Plasma One Lite Card Review 2026

Plasma One Lite Card is a free self-custodial Visa on the Plasma chain. 2% cashback on the first $500/month (then 0.1%) in XPL, 0% APR, up to 5% variable yield on stablecoin balance, Apple Pay support.

Prefer mobile? Scan to continue

Opens the mobile signup with your SpendNode link, code SPESPE.

SpendNode Rating for Plasma One Lite Card

Plasma One pairs a Visa card with a self-custodial smart wallet and a stablecoin yield vault on a chain built for stablecoin payments. In our testing, the XPL cashback (2% on the first $500/month, then 0.1%) paid out weekly on Thursdays and the Earn vault ran 3.93% APY with no lockup. Lite is the free entry tier of a three-tier lineup.

The architecture is unusual for a card product: self-custodial wallet, third-party issuer (Rain), third-party fiat rails (Bridge), third-party yield (Veda vault). That keeps the trust story clean but means the consumer is taking smart-contract risk on the Earn side and XPL price risk on cashback. The app now itemizes every fee in two places, as a preview before you confirm a purchase and again on the post-purchase receipt, so the real cost is visible at the point of spend. Lite is free with no token lock; the Core and Platinum tiers step up the rate and perks.

Also relevant for Self-Custody Spending.

How It Competes

Cost Efficiency

4.5

Product Utility

4.2

Custody & Trust

4.4

Reliability & UX

4.2

Transparency

4.3

APPLE PAY

Verified

CASHBACK

Verified

YIELD LINKED

Verified

Plasma One Lite Card Overview

Free Self-Custodial Visa - 2% XPL Cashback, 0% APR, Up to 5% Variable Yield on Idle Balance

The Plasma One Lite Card is the free entry tier of Plasma One Cards. Free annual fee, 2% base cashback in XPL, 0% APR, and up to 5% variable yield on the stablecoin balance through the Earn vault. Best for stablecoin spenders who want a free self-custodial card and are comfortable with XPL exposure on their rewards.

Fees & Charges

Annual Fee

Free

FX Fee

1%

ATM Fee

TBD

Requirements

Supported Regions

GLOBAL

Spendable Assets

USDT, USDC

On This Page

The Plasma One Lite Card is the free entry tier of the Plasma One Visa lineup, which also includes the Core and Platinum tiers.

The card is a self-custodial Visa funded by a stablecoin wallet on the Plasma chain, charges no annual fee, 0% APR, and a 1% FX fee on non-USD purchases, earns 2% cashback on the first $500 of monthly spend (then 0.1% above), paid weekly in XPL, and pairs with an Earn vault that pays up to 5% variable yield on idle stablecoin balance.

It supports Apple Pay and is issued by Rain, a Visa Principal Member, under a license from Visa, with account services powered by Bridge.

A Free Self-Custodial Visa on a Stablecoin-Native Chain

The Plasma One Lite Card is the free entry tier of Plasma One, the consumer product of Plasma, a layer-1 blockchain whose entire purpose is moving stablecoins.

The card sits on top of that chain: your USDT or USDC balance lives in a self-custodial smart wallet on Plasma, you tap a Visa card or Apple Pay, the balance funds the purchase, and cashback in XPL credits to your rewards ledger (paid weekly, on Thursdays). The Earn vault sits inside the same app and pays variable yield on whatever stablecoin balance you have not yet spent.

This is the same architectural family as Tuyo and Avici Platinum. All three keep custody on your side, and all three use a regulated card issuer for the Visa rails. Plasma One is the only one of the three that pays live cashback in a chain-native token (XPL), with the chain itself as a substantive value-accrual story rather than a points placeholder.

Lite is where most people start: free, no token lock, 2% cashback on the first $500/month. The Core and Platinum tiers step the rate and perks up for a fee or an XPL lock, and each has its own review.

In our hands-on testing, the card worked as advertised on the core flow. Funding from USDT on the Plasma chain settled in minutes. Cashback pays weekly in XPL, on Thursdays. The Earn vault displayed 3.93% against the "up to 5%" headline, with no lockup and on-demand withdrawals.

