connected wallet. The card never touches your crypto - it reads your wallet balance to determine reward rates, then pays you accordingly. Note: with the 2026 fee changes (2.5% non-domestic FX fee), this card is best suited for domestic spending in GBP or EUR.

Card Specs: What You're Actually Getting

Physical & Virtual Cards

Plutus Physical Card - Optional at £9.99. Same balance as virtual with different card number. Matte black with no visible card numbers for privacy.

- Virtual card: Issued instantly upon KYC approval (same day in most cases)

- Physical card: Optional, £9.99 fee

- Design: Matte black finish with Plutus logo (no visible card numbers for privacy)

- Material: Recycled PVC (2026 sustainability initiative)

Payment Network

- Network: Visa debit

- Acceptance: 80M+ merchants worldwide

- Contactless: Yes (NFC limit: £100 standard, £300 if enabled in app)

- Mobile wallets: Apple Pay, Google Pay, Samsung Pay, Curve integration

Security Features

- 3D Secure 2: Required for online purchases over £30

- Instant freeze/unfreeze: Toggle card on/off in-app

- Transaction notifications: Real-time push alerts

- Virtual card rotation: Generate new virtual card numbers monthly for subscription security

How Spending Works: Transaction Flow

Example: £200 grocery shop at Tesco

Step 1: Pre-load fiat balance

- You transfer £200 GBP from your bank → Plutus card

- Arrives via UK Faster Payments (instant) or SEPA (1-2 business days for EEA)

Step 2: Shop at Tesco (designated perk merchant)

- You tap Plutus card to pay £200

- Visa network processes instantly

- £200 debited from your fiat balance

Step 3: Plutus calculates rewards

- Perk rebate: First £10 of Tesco purchase = £10 in PLU (100% rebate)

- Cashback: Remaining £190 x 6% (Legend tier) = £11.40 in PLU

- Total earned: £21.40 in PLU for this transaction

- Eligible spend note: This £200 counts toward your monthly eligible spend cap (£250/£500/£1,000 depending on plan). Once you hit the cap, subsequent purchases earn zero cashback for the rest of the month.

Step 4: Monthly PLU distribution (around 5th of next month)

- All month's rewards tallied

- PLU sent directly to your connected wallet on Polygon

- You retain full custody—can sell, stake, or hold for next month's tier

Gas costs: Zero. Plutus covers the Polygon gas fees to send you rewards.

Subscription Plans: Which Tier Makes Sense?

Starter Plan (£6.99/month)

What you get:

- 3% base cashback

- £250 eligible spend per month (only the first £250 of spending earns rewards)

- 1 perk slot (£10 value)

Monthly break-even:

- Subscription cost: £6.99

- Max cashback: £250 x 3% = £7.50

- Perk value: £10

- Net at full usage: £10.51/month (£126/year)

- Break-even requires spending at least £233/month AND using the perk slot

Best for: Testing Plutus before committing to a higher tier. The economics are tight - at £6.99/month for a £250 eligible spend cap, you need to maximize every element to make it work.

Everyday Plan (£9.99/month)

What you get:

- 3% base cashback

- £500 eligible spend per month

- 2 perk slots (£20 value)

Monthly break-even:

- Subscription: -£9.99

- Perks: +£20

- Max cashback: £500 x 3% = £15

- Net at full usage: £25.01/month (£300/year)

- Break-even requires spending at least £333/month AND using both perk slots

Best for: Regular domestic spenders in the £500-1,500/month range

ROI example (£1,500/month domestic spend):

- Subscription: -£9.99

- Perks: +£20 (Netflix, Spotify)

- Cashback: £500 (eligible) x 3% = +£15 (remaining £1,000 earns nothing)

- Net: £25.01/month = £300.12/year

Premium Plan (£19.99/month)

What you get:

- 3% base cashback (higher with stacking)

- £1,000 eligible spend per month

- 3 perk slots (£30 value)

Monthly break-even:

- Subscription: -£19.99

- Perks: +£30

- Max cashback at 3%: £1,000 x 3% = £30

- Net at 3% (no stacking): £40.01/month (£480/year)

- With Legend stacking (6%): £1,000 x 6% = £60 cashback → £70.01/month (£840/year)

Best for: Users who stack PLU for 6%+ rates and can fill all 3+ perk slots. Without stacking, the Premium plan only marginally beats Everyday.

