Plasma One Platinum Card Review 2026

Plasma One Platinum Card is the top self-custodial Visa tier on the Plasma chain. 4% base, 10% AI, 10% flight cashback in XPL, travel perks, boosted 5% yield. Requires locking 100,000 XPL.

Prefer mobile? Scan to continue

Opens the mobile signup with your SpendNode link.

SpendNode Rating for Plasma One Platinum Card

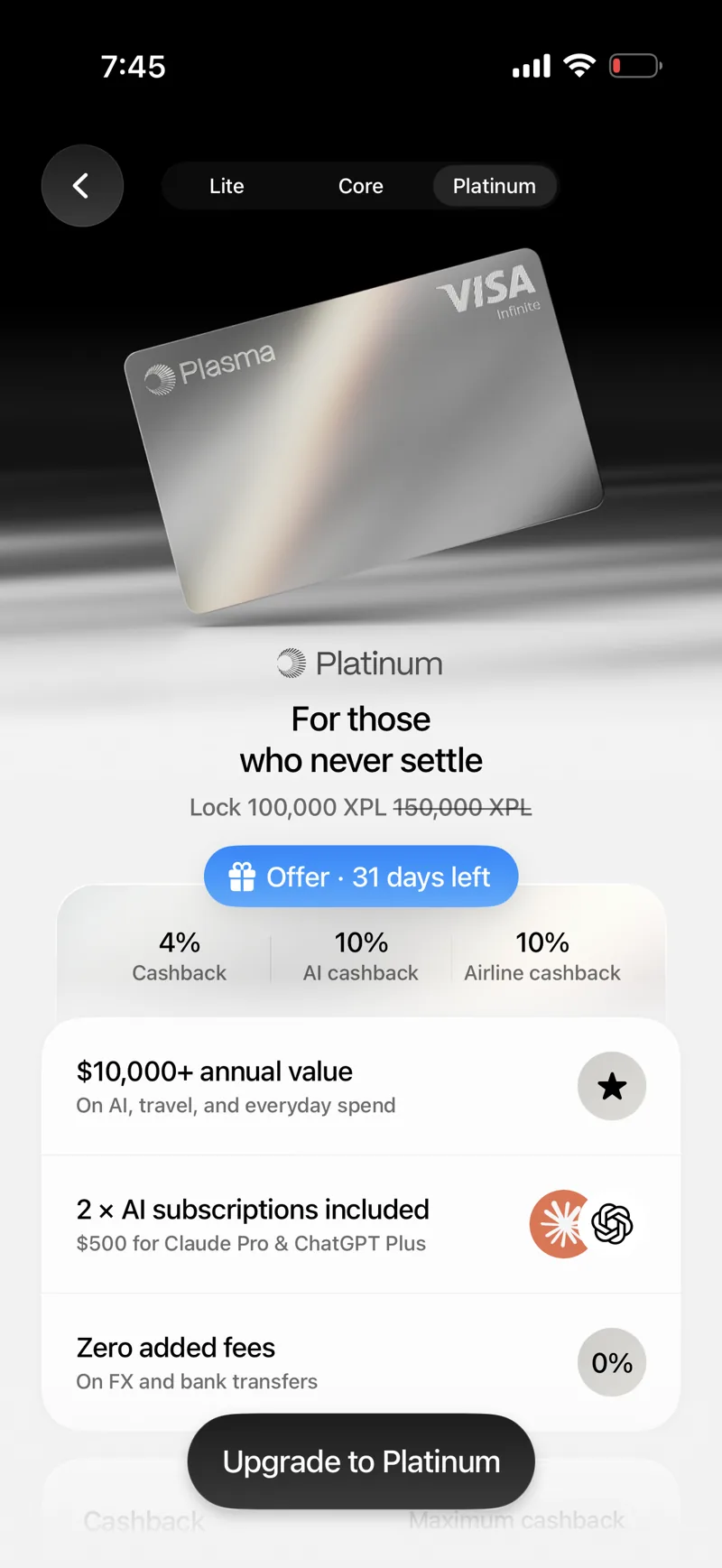

The top tier of Plasma One: a self-custodial Visa Infinite earning 4% base, 10% on AI spend, and 10% on eligible flights in XPL, with discounted Visa Airport Companion lounge access, travel perks, Claude Pro and ChatGPT Plus rebates (up to $20/month each), and a boosted, fixed 5% yield on the first $500,000 of balance. Access is a 100,000 XPL twelve-month lock rather than a cash fee.

Platinum is the richest tier on paper and the narrowest in fit. Its cost is not a fee but a year-long XPL lock and the price exposure that comes with it, so it makes sense mainly for users who already hold XPL or who carry a large stablecoin balance the boosted 5% yield can work on. For a moderate spender who would have to buy the lock, the base-rate bump over Core does not justify it. Cashback pays in XPL at the lineup's top rates, with no fixed monthly cap.

Also relevant for Travel / Lounge Access.