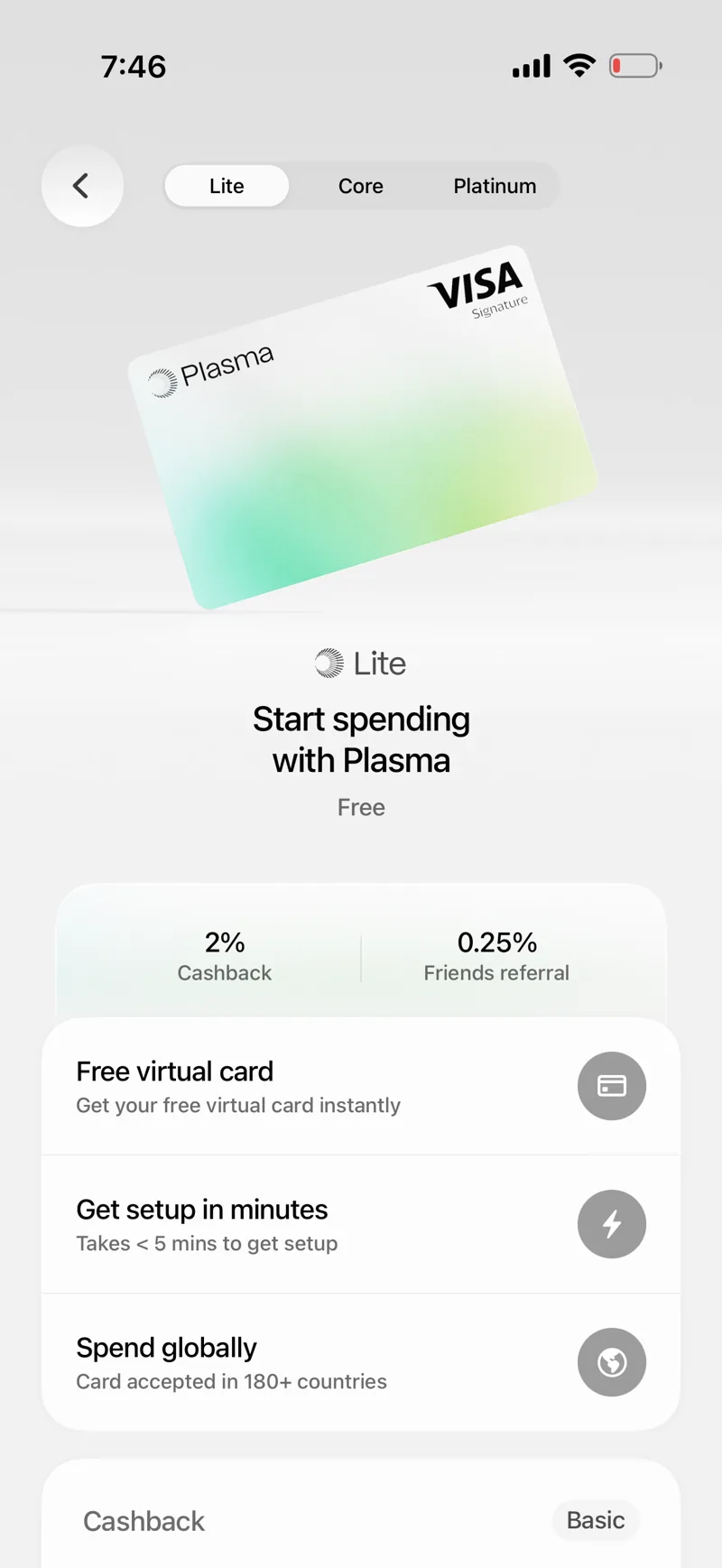

SpendNode app screenshot

Lite tier overview - Free white Visa, 2% base cashback on the first $500/month and 0.25% referral, a free virtual card issued instantly, and global acceptance in 180+ countries.

Card Specs: What You Are Actually Getting

Physical and Virtual Cards

The Plasma One Lite Card is virtual at time of review. It provisions directly into Apple Wallet at activation. Lite includes one free virtual card and no physical card; the Core tier adds a physical card and Platinum ships a 16g metal Visa Infinite.