ROI example (£3,000/month domestic spend, Legend tier 6%):

- Subscription: -£19.99

- Perks: +£60 (6 perks from Legend tier, overriding plan's 3)

- Cashback: £1,000 (eligible) x 6% = +£60 (remaining £2,000 earns nothing)

- Net: £100.01/month = £1,200.12/year

The Stacking Decision: Should You Buy PLU?

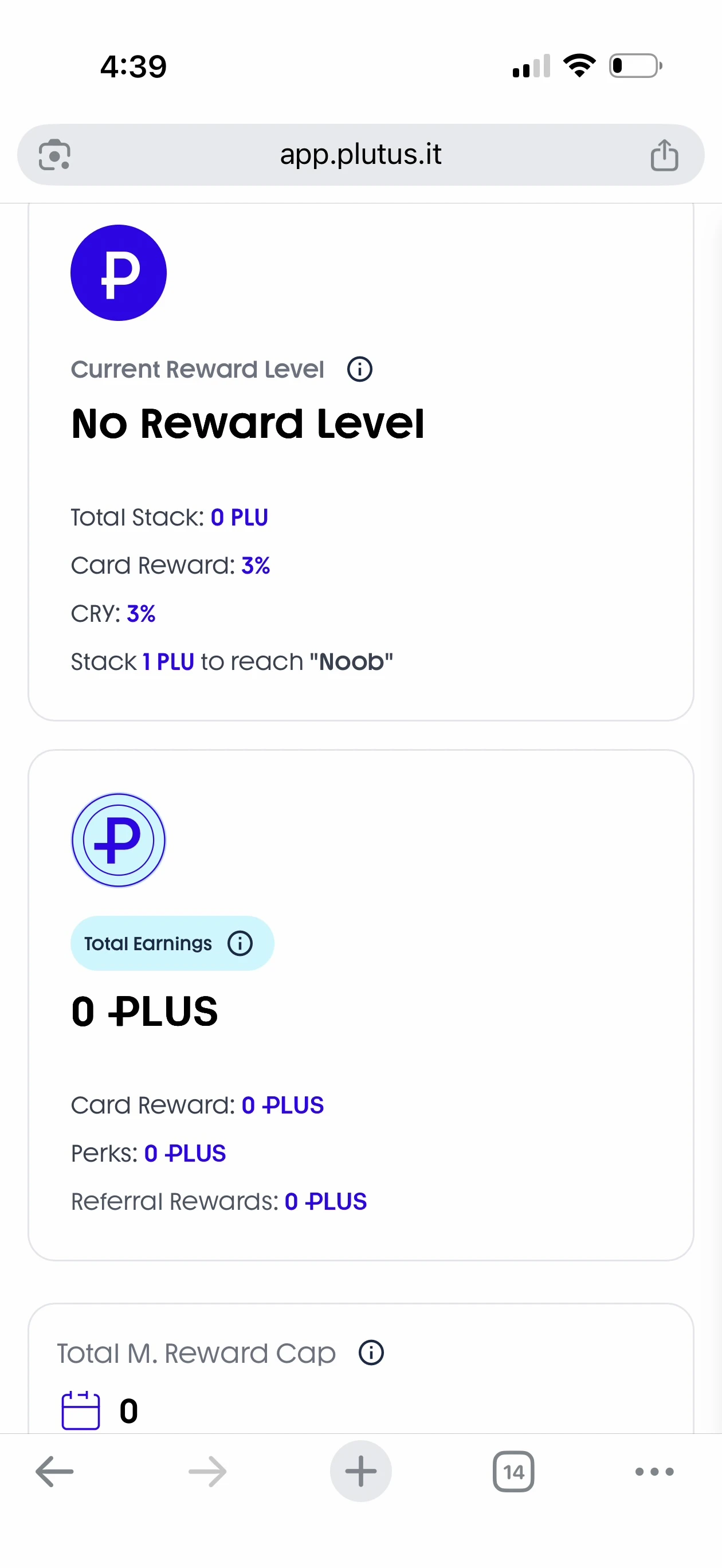

Rewards Dashboard - Track your reward level, cashback rate, CRY rate, earnings breakdown (card rewards, perks, referrals), and monthly reward cap progress.