How It Competes

Cost Efficiency

3.8

Product Utility

4.5

Custody & Trust

4.4

Reliability & UX

4.2

Transparency

4.1

CASHBACK

Verified

YIELD LINKED

Verified

SELF CUSTODY SPEND

Verified

Plasma One Platinum Card Overview

Premium Self-Custodial Visa - 4% Base, 10% AI, 10% Flights, Lounge Access, Boosted 5% Yield

The Plasma One Platinum Card is the top tier. Access requires locking 100,000 XPL for 12 months, and no fiat subscription price has been published yet. It earns 4% base, 10% AI-spend, and 10% flight cashback in XPL, rebates up to $20/month each toward Claude Pro and ChatGPT Plus, pays a boosted 5% yield on the first $500,000 of balance, and adds full travel perks. Best for XPL holders and high or travel-heavy spenders comfortable with a year-long token lock.

Fees & Charges

Annual Fee

Free100k XPL lock (12 mo)

FX Fee

1%

ATM Fee

TBD

Requirements

Supported Regions

GLOBAL

Spendable Assets

USDT, USDC

On This Page

The Plasma One Platinum Card is the top tier of the Plasma One Visa lineup, which also includes the Lite and Core tiers. The card is a self-custodial Visa Infinite funded by a stablecoin wallet on the Plasma chain. Access requires locking 100,000 XPL for 12 months; Plasma has not published a fiat subscription price.

It charges 0% APR and up to 1% network FX with no Plasma markup on non-USD purchases, earns 4% base cashback in XPL, with 10% on AI spend and 10% on eligible flights, rebates up to $20/month each toward Claude Pro and ChatGPT Plus (about $480/year), ships a 16g metal Visa Infinite card, adds travel perks including discounted Visa Airport Companion lounge access, and pays a boosted 5% yield on the first $500,000 of stablecoin balance.

It is issued by Rain, a Visa Principal Member, under a license from Visa, with account services powered by Bridge.

The Top Tier of a Self-Custodial Visa Lineup

The Plasma One Platinum Card is the flagship of Plasma One, the consumer product of Plasma, a layer-1 blockchain built for stablecoin payments.

It keeps the self-custodial architecture of the Lite and Core tiers. Your USDT or USDC lives in a smart wallet on the Plasma chain, you tap a Visa or Apple Pay, and cashback credits in XPL. It layers on the highest rates, a full travel-perk stack, and a boosted yield reserved for the tier.