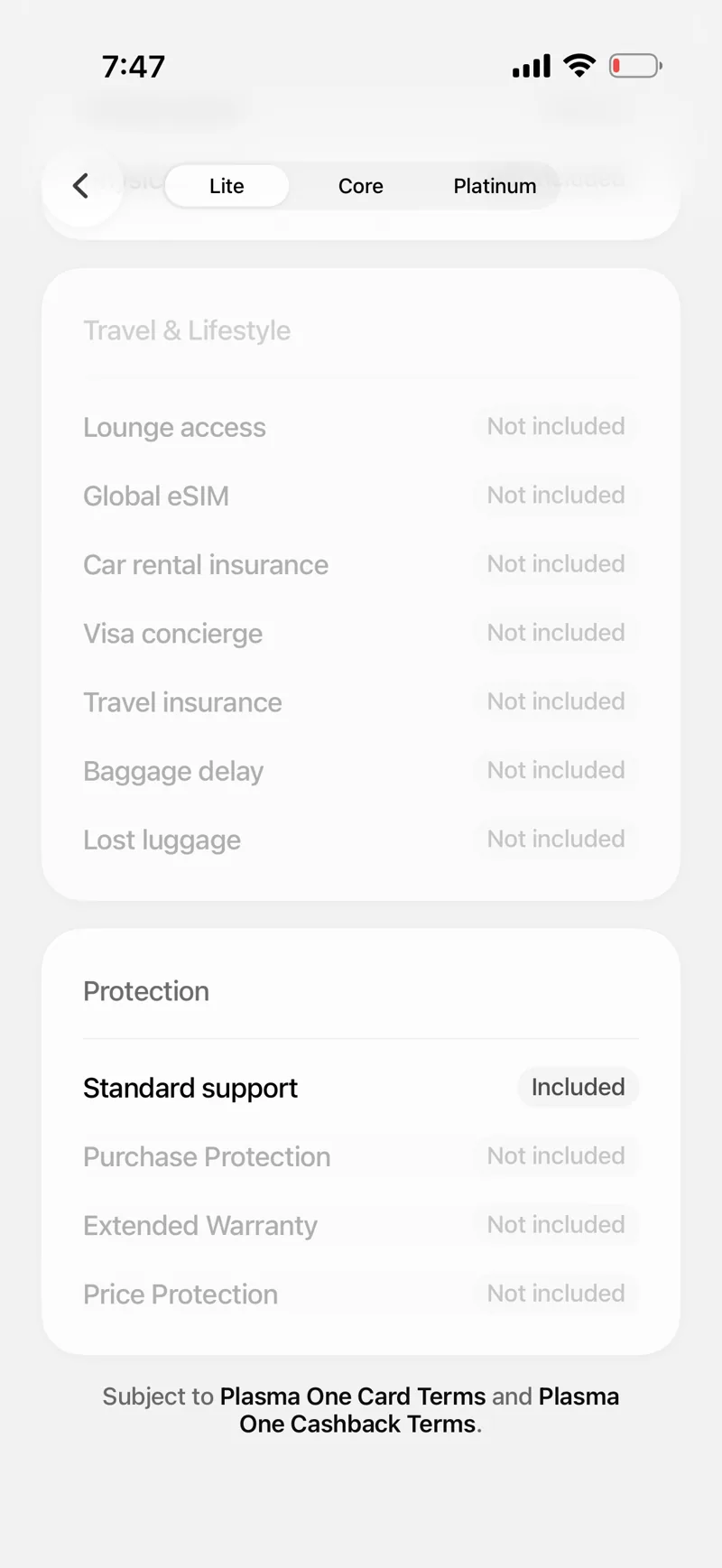

SpendNode app screenshot

Lite is the lean tier - Travel and lifestyle perks (lounges, eSIM, insurance) and purchase protections are not included on Lite; you get standard support. Those benefits begin on Core and fill out on Platinum.

Because the card is virtual, ATM withdrawals are not available on Lite. Spending is tap-to-pay via Apple Wallet on iPhone and Apple Watch, or online card-not-present checkout where the Visa credentials are entered manually or auto-filled. The Plasma One app runs on iOS and Android.

Activation happens in-app through a Terms and Conditions acceptance screen that bundles the E-Sign Consent, the Plasma One Card Terms, the Plasma One Cashback Terms, and the Issuer Privacy Policy. Once you accept and tap "Activate Card," the virtual card is live and ready to add to Apple Wallet.

Payment Network

Visa international. The Plasma One Card is accepted anywhere Visa is accepted, across roughly 150+ countries and tens of millions of merchants. Online and in store. Contactless, chip, and Apple Pay. The app runs on iOS and Android; tap-to-pay runs through Apple Wallet on iPhone and Apple Watch.

Security Features

- Hardware-backed keys (passkeys / biometric) instead of seed phrases for account access

- In-app freeze and unfreeze with a tap

- Configurable daily spending limit ($1,000 / $5,000 / $10,000 / Custom presets)

- Real-time push notifications on every transaction

- Self-custodial wallet model: Plasma cannot move funds without an action you sign

The self-custody architecture is the single most important security feature. Even if Plasma's servers are compromised, an attacker cannot move your stablecoin balance without your authentication. The trade-off is that there is no central party to recover funds if you lose access to your authentication method. Account deletion or device loss can result in complete loss of the underlying wallet.