Recall the tiers (PLU price approx. £0.10 as of March 2026):

- 1 PLU = 3% cashback, €1 cap (Noob)

- 500 PLU (approx. £50) = 3%, 1 perk (Adventurer)

- 2,000 PLU (approx. £200) = 4%, 4 perks (Hero)

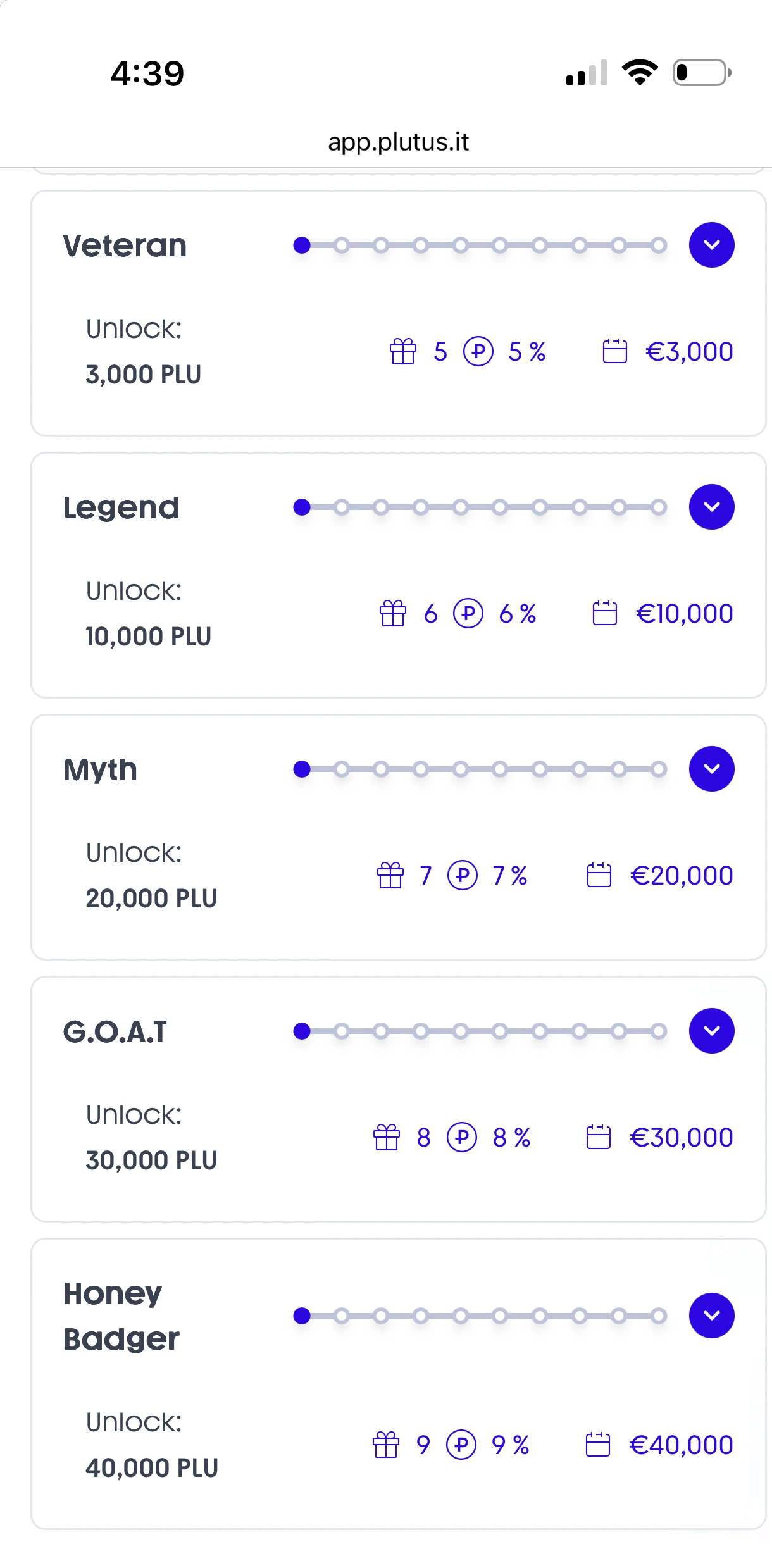

- 3,000 PLU (approx. £300) = 5%, 5 perks (Veteran)