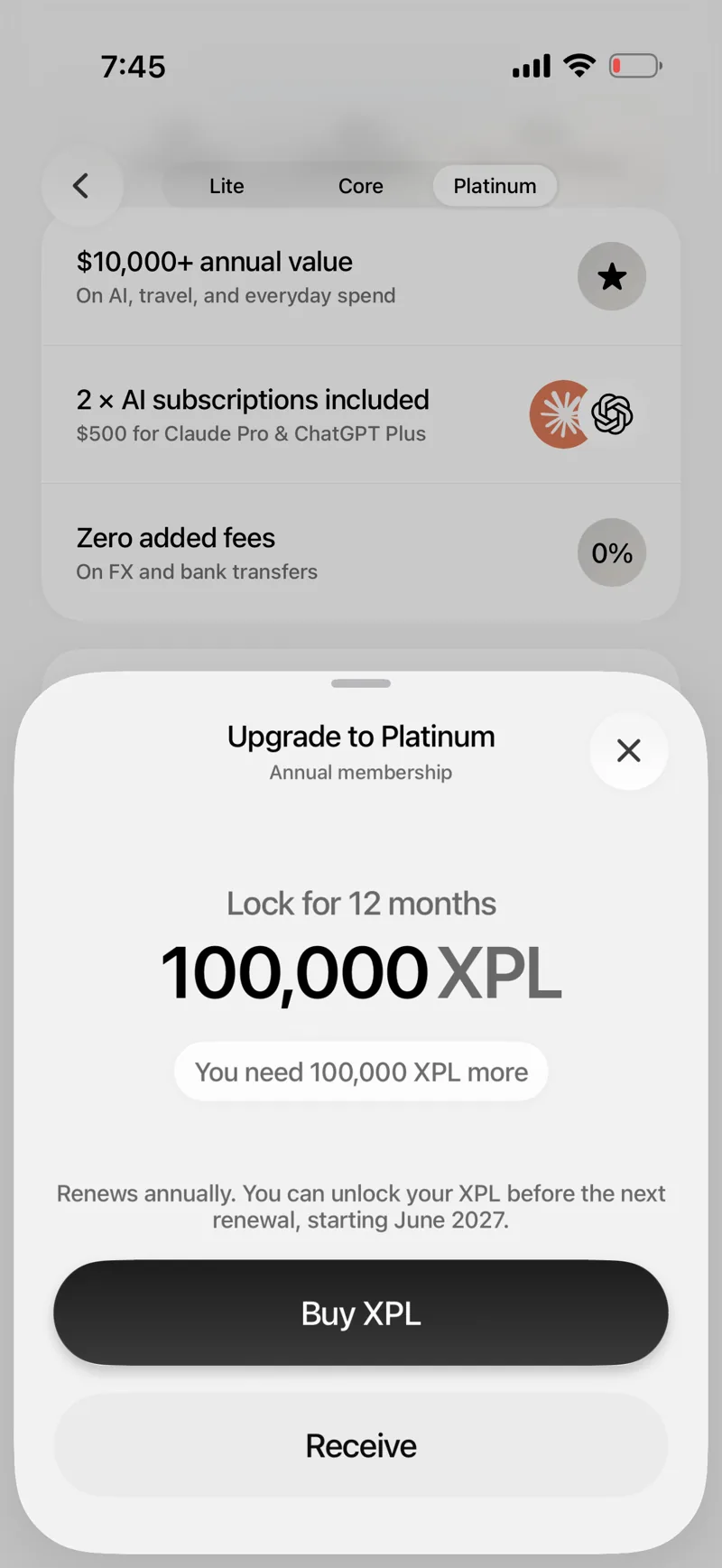

It is also the only tier with no fiat price. Access requires locking 100,000 XPL for 12 months. Plasma has not published a subscription option, so the token lock is the access path. The locked XPL is returned after the year, but you carry full XPL price exposure for the duration, which makes Platinum a different kind of decision from Lite or Core: it is a tier for people who already hold XPL or are willing to take a year-long position in it.

SpendNode app screenshot

Platinum tier overview - The 16g metal Visa Infinite*: 4% base, 10% AI, and 10% airline cashback, two AI subscription rebates (up to $480/year), and no added Plasma fees on FX or bank transfers. Plasma markets $10,000+ of annual value.

*Metal card not yet available as of June 2026; virtual cards ship at launch, with the physical card to follow.

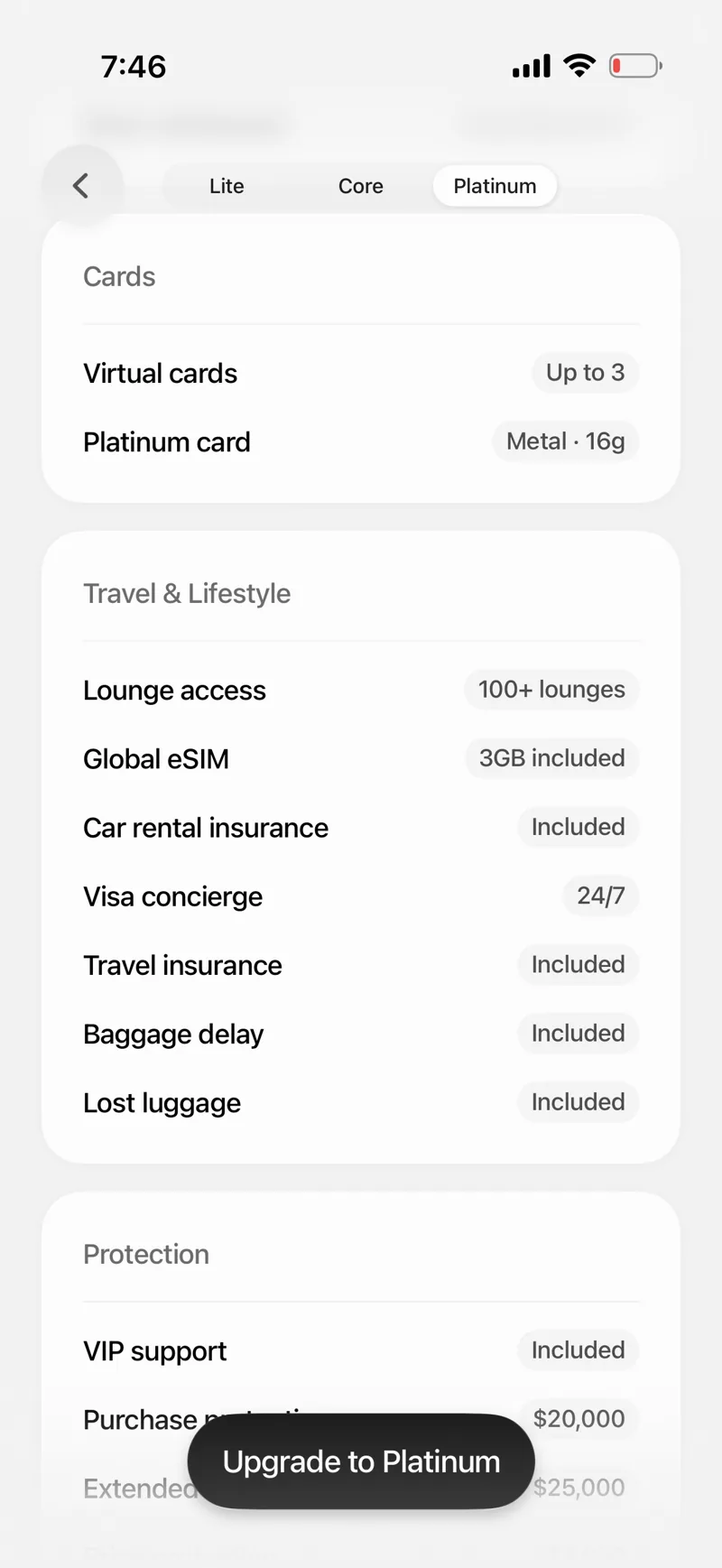

Platinum sits on the Visa Infinite product tier, Visa's premium band, which is what carries the lounge access, concierge, and travel-insurance eligibility. The card ships as a 16g metal Visa Infinite alongside up to three virtual cards, and the app runs on both iOS and Android, so the upgrade over Core is about rate, travel benefits, hardware, yield, and the AI rebates.