Getting the Card

The full step-by-step sign-up flow (access code, KYC, activation, funding, and daily limits) lives on the Plasma One vendor page.

How Spending Works

Example: $1,200 purchase at a hotel in EUR.

Step 1. Fund the wallet. You deposit 1,500 USDT on the Plasma chain (free) or 1,500 USDC on Polygon (free, under the $30k cap). The balance shows in your Plasma One wallet.

Step 2. Tap to pay. At the hotel terminal you tap your Plasma One Card or your phone via Apple Pay. The terminal authorizes a 1,200 EUR transaction with Visa.

Step 3. Authorization and conversion. Plasma does not show an FX fee as a separate line; the 1% FX fee on non-USD spend is collected in the conversion rate rather than shown as a labeled entry. On a 1,200 EUR purchase at a ~1.08 mid-market rate (=$1,296), the 1% adds about $13, landing you around $1,309. Cross-border fee is 0%, so no extra surcharge for the international merchant.

Step 4. Settlement from your balance. The purchase is settled from the stablecoin balance in your self-custodial wallet on the Plasma chain. From the user's view this looks identical to a debit: tap, settle, done.

Step 5. Cashback calculation. Card spend earns 2% on the first $500 of monthly spend, then 0.1% above. If this $1,322 purchase falls early in the month, the first $500 earns 2% ($10) and the rest earns 0.1% (about $0.82), roughly $11 in XPL at the spot price when cashback credits.

Step 6. Cashback distribution. Cashback is paid weekly, on Thursdays, in XPL to your Rewards ledger, and may stay pending for several days before it vests. The dollar value of your XPL when it lands depends on the token's market price, which can move between when you spent and when you received cashback.

Step 7. Optional Earn allocation. Any remaining stablecoin balance can be moved to the Earn vault for yield. Allocation and withdrawal are on-demand.

Fees and Rates

| Fee | Amount | Notes |

|---|---|---|

| Annual fee | $0 | Lite tier |

| APR on purchases | 0% | Plasma reserves the right to introduce interest later |

| Card issuance (virtual) | $0 | Free at signup |

| Foreign exchange fee | 1% | On non-USD purchases |

| Cross-border fee | 0% | No surcharge for international merchants |

| USDT funding (Plasma chain) | Free | Native chain route |

| USDT funding (Polygon, Ethereum, Arbitrum) | Free | Plus third-party network fees |

| USDC funding (Polygon, Ethereum, Arbitrum) | Free up to $30,000 | Above $30k: third-party fees may apply |

| USD ACH deposit | Free | Through Bridge; settlement times standard |

| USD wire deposit | Free | Through Bridge |

| Cashback | 2% base, paid in XPL | 2% on the first $500/mo, then 0.1%; no hard dollar cap |

| Cash advances and balance transfers | Not available | Excluded in the Card Terms |

Break-even math: With $0 annual fee, 0% APR, and free funding on the Lite tier, any positive cashback or yield is net positive against zero fixed cost. Break-even is effectively immediate. The relevant question is opportunity cost vs alternatives, which the Real User Scenarios section below covers in detail. If you spend heavily on AI tools or travel, the paid Core and Platinum tiers can out-earn Lite despite their cost, which the comparison section addresses.