- 10,000 PLU (approx. £1,000) = 6%, 6 perks (Legend)

- 30,000 PLU (approx. £3,000) = 8%, 8 perks (G.O.A.T)

- 40,000 PLU (approx. £4,000) = 9%, 9 perks (Honey Badger)

Higher Tiers - Veteran (3K PLU, 5%, EUR 3K) to Honey Badger (40K PLU, 9%, 9 perks, EUR 40K cap). At PLU approx. £0.10, Legend tier costs approx. £1,000.

Break-even analysis for Legend tier (10,000 PLU = approx. £1,000 staked at current prices):

You are paying approx. £1,000 upfront (opportunity cost) to upgrade from 3% to 6% cashback. But critically, this only applies to your eligible spend (max £1,000/month on Premium).

Monthly benefit:

- Extra 3% on eligible spend only: 3% x £1,000 = £30 extra cashback per month

- Plus 3 additional perks (Legend 6 vs Premium 3): £30 extra perk value per month

- Total monthly benefit: £60 extra

- Annual benefit: £720

Payback period: £1,000 / £60/month = approx. 17 months

Risk: If PLU drops 30% during that time:

- Your £1,000 stake becomes £700 (-£300 loss)

- Your extra rewards = £720/year (still £420 net profit after first year)

Conclusion: Legend tier makes sense if:

- You consistently spend £1,000+/month to maximize eligible spend

- You can fill all 6 perk slots each month

- You can hold approx. £1,000 in PLU for 17+ months to break even

- You are comfortable with 30-50% PLU volatility risk on the staked amount

Perk Selection Masterclass

You can change perks once per month (1st-5th of each month). Here's how to maximize value:

High-Frequency Perks (Use if you shop there regularly)

- Tesco: If you grocery shop weekly, you'll hit £10 four times → Use it

- Amazon: If you order Prime regularly, instant £10 rebate

- Uber: 2-3 rides = £10, easy to hit

Subscription Perks (Set and Forget)

- Netflix, Spotify, Disney+: If you already pay these, 100% no-brainer

- YouTube Premium, Amazon Prime: Same logic

Trap Perks (Avoid unless you already shop there)

- High-end retail (Harrods, Selfridges): Unless you're already spending there, don't force it

- Airlines (BA, Ryanair): Only useful if you travel monthly

The Rotation Strategy

Month 1 (January):

- Tesco, Aldi, Lidl, Sainsbury's, Waitrose

- Why: Post-holiday budget mode, focus groceries

Month 2 (February):

- Netflix, Spotify, Amazon, Disney+, YouTube

- Why: Fewer big purchases, lock in subscriptions

Month 3 (March):

- Uber, Trainline, Shell, Booking.com, Ryanair

- Why: Spring travel season

Pro tip: Track your spending in January, then assign perks based on actual behavior, not aspirational spending.

Foreign Exchange: 2.5% Non-Domestic Fee

2026 change: Plutus now charges 2.5% on all non-domestic (foreign currency) transactions. This is a significant shift from the previous 0% FX policy and fundamentally changes how the card should be used.

Example: UK cardholder spending in Paris

- You spend EUR 100

- Mid-market rate: EUR 1 = GBP 0.85 → Should cost £85

- Visa exchange rate (approx. 0.5% spread): £85.43

- Plutus 2.5% non-domestic fee: +£2.14

- You pay: £87.57

- Total effective FX cost: approx. 3%

Comparison:

- Traditional UK bank card (2.75% FX): £87.34

- Plutus (2.5% + Visa spread): £87.57

- Wise (0% spread): £85.00

- Wirex (0% FX): £85.43

- Crypto.com (0% FX): £85.43

Verdict: Plutus is now MORE expensive than many traditional bank cards for international spending. The 2.5% fee makes it unsuitable as a travel card. For any non-domestic spending, use a 0% FX alternative (Wirex, Crypto.com, Gnosis Pay, or Wise).