Card Specs: What You Are Actually Getting

Physical and Virtual Cards

The Plasma One Platinum Card ships as a 16g metal Visa Infinite, the only physical card in the lineup, and also provisions a virtual card into Apple Wallet. Platinum includes up to three virtual cards plus the metal card, the most of any tier, which suits separating travel spend, AI subscriptions, and everyday purchases onto distinct numbers.

ATM withdrawal terms are not published. Spending is tap-to-pay via Apple Wallet on iPhone and Apple Watch, the metal card, or online card-not-present checkout. The Plasma One app runs on iOS and Android.

SpendNode app screenshot

Platinum benefits - The full stack: three virtual cards plus the metal card*, discounted Visa Airport Companion lounge access, a 3GB eSIM, car-rental and travel insurance (travel accident up to $1.5M), baggage delay (up to $600) and lost-luggage (up to $3,000) cover, 24/7 Visa concierge, VIP support, and the lineup's highest protection limits ($20,000 purchase, $25,000 warranty, $4,000 price).

*Metal card not yet available as of June 2026; virtual cards ship at launch, with the physical card to follow.

Payment Network

Visa Infinite, international. The Platinum Card is accepted anywhere Visa is accepted, across roughly 150+ countries and tens of millions of merchants. Visa Infinite is the top of Visa's three consumer product tiers, above the Signature band used by Core, and it is the band that unlocks the lounge, concierge, and insurance benefits Plasma layers onto the tier.

Security Features

- Hardware-backed keys (passkeys / biometric) instead of seed phrases for account access

- In-app freeze and unfreeze with a tap

- Configurable daily spending limit ($1,000 / $5,000 / $10,000 / Custom presets)

- Real-time push notifications on every transaction

- Self-custodial wallet model: Plasma cannot move funds without an action you sign

The self-custody architecture is identical across the three tiers. The distinction worth flagging for Platinum is that your largest at-risk position is not the spendable balance - it is the 100,000 XPL you lock for a year, which is exposed to the token's price for the full term.

Getting the Card

The full step-by-step sign-up flow (waitlist, KYC, activation, funding, and daily limits) lives on the Plasma One vendor page. SpendNode's embedded referral code does not currently skip the waitlist. Platinum additionally requires locking 100,000 XPL for 12 months to unlock the tier.

SpendNode app screenshot

The XPL lock - Platinum access is a 12-month lock of 100,000 XPL, bought or received in-app. It renews annually, and Plasma states you can unlock the XPL before the next renewal, starting June 2027.

How Spending Works

Example: a $2,000 trip with flights and on-the-ground spend.

Step 1. Fund the wallet. You deposit USDT on the Plasma chain (free) or USDC on Polygon (free, under the $30k cap).

Step 2. Book the flights. You put $1,200 of eligible flights on the Platinum Card. Flight cashback is 10% on the first $500/month of airline spend (up to $600/year back), so $50 of this booking earns at the boosted flight rate; the remaining $700 earns the base rate like any other purchase.

Step 3. Spend on the ground. You spend $800 across hotels, dining, and transport at the base rate. Combined with the $700 flight remainder, that is $1,500 of base-rate spend this month, all within the first $3,000 band at 4%, about $60 in XPL. With the $50 flight boost, the trip earns roughly $110 in XPL. Cross-border fee is 0%, and FX is up to 1% (network) with no Plasma markup added on non-USD spend.

Step 4. Settlement from your balance. Each purchase settles from your self-custodial stablecoin balance on the Plasma chain. Tap, settle, done.

Step 5. Cashback distribution. Cashback pays weekly, on Thursdays, in XPL to your Rewards ledger, and may stay pending for several days before it vests. Platinum pays the lineup's top cashback rates, so this trip earns at the full band rate.

Step 6. The perks that do not depend on spend. Lounge access, the Visa concierge, travel and rental insurance, baggage protection, and a global eSIM apply to the trip independent of cashback, and the Claude Pro and ChatGPT Plus rebates sit on top.