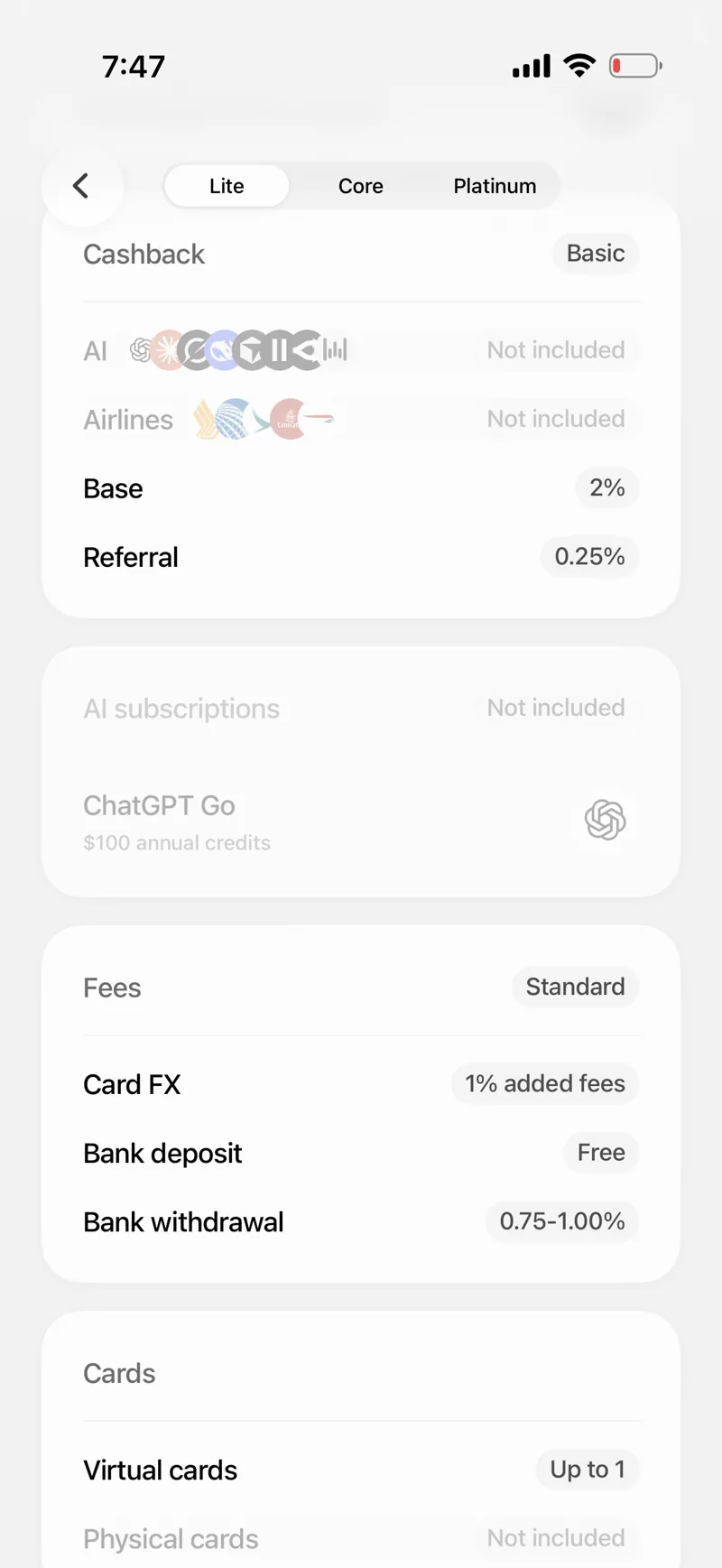

SpendNode app screenshot

Lite cashback and fees - 2% base and 0.25% referral, with no AI or airline boost on the free tier. Card FX is 1% on non-USD spend, bank deposits are free, and bank withdrawals run 0.75-1.00%.

Rewards and Cashback

Plasma One pays cashback in XPL, the native token of the Plasma chain. The economic effect is different from cashback paid in USDC or fiat, and the difference is worth understanding before you start earning.

The bull case. If XPL appreciates against the dollar between the time you earn it and the time you spend or sell it, your effective cashback rate exceeds 2%. Token-denominated rewards on chains that grow value over time can outpace the headline cashback rate. Plasma is positioned as infrastructure for the stablecoin payments market, which is one of the more credible verticals in 2026 crypto.

The bear case. If XPL depreciates 25-50% from the date you earn it, your realized cashback drops proportionally. At a 50% decline, your 2% cashback becomes effectively 1%. Below that, a custodial card paying stable USD cashback would have served you better.

The neutral case. XPL holds roughly flat against the dollar. Your effective rate is approximately 2% with a few weeks of holding-period drift. This is the most likely short-term outcome assuming the chain's token model functions as planned.

Risk mitigation. You can swap XPL to USDT on the Plasma chain (or any DEX with XPL liquidity) on receipt to lock in the dollar value at credit. The trade-off is gas costs on the swap and your view of XPL trajectory. Users who believe in the Plasma chain typically hold XPL; users who want pure cashback efficiency convert on receipt.

What if XPL is illiquid? This is the worst case. If liquidity dries up at the moment you want to exit, you may face significant slippage. Stay aware of XPL's DEX depth on Plasma and external listings.

Multi-Chain Funding

Most self-custodial Visa cards lock you to one chain for funding:

- Tuyo is USDC on Base only

- Gnosis Pay is EURe on Gnosis Chain only

- Ready's unavailable program was on Starknet only

- Avici Platinum is USDC on supported chains

Plasma One supports USDT on Plasma, Polygon, Ethereum, and Arbitrum, plus USDC on Polygon, Ethereum, and Arbitrum, plus USD ACH and wire. Seven funding routes against most competitors' one. If you already hold USDT on Polygon from a previous CEX withdrawal or DEX swap, you can fund without paying bridge fees or waiting for cross-chain swaps. For users who move funds across chains routinely, this saves real money each year.