Best practice: Use Plutus exclusively for domestic GBP or EUR spending where you can maximize perks and cashback. Pair it with a 0% FX card for all international transactions.

Limits & Restrictions

Spending Limits (2026)

| Limit | All Plans |

|---|---|

| Single transaction | £500,000 |

| 30-day spending | £1,000,000 |

| Eligible spend (rewards) | Starter £250, Everyday £500, Premium £1,000 |

Transaction limits are generous across all plans. The real constraint is the eligible spend cap for rewards - only the first £250/£500/£1,000 of monthly spending earns cashback, regardless of how much you actually spend.

ATM Withdrawals

- Fee: 2.5% on all cash withdrawals

- Example: Withdraw £200 → £200 x 2.5% = £5.00 fee

Recommendation: Avoid ATM use entirely. The 2.5% fee wipes out any cashback earned. Use the card for tap-to-pay purchases only.

Restricted Merchants (No Rewards)

Plutus blocks rewards for:

- Gambling sites (Bet365, Paddy Power, etc.)

- Crypto exchanges (Coinbase, Binance, Kraken)

- Money transfer services (Wise, Western Union)

- Bill payments in some cases (utilities via third-party platforms)

Workaround: Pay these directly from bank account, reserve Plutus for reward-eligible spending.

What Happens If Plutus Goes Bankrupt?

Your fiat balance on the card:

- Held in segregated accounts at Modulr FS Limited (FCA-regulated e-money institution)

- Protected under UK Electronic Money Regulations

- In bankruptcy, you'd likely recover 100% within 30-90 days via FCA claims

Your PLU rewards:

- Already distributed to your self-custody wallet = zero risk

- Pending rewards (current month not yet paid) = at risk (max exposure: approx. £90 for Premium users at 9% on £1,000 eligible spend, plus perk rebates)

Comparison to custodial exchange cards:

- Crypto.com bankruptcy → Users lose 100% of balances on platform

- Plutus bankruptcy → Users lose only current month's pending rewards (approx. £90 + perk value)

The self-custody shield: Our annual cost calculation rates this as the single strongest risk-mitigation feature of Plutus. Even catastrophic failure leaves your historical PLU earnings untouched in your wallet.

Real User Scenarios

Scenario 1: Sarah (Freelancer, £2,500/month domestic spend)

Setup:

- Everyday plan (£9.99/month)

- No stacking (busy with work, cannot manage PLU)

- 2 perks: Netflix, Spotify

Results after 6 months:

- Perks earned: £120 (£20 x 6)

- Cashback earned: £90 (£500 eligible x 3% x 6 months - remaining £2,000/month earns nothing)

- Subscription cost: -£59.94

- Net profit: £150.06 in 6 months (£300/year)

Her verdict: "The eligible spend cap means most of my spending earns nothing. But the two subscription rebates cover the plan cost, and £15/month in cashback is free money on top. Just do not expect to get rich from it at the Everyday tier without stacking."

Scenario 2: Marcus (Crypto trader, £6,000/month domestic spend)

Setup:

- Premium plan (£19.99/month)

- G.O.A.T tier (30,000 PLU stacked, approx. £3,000 at current prices)

- 8% cashback + 8 perks

Results after 12 months:

- Perks earned: £960 (£80 x 12, 8 perks from G.O.A.T tier)

- Cashback earned: £960 (£1,000 eligible x 8% x 12 months - remaining £5,000/month earns nothing)

- Subscription cost: -£239.88

- Gross profit: £1,680.12

PLU risk: His 30,000 PLU staked dropped 25% during the year = -£750 loss on stake

Net profit: £930.12 (31% return on approx. £3,000 staked)

His verdict: "The eligible spend cap completely changed the math. I earn 8% but only on £1,000/month - the other £5,000 is dead weight. I could get similar results at Legend tier (6%, £1,000 eligible) with a third of the PLU investment. G.O.A.T only makes sense if you want all 8 perk slots."