Fees and Rates

| Fee | Amount | Notes |

|---|---|---|

| Subscription price | Not published | Access is the 100,000 XPL lock |

| XPL lock | 100,000 XPL for 12 months | Returned after the term; full token price risk during it |

| APR on purchases | 0% | Plasma reserves the right to introduce interest later |

| Cards | Included | 16g metal card plus up to three virtual cards |

| Foreign exchange fee | Up to 1%, no Plasma markup | Network FX only; Platinum adds nothing |

| Cross-border fee | 0% | No surcharge for international merchants |

| Bank withdrawal fee | Under 0.1% | Bank deposits are free; lowest of any tier |

| USDT / USDC funding | Free | USDC free up to $30,000; third-party network fees may apply |

| USD ACH / wire deposit | Free | Through Bridge |

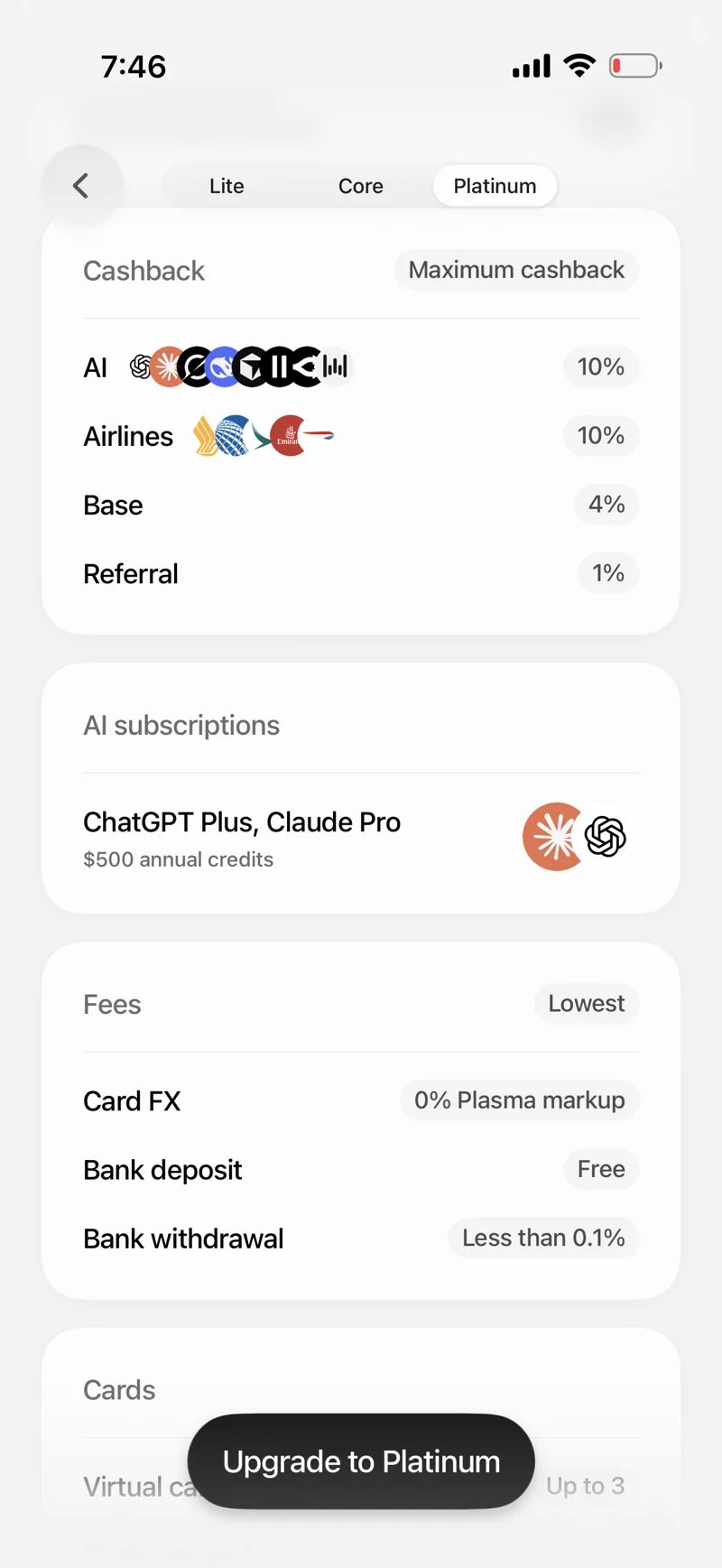

| Cashback | 4% base, 10% AI, 10% flights | Top rates in the lineup; base steps down by spend band (4% to $3k, 3% to $10k, 2% to $15k, 1% above), AI is 10/5/1% by band, flights 10% on first $500/mo; AI and flight rates replace base, not stack |

| Cash advances and balance transfers | Not available | Excluded in the Card Terms |

The real cost is the lock, not a fee. Platinum has no annual fee to recover. Its cost is opportunity cost and price risk on 100,000 XPL held for a year. At recent mid-2026 XPL prices that is on the order of $9,000 of value tied up, though the figure moves with the token. You get the XPL back after twelve months, so the question is whether a year of cashback, travel perks, the boosted yield, and the AI rebates outweighs a year of XPL price exposure and the foregone use of that capital.

Break-even framing. Because there is no cash fee, "break-even" is about whether the boosted yield plus cashback beats holding the same XPL unlocked (or deploying that capital elsewhere). The boosted 5% yield on up to $500,000 of stablecoin balance is the largest lever for users who carry a big balance; for users who do not, the case rests on the 4% base, the 10% AI and flight rates, and the travel perks.