Limits and Restrictions

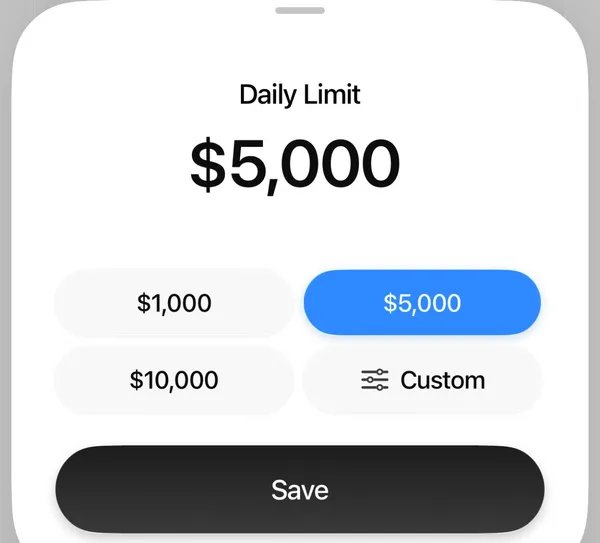

Daily Spending Limit

The Plasma One Card has a user-configurable daily spending limit set in-app:

| Preset | Daily Limit |

|---|---|

| Low | $1,000 |

| Default | $5,000 |

| High | $10,000 |

| Custom | User-defined (may require higher KYC tier) |

SpendNode app screenshot

Daily Limit selector - User-configurable in-app. The effective limit is the lower of the user-set daily preset and your stablecoin balance.

The custom option allows users to set a daily limit other than the three presets, subject to KYC review. We have not tested the upper bound of the custom option. The effective spending limit is also bounded by the market value of your stablecoin balance.

Restricted Merchant Categories

The Plasma One Cashback Terms exclude a list of transactions from earning rewards: ATM withdrawals, peer-to-peer transfers, currency exchange, tax payments, gift cards and prepaid cards, money orders and cash equivalents, gambling and quasi-cash, cryptocurrency purchases, wire and balance transfers, and any spending Plasma judges to be structured to game the program. Cash advances and balance transfers are also not available.

Eligibility Caveat

Plasma One is available across 150+ countries but does not publish a full country eligibility list for opening an account. United States residents are supported, with US account services provided by Bridge Building Inc. Eligibility is confirmed at signup through KYC, and the service is unavailable to OFAC-sanctioned individuals and entities. Because terms can vary by region, read the activation screens at signup to confirm the current terms for your jurisdiction.

There is also an access step. Download the app and enter the access code SPESPE at signup to skip the waitlist and reach the KYC step.

Is the Plasma One Lite Card Safe?

Self-custody is the answer to most of the failure question. Because your stablecoin balance is in a self-custodial wallet on the Plasma chain, you retain ownership of the funds regardless of what happens to Plasma the company. The four sub-questions break out as follows:

Stablecoin balance in your wallet. Unaffected. You retain control of the wallet via your authentication method. You would need an alternative interface to interact with the Plasma chain, since the chain itself is decentralized and survives the app. This is the key advantage over custodial alternatives like Crypto.com and Coinbase where balances are claims against the issuer.

Stablecoin balance in the Earn vault. Exposed to the vault's smart-contract risk. The Earn vault routes to third-party DeFi protocols, and if a protocol is exploited, the loss flows to you. Plasma does not guarantee the vault. Do not allocate more to Earn than you would accept as a smart-contract risk position.

Pending XPL cashback. At risk. If Plasma terminates the cashback program during a wind-down, XPL owed to you that has not yet vested may not pay out. This is consistent with how token-denominated rewards programs work in distress.

Card functionality. Stops. The card is issued by Rain under a license from Visa. If Plasma's relationship with the issuer ends, the card stops working. Your wallet survives. You can stand up another self-custodial Visa with a different issuer and fund it from your existing Plasma chain balance.

The net exposure for a typical user: only the Earn-allocated balance and any unpaid XPL cashback are at real risk. Spendable balance and any XPL already vested in your Rewards ledger are unaffected.

Is the Plasma One Lite Card a Scam?