Scenario 3: Emma (Student, £800/month spend)

Setup:

- Starter plan (£6.99/month)

- No stacking

- 1 perk: Spotify

Results after 12 months:

- Perks earned: £120 (Spotify £10 x 12)

- Cashback earned: £90 (£250 eligible x 3% = £7.50/month x 12)

- Subscription cost: -£83.88

- Net profit: £126.12

Her verdict: "With the Starter plan now costing £6.99/month, the math is tighter. Spotify rebate covers most of the subscription, and £7.50/month in cashback is a small bonus. But at £800/month spending, £550 of it earns nothing. It still works for me because I want the Spotify rebate anyway, but this is not the free ride it used to be."

How Plutus Compares to Other UK/EEA Cards

For UK users:

- Crypto.com: 0% FX, global availability, lounge access, but custodial. Better for travelers.

- Wirex: Up to 8% cashback, 0% FX, £14.99/month. Better for international spending.

- Curve: No crypto rewards, but 1% cashback + aggregates all your cards (not a crypto card)

For EEA users:

- Gnosis Pay: Self-custodial, 1-5% GNO cashback, 0% FX. Better all-around European card for mixed spending.

- Nexo: 0.2% FX (EEA weekday), 2% cashback, custodial model. Simpler with lower FX (0.2% vs 2.5%).

Plutus's unique value in 2026:

- Highest theoretical cashback ceiling (9%) in the market

- Only non-custodial card with elite-tier rewards

- 50+ lifestyle perks (no competitor matches this variety)

- But: 2.5% FX fee, no free tier, low eligible spend caps, and domestic-only economics mean Plutus now occupies a narrow niche - dedicated UK/EEA domestic perk optimizers who actively stack PLU

The Verdict: Is Plutus Visa Worth It in 2026?

Use Plutus Visa if:

- ✅ You live in UK or EEA and spend primarily in your domestic currency

- ✅ You stack PLU (at least Adventurer tier) to unlock meaningful cashback

- ✅ You already use self-custody wallets (MetaMask, Ledger)

- ✅ You actively optimize perk selections monthly

- ✅ You value non-custodial security over simplicity and low fees

Skip Plutus if:

- ❌ You spend internationally - the 2.5% FX fee eliminates any travel value

- ❌ You are new to crypto and self-custody feels overwhelming

- ❌ You spend under £500/month (eligible spend caps leave too little room for meaningful returns)

- ❌ You want a simple, low-maintenance card

- ❌ You live outside UK/EEA

- ❌ You are unwilling to pay £6.99-£19.99/month subscription

Final verdict: The 2026 pricing overhaul significantly narrowed the Plutus Visa Card's value proposition. The removal of the free tier, introduction of 2.5% FX fees, and reduction in plan perk counts mean Plutus is no longer a general-purpose European crypto card. It is a niche tool for dedicated domestic perk optimizers.

For crypto-native UK/EEA users who stack PLU, actively manage perks monthly, and spend primarily in their home currency, Plutus still offers the highest theoretical cashback rate in the market (9%). The non-custodial model remains its strongest differentiator - your PLU is always in your own wallet. But the eligible spend caps (max £1,000/month on Premium) mean even high spenders earn rewards on only a fraction of their total volume. Pair Plutus with a 0% FX card for international spending to build a genuinely optimized setup.

Sources & Verification

All card specs, fees, and limits verified from:

FAQ

How do you choose Plutus Visa Card crypto cards?

We compare verified issuer sources, fees, and eligibility. Availability can change, so confirm with the issuer before applying.

Do all cards in this list offer the same benefits?

No. Each issuer defines its own program terms. Review the sources on each card profile.

Are these rankings or recommendations?

No. Lists are filtered views of cards in our database and do not imply rankings.

This is a debit card. Some merchants with pre-authorization holds (hotels, car rentals) may temporarily hold funds beyond the transaction amount.

This card requires token staking to unlock higher reward tiers. If the staked token's price drops, your losses may exceed the cashback earned. Consider the break-even math before locking funds.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?