SpendNode app screenshot

Platinum cashback and fees - 10% AI, 10% airlines, 4% base, and 1% referral, with up to $480/year of ChatGPT Plus and Claude Pro rebates. Card FX adds no Plasma markup (only the up-to-1% network fee applies), bank deposits are free, and withdrawals run under 0.1%.

Rewards and Cashback

Platinum pays cashback in XPL, like every tier, so the headline rates are denominated in a token whose dollar value moves.

The structure. Base cashback is banded by monthly spend: 4% on the first $3,000, 3% to $10,000, 2% to $15,000, and 1% above. AI spend earns 10% on the first $500/month (then 5% to $1,000, then 1%), and eligible flights earn 10% on the first $500/month. The AI and flight rates apply in place of the base rate on those purchases, not on top, and revert to the base rate once a monthly cap is reached. It pays the lineup's top rates in XPL, so Platinum keeps paying further up the spend curve than the other tiers.

The bull, bear, and neutral cases are the same shape as the other tiers. If XPL appreciates, your effective rates clear the headline; if it drops 25-50%, they fall proportionally; if it holds flat, you earn roughly the headline with holding-period drift. The difference at Platinum is scale: with a 4% base and the top boost rates, a high spender accrues far more XPL, which means more upside if the token rises and more exposure if it falls. You can swap XPL to USDT on receipt to lock the dollar value.

Referral rewards add 1% of referred users' spend for six months, the longest referral window of the three tiers.

Travel Perks and AI Rebates

Platinum is the only tier with a full travel stack, and it is where the Visa Infinite band earns its place:

- Discounted Visa Airport Companion lounge access and a Visa concierge

- Travel insurance and auto rental insurance

- Baggage delay and lost luggage protection

- A global eSIM for data abroad

- VIP support

- 10% back on the first $500/month of eligible flights (partner airlines: United, Emirates, Singapore Airlines, Cathay Pacific, British Airways)

On the AI side, Platinum rebates up to $20/month each toward Claude Pro and ChatGPT Plus (about $480/year): pay for the subscriptions with the card and Plasma reimburses up to $40/month total in USD to your cash balance. That is a step up from Core's single ChatGPT Go rebate.

For a frequent traveler who already pays for premium AI tools, the perk stack and the rebates together can represent several hundred dollars of annual value before any cashback - though, as with Core, the rebates are worth nothing unless you actually pay for those subscriptions, and lounge or insurance benefits matter only if you travel.

SpendNode app screenshot

Perks across travel and AI - The in-app benefit hub spans airline and lounge perks, VIP services, and AI tools, the categories where Platinum's AI rebates and travel stack pay back.

The Boosted 5% Yield

Platinum holders with an active tier receive a boosted, fixed 5% annual yield on the first $500,000 of stablecoin balance in the Earn vault, against the "up to 5% variable" rate the other tiers see (3.93% at our observation on Lite). For a user who parks a large stablecoin balance, this is the single most valuable part of the tier: a fixed 5% on up to half a million dollars is $25,000/year at the ceiling. Balance above $500,000 earns the standard variable rate.

The caveats matter. The rate is set by Plasma and can change; it is not a guaranteed return or a bank deposit, and the underlying vault routes to third-party DeFi protocols with smart-contract risk. The yield is most valuable for users who already hold a large stablecoin balance and would otherwise leave it idle - it is not a reason on its own to move money you would not have parked.

Multi-Chain Funding

Platinum inherits Plasma One's funding flexibility: USDT on Plasma, Polygon, Ethereum, and Arbitrum, plus USDC on Polygon, Ethereum, and Arbitrum, plus USD ACH and wire. Most self-custodial Visa cards (Tuyo on Base, Gnosis Pay on Gnosis Chain, Ready on Starknet) lock you to a single chain.

Limits and Restrictions

Daily Spending Limit

The Platinum Card uses the same user-configurable daily limit as the rest of the lineup:

| Preset | Daily Limit |

|---|---|

| Low | $1,000 |

| Default | $5,000 |

| High | $10,000 |

| Custom | User-defined (may require higher KYC tier) |

The effective limit is the lower of your set daily preset and the market value of your stablecoin balance.

Restricted Merchant Categories

The Plasma One Cashback Terms exclude a list of transactions from earning rewards: ATM withdrawals, peer-to-peer transfers, currency exchange, tax payments, gift cards and prepaid cards, money orders and cash equivalents, gambling and quasi-cash, cryptocurrency purchases, wire and balance transfers, and any spending Plasma judges to be structured to game the program.

Eligibility Caveat

Plasma One is available across 150+ countries but does not publish a full country eligibility list for opening an account. United States residents are supported, with US account services provided by Bridge Building Inc. Eligibility is confirmed at signup through KYC, and the service is unavailable to OFAC-sanctioned individuals and entities.

Is the Plasma One Platinum Card Safe?