No. The Plasma One Lite Card is issued by Rain, a Visa Principal Member, under a license from Visa. Account and currency services run through Bridge (Bridge Building Inc. for US residents, Bridge Building Sp. z o.o. for the EEA, and Bridge Building Limited elsewhere), and cashback in XPL paid out weekly, on Thursdays, per Plasma's terms. The Earn vault honored on-demand withdrawals at the displayed yield.

What the card is not: a deposit account. Stablecoin balances are not FDIC insured and are not bank deposits. The cashback is paid in XPL, which is volatile and can rise or fall against the dollar between when you earn it and when you spend or sell it.

Real risks exist and they are different from scam risks: XPL price volatility on rewards, smart-contract risk on the Earn vault, and the operational track record of a young product. None of those are scam markers. They are product and counterparty risks that a prospective user should weigh on their own merits.

Real User Scenarios

Scenario 1: Maya, occasional spender, $800/month

Setup: Funds Plasma One Lite Card with $1,500 USDC on Polygon, free. Spends $800/month on subscriptions and dining. Keeps $700 idle balance allocated to the Earn vault at 3.93%.

Results after 6 months:

- Card spend: $4,800

- Cashback: 2% on the first $500/month, then 0.1% above, so about $10.30/month, ~$62 in XPL at credit price

- Earn yield on average $700 balance: ~$13

- Total economic return: ~$75 over 6 months, or ~$12/month

- Annualized: ~$150 against $0 fees

Verdict: "Lite pays 2% on the first $500 of monthly spend and 0.1% past that, so at low volume the value is mostly that it is free, with a small cashback and yield kicker on top."

Scenario 2: Daniel, monthly $3,500 cross-border spender

Setup: Funds with USDT on the Plasma chain (free). Spends $3,500/month across mostly USD subscriptions and some EUR travel. Lite pays 2% only on the first $500/month; the rest earns 0.1%.

Results after 12 months:

- Card spend: $42,000

- Cashback: 2% on the first $500/month plus 0.1% on the ~$3,000 above, so about $13/month, ~$156/year in XPL

- FX cost on ~$8,000 EUR spend annually at 1%: -$80

- Earn yield on average $2,000 idle balance: ~$78

- Total economic return: ~$154/year against $0 fees

Verdict: "At $3,500/month, only the first $500 earns 2%; the rest earns 0.1%, so the cashback stays thin on a big spend. A spender at this level should treat Lite as a $500/month card or move to Core, where the 3% band runs to $1,000 and AI spend earns more."

Scenario 3: Anika, heavy spender, $9,000/month

Setup: Funds with $15,000 USDC and rotates from USDT funding when on the Plasma chain. Spends $9,000/month across business and personal.

Results after 6 months:

- Card spend: $54,000

- Cashback: 2% on the first $500/month, then 0.1% on the ~$8,500 above, so about $18.50/month

- Cashback over 6 months: ~$111 in XPL

- Earn yield on average $5,000 idle balance: ~$98

- Total return: ~$209 against $0 fees

Verdict: "At $9,000/month almost all of it earns just 0.1%, so Lite leaves real cashback on the table. This is the spender who should move up: Core and Platinum widen the high-rate bands and add AI and flight cashback that clear their cost at this volume."

Plasma One Lite Card vs Other Cards

For self-custodial USDC/USDT spenders, Plasma One is the self-custodial Visa paying live cashback in a chain-native token, starting at 2% on the free Lite tier. Tuyo is the closest match on architecture but pays no live cashback (TUYO points toward a 2026 TGE). Avici Platinum is secured credit with no cashback. Plasma One's value depends on XPL holding or appreciating.

For users wanting stable USD-equivalent cashback, Jupiter Global is the alternative: 4% headline in USDC with no token volatility, though its base cashback caps at $100/month, while Lite pays its 2% only on the first $500/month and 0.1% above. Choose Jupiter if you want certainty; choose Plasma One Lite if you want chain-token exposure and free yield on idle balance.

For users wanting more from Plasma One itself, the in-house step-up is the point of the tiers. Core adds 3% base, 5% on AI spend, and a ChatGPT Go rebate (up to $8/month) for $199/year or a 20,000 XPL lock.

Platinum reaches 4% base, 10% on AI spend, 10% on flights, travel perks, and a boosted 5% yield, in exchange for locking 100,000 XPL for 12 months. Lite is the free baseline; the paid tiers earn their keep only at higher or more AI-weighted spend.

Plasma One Lite Card unique value: A free self-custodial Visa where your idle balance earns yield, your spending earns chain-native cashback, and funding is free across four chains. It is the no-cost entry point to the Plasma chain stablecoin stack, with the rails, the spending instrument, and the savings vault all under one roof.