Self-custody answers most of the failure question, but Platinum adds one exposure the other tiers do not have:

The locked 100,000 XPL. This is the distinctive Platinum risk. The tokens are locked for 12 months and returned after, but during the term you carry full XPL price risk and cannot access that capital. If XPL falls sharply during your lock, the value you get back is lower, independent of how the card performed. Size the lock as a token position you are willing to hold for a year, not as a fee.

Stablecoin balance in your wallet. Unaffected by anything that happens to Plasma the company - you retain control via your authentication method, and the chain survives the app. This is the advantage over custodial premium cards like Crypto.com, whose top tiers also require large token stakes but hold your balance as a claim against the issuer.

Stablecoin balance in the Earn vault. Exposed to smart-contract risk on the third-party protocols the vault routes to, including the balance earning the boosted 5%.

Pending XPL cashback, perks, and the AI rebates. At risk in a wind-down. Unvested XPL may not pay out, and lounge access, insurance, and the AI rebates depend on Plasma's partnerships continuing.

Card functionality. Stops if Plasma's relationship with the issuer ends. The card is issued by Rain under a license from Visa; your wallet survives.

Is the Plasma One Platinum Card a Scam?

No. The Platinum Card is issued by Rain, a Visa Principal Member, under a license from Visa, with account services through Bridge (Bridge Building Inc. for US residents, Bridge Building Sp. z o.o. for the EEA, and Bridge Building Limited elsewhere). On the Lite tier we tested, cashback paid out in XPL weekly (on Thursdays) and the Earn vault honored on-demand withdrawals - the same platform that powers Platinum.

What it is not: a deposit account. Stablecoin balances are not FDIC insured. Cashback and the boosted yield are paid in or denominated against XPL and on-chain strategies, both of which carry real risk. The standout consideration is the 100,000 XPL lock, which is a genuine year-long token position, not a scam marker but a substantial commitment to weigh on its own.

Real User Scenarios

Scenario 1: Sofia, frequent traveler and XPL holder, $5,000/month

Setup: Already holds 100,000 XPL and locks it for the tier rather than selling. Spends $5,000/month including ~$1,000/month of eligible flights across the year. Uses the lounge access and pays for both rebated AI subscriptions with the card.

Results after 12 months:

- Flight cashback at 10% on the first $500/month of flights: ~$600/year in XPL

- Base cashback on ~$4,500/month via the bands (4% on the first $3,000, then 3%): ~$1,980/year in XPL

- Claude Pro + ChatGPT Plus value: several hundred dollars she already paid for

- Lounge access, insurance, eSIM: used on multiple trips

- Cost: a year of price exposure on already-held XPL

- Verdict: "I was holding the XPL anyway, so the lock costs me liquidity, not new capital. The flight cashback, lounges, and AI rebates make this the right tier for how much I travel."

Scenario 2: Tomas, high-balance saver, $3,000/month

Setup: Parks $400,000 of stablecoins in the Earn vault and locks 100,000 XPL for the boosted yield. Spends $3,000/month.

Results after 12 months:

- Boosted 5% yield on $400,000: ~$20,000 (vs ~$15,700 at the 3.93% variable rate, a ~$4,300 uplift)

- Base cashback on $3,000/month via the bands (4% on the full first $3,000 band): ~$1,440/year in XPL

- Cost: a year of XPL price exposure on the lock

- Verdict: "The boosted yield on my balance dwarfs the cashback. Platinum pays for itself through the yield uplift alone - as long as I'm comfortable with the smart-contract risk and the XPL lock."

Scenario 3: Daniel, moderate spender weighing the lock, $1,500/month

Setup: Does not already hold XPL. Would have to buy 100,000 XPL to lock it. Spends $1,500/month, ~$200 AI, rarely flies, keeps a small balance.

Results after 12 months:

- Base cashback on ~$1,300/month via the bands (4%, within the first $3,000 band): ~$624/year in XPL

- AI cashback at 10% on ~$2,400 ($200/month, within the first $500 AI band, in place of base): ~$240 in XPL

- Travel perks and boosted yield: largely unused

- Cost: buying and locking ~$9,000 of XPL for a year, with full price risk

- Verdict: "Buying ~$9,000 of XPL just to lift my base from Core's 3% to 4% does not pencil for the ~$860 a year I would earn. Core gives me the AI rate and the rebate without the lock."

How the Plasma One Platinum Card Compares

Within Plasma One: Platinum is the travel-and-yield flagship, and it is the right tier only for two profiles - XPL holders who can lock 100,000 tokens without buying them, and high-balance users who want the boosted 5% yield. Everyone else is usually better served by Core (the AI rate and ChatGPT Go without a lock) or the free Lite tier. The base-rate jump from Core's 3% to Platinum's 4% does not, on its own, justify locking roughly $9,000 of XPL for a year.

For premium card seekers: Crypto.com runs the closest model (high cashback tiers gated behind large token stakes) but holds your balance custodially and pays in CRO. Platinum keeps custody on your side and pays in XPL, and its boosted stablecoin yield is a benefit Crypto.com's structure does not match in the same way.

Plasma One Platinum unique value: A self-custodial Visa Infinite where a year-long XPL lock unlocks the lineup's top cashback, a full travel-perk stack, a boosted 5% yield on a large balance, and premium AI rebates - best for XPL holders and high or travel-heavy spenders, not for moderate spenders who would have to buy the lock.