Who Should Use the Plasma One Lite Card?

Lite makes sense if you hold USDT or USDC across multiple chains and want a free card you can fund from any of them, you want 2% cashback on your first ~$500 of monthly spend accumulated as a chain-native token (XPL), and you want yield on idle stablecoin balance without lockup or manual DeFi management. It suits light spenders, roughly $500/month or less, who are comfortable with self-custodial wallet mechanics; heavier spenders earn far more on Core or Platinum, whose high-rate bands run much higher.

Look elsewhere if you need stable USD-equivalent cashback, where Jupiter Global pays in USDC with no token-price risk; if you spend more than about $500/month, since Lite drops to 0.1% above that band, or spend heavily on AI tools or travel, where Core and Platinum earn more even after their cost; if you need a physical card or ATM access, since Plasma One is currently virtual; if you need a regulated EMI, FDIC insurance, or UK FCA cardholder regime; or if you are a New York State resident, since Earn vault services are not available there.

The Plasma One Lite Card is one of the more credible free self-custodial Visa options in 2026, alongside Tuyo. Cashback pays weekly on Thursdays, the Earn vault ran at 3.93% in our testing with no lockup, and the multi-chain funding routes worked without hidden costs.

The friction points: the card is virtual (no ATM access yet), a 1% FX fee on non-USD spending, and rewards paid in a volatile token. For a free card, the trade is reasonable, and the paid tiers exist for anyone who outgrows it.

Sources and Verification

All card specs, fees, limits, and product mechanics verified from:

- Plasma One Lite tier page

- Plasma One Official

- Plasma Homepage

- Plasma One Cashback and Referral Terms

In-app screenshots and product flow captured during early-access testing. Earn yield (3.93% at observation) and daily limit presets ($1,000 / $5,000 / $10,000 / Custom) were directly observed in the app. Cashback is paid weekly (Thursdays) in XPL. Lite base cashback is 2% on the first $500/month, then 0.1% above, per Plasma's published rates, June 2026.

User scenarios above are composite illustrations based on the card's published mechanics and our testing. Actual returns depend on XPL price, Earn vault yield at the time of allocation, FX schedules confirmed at signup, and individual spending profiles.

Written by Aleksandar Dukic

FAQ

Does the Plasma One Lite Card have an invite code?

Yes. Enter the code SPESPE in the Plasma One app (iOS or Android) at signup. Download the app through SpendNode's Plasma One link and apply the code when you create your account. The code skips the waitlist.

Is the SPESPE code for the Plasma One Lite Card working in August 2026?

Yes. SPESPE is still a working Plasma One code as of August 11, 2026 - we re-verify it daily. It skips the waitlist.

What does the Lite tier cost?

Nothing. Lite is the free tier, with no annual fee and no token lock. APR is 0% on purchases and the foreign exchange fee is 1% on non-USD spend. The card is virtual at launch, so there is no ATM option yet.

What is the Lite cashback rate and how is it paid?

Card spend earns 2% on the first $500 of monthly spend, then 0.1% above, paid in XPL (the native token of the Plasma chain). Cashback is paid weekly, on Thursdays. The dollar value you receive depends on the XPL price when it is credited. Core and Platinum earn higher rates.

How does the up to 5% yield work?

Stablecoin balances can be allocated to the Earn vault. The displayed yield in-app at the time of review was 3.93%, with the marketing 'up to 5%' as the ceiling and a boosted, fixed 5% reserved for the Platinum tier. The vault has no lockup and can be withdrawn at any time. Yield comes from on-chain DeFi strategies and is variable, not a deposit interest rate.

Who issues the Plasma One Lite Card and is my balance protected?

The card is issued by Rain, a Visa Principal Member, under a license from Visa. Account services are powered by Bridge (Bridge Building Inc. for US residents, Bridge Building Sp. z o.o. for the EEA, and Bridge Building Limited elsewhere).

Your stablecoin balance is owned and custodied by you, not by Plasma. Stablecoin balances are not bank deposits and are not FDIC insured.

Is the Plasma One Lite Card available in my country?

Plasma One states the card works anywhere Visa is accepted, across 150+ countries, but does not publish a full country eligibility list for opening an account. Eligibility is confirmed at signup through KYC, and United States residents are supported. The service is unavailable to OFAC-sanctioned individuals and entities.

You retain custody of your funds until the moment of spending. Your balance is not exposed to provider insolvency risk.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?

User Reviews

Reviews are moderated and may take a moment to appear.