Who Should Use the Plasma One Platinum Card?

Platinum makes sense if you already hold 100,000 XPL (or more) and can lock it for 12 months without buying in, or you carry a large stablecoin balance and want the boosted, fixed 5% yield on up to $500,000. It rewards frequent travelers who will use the lounge access, flight cashback, insurance, and eSIM, anyone who wants both Claude Pro and ChatGPT Plus rebated, and high spenders who want the lineup's top rates.

Look elsewhere if you would have to buy 100,000 XPL just to qualify and cannot comfortably hold that position for a year.

It is the wrong tier for a moderate spender, where Core gives you the AI rate and the ChatGPT Go rebate without a lock and Lite is free; for someone who rarely travels, since the lounge, flight, and insurance perks go unused; for anyone who wants stable USD-equivalent cashback (Jupiter Global pays in USDC with no token risk); for users who rely on ATM access, since ATM terms are not published; and for New York State residents, since Earn vault services are not available there.

The Plasma One Platinum Card is a tier for a specific person: an XPL holder or high-balance, travel-heavy spender who can absorb a year-long 100,000 XPL lock. For that person, it is one of the richest self-custodial cards in 2026 - top cashback, a boosted yield that can dwarf the cashback at scale, a full travel stack, and premium AI rebates. For everyone else, the lock is the wrong shape, and Core or Lite is the better home.

Sources and Verification

All card specs, fees, limits, and product mechanics verified from:

- Plasma One Platinum tier page

- Plasma One Official

- Plasma Homepage

- Plasma One Cashback and Referral Terms

User scenarios above are composite illustrations based on the card's published mechanics and our testing of the Plasma One platform. Actual returns depend on XPL price, Earn vault yield at the time of allocation, FX schedules confirmed at signup, your use of the AI rebates and travel perks, and individual spending profiles.

Written by Aleksandar Dukic

FAQ

Does the Plasma One Platinum Card have an invite code or signup bonus?

SpendNode's Plasma One link includes the SPENDE referral code automatically, but the code does not currently skip the waitlist or provide a separate user benefit. The $10 new-user bonus is a general Plasma One offer, not a code benefit: eligible new users receive $10 after spending $100 with the card within 14 days of signup, whether or not they use a referral code. Standard signup, waitlist, and Platinum qualification requirements apply. Download Plasma One through SpendNode.

How do I get the Platinum tier?

Platinum is available to XPL holders who lock 100,000 XPL for 12 months. Plasma has not published a fiat subscription price for the tier, so the token lock is the access path. The locked XPL is returned after the 12 months, but you carry full XPL price risk for the duration.

How does Platinum cashback work?

Card spend earns 4% base cashback, 10% on AI spend, and 10% on eligible flights (up to $600/year back), all paid in XPL. There is no hard dollar cap, but the rates band by monthly spend: base cashback is 4% on the first $3,000, then 3% to $10,000, 2% to $15,000, and 1% above; AI spend earns 10% on the first $500, then 5% to $1,000, then 1% above; and eligible flights earn 10% on the first $500/month.

Platinum still carries the lineup's top rates. Referral rewards add 1% of referred users' spend for six months. The dollar value of XPL cashback depends on the token price when it is credited.

What is the Platinum yield boost?

Platinum holders with an active subscription receive a boosted, fixed 5% annual yield on the first $500,000 of stablecoin balance in the Earn vault. Balance above $500,000 earns the standard variable rate. The boosted rate is set by Plasma and can change; it is not a guaranteed return or a bank deposit.

What travel perks come with Platinum?

Platinum includes discounted Visa Airport Companion lounge access, a Visa concierge, travel insurance (accident up to $1.5M), auto rental insurance, baggage delay (up to $600) and lost luggage (up to $3,000) protection, a global eSIM, and VIP support, plus 10% back on eligible flights up to $600/year. It also rebates up to $20/month each toward Claude Pro and ChatGPT Plus.

How does Platinum airline cashback work?

Platinum members earn boosted cashback on eligible purchases with partner airlines. Where a purchase qualifies for airline cashback, the airline rate (10% on the first $500/month of airline spend) applies in place of the base rate rather than stacking on top, and once the monthly airline cap is reached the base rate applies.

Eligible airlines are United Airlines, Emirates, Singapore Airlines, Cathay Pacific, and British Airways. If an airline is not on this list, the base cashback rate applies instead. Cashback is paid in XPL.

You retain custody of your funds until the moment of spending. Your balance is not exposed to provider insolvency risk.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?

User Reviews

Reviews are moderated and may take a moment to appear.

Latest Page Changes to the Plasma One Platinum Card Review

- Plasma reworked the Platinum base-cashback bands: the 4% top rate now runs to the first $3,000/month of spend (up from $1,000), then steps to 3% to $10,000, 2% to $15,000, and 1% above

- The change earns mid-range spenders the top rate on more of their spend, while very high spenders cross into the lower bands sooner than before