PlasBit Debit Card Review 2026

PlasBit Debit Card: reloadable Visa Platinum in EUR or USD, virtual or plastic. Currently $0 issuance, loading, and monthly fees (verified July 2026), 1.5% FX, ATM free to €200/month then 2% on plastic, 30k monthly limit, loads from 48 cryptos.

SpendNode Rating for PlasBit Debit Card

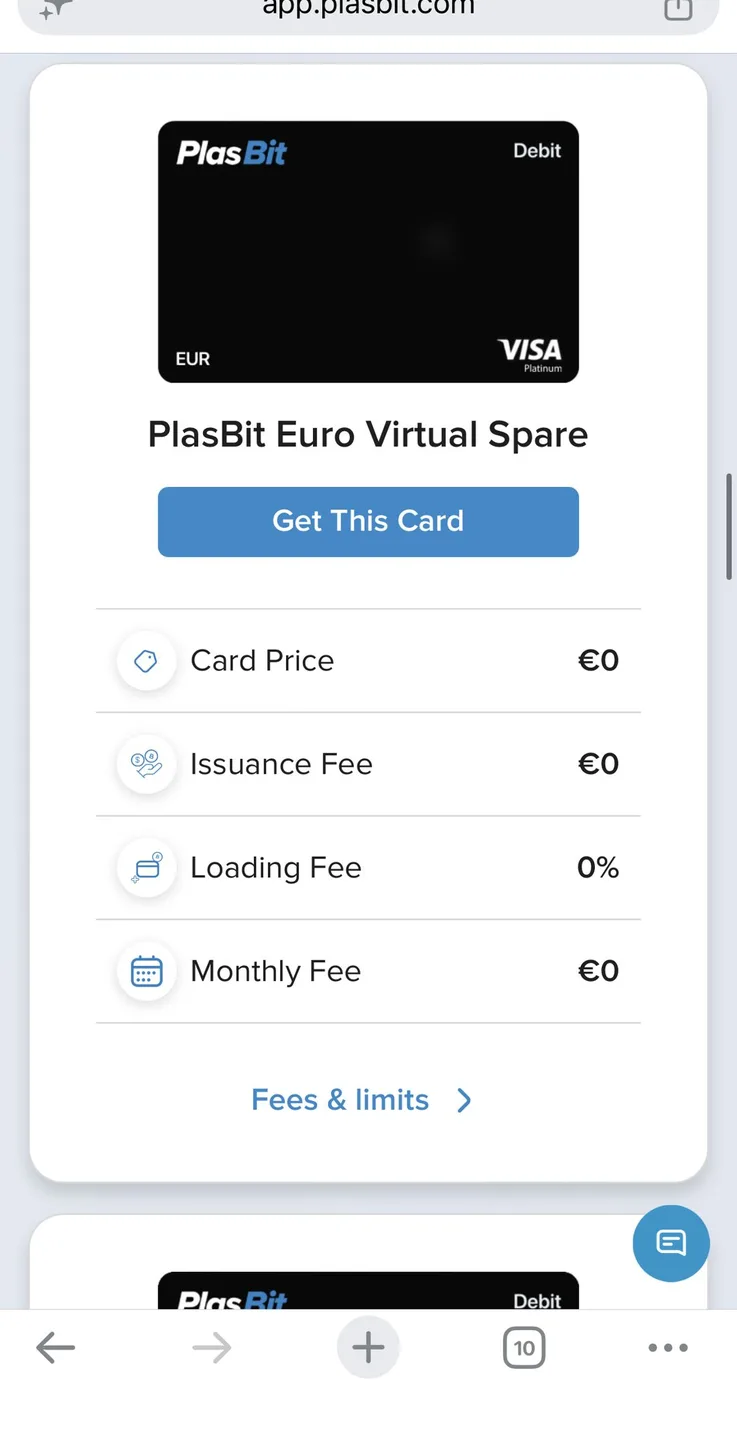

The PlasBit Debit Card pairs zero issuance, loading, and monthly fees with EUR and USD denominations, virtual and plastic formats, and a published ATM allowance on plastic. We verified the virtual-card flow and placed a plastic-card order ourselves in July 2026.

The in-account card screens make the economics easy to verify before ordering: card price, issuance, loading, and monthly fees all show zero, while FX, ATM terms, limits, and form factors are itemized. Matching the EUR or USD card to the spending currency can avoid the 1.5% FX fee. The completed virtual-card test and accepted plastic-card order support the utility and UX scores, and Apple Pay and Google Pay showed live in-account in July 2026; the web-only platform is the main remaining product limitation.

How It Competes

Cost Efficiency

4.6

Product Utility

4.2

Custody & Trust

3.8

Reliability & UX

4.3

Transparency

4.4

VIRTUAL CARD

Verified

PHYSICAL CARD

Verified

APPLE PAY

Verified

PlasBit Debit Card Overview

The zero-overhead crypto debit: load from 48 cryptos, spend in EUR or USD, pay nothing to hold it.

The PlasBit Debit Card is one of the cheapest cards in our catalog to simply hold and use: currently nothing to issue, nothing to load, nothing per month. Spend in the card's own currency and the schedule is essentially free; cross-currency spending costs 1.5%. What you give up is every form of reward, so the card suits spenders who value a clean fee page over a cashback ledger.

Fees & Charges

Annual Fee

Free

FX Fee

1.5%

ATM Fee

2%

Requirements

Supported Regions

EU, APAC, LATAM, MEA

Spendable Assets

USDT, USDC, BTC, ETH, SOL, TRX, DAI, PYUSD

On This Page

The PlasBit Debit Card is a reloadable Visa Platinum issued in partnership with Wirex BaaS, available in EUR and USD denominations as virtual or plastic cards. It currently carries zero card price, issuance, loading, and monthly fees, a 1.5% foreign exchange conversion fee, and ATM withdrawals on plastic free up to €200 per month, loaded with cryptocurrency from the custodial PlasBit wallet.

The Card That Costs Nothing to Keep

Every card review eventually reaches the same question: what does it cost to hold this thing when you are not using it? For the PlasBit Debit Card, in our account in July 2026, the answer was zero on every line. Card price 0. Issuance 0. Loading 0%. Monthly 0. Plastic delivery by DHL, also 0.

That schedule turns the usual cost analysis inside out. There is no annual fee to amortize, no loading percentage to model, and no subscription to break even against. The card's entire running cost is one number, the 1.5% FX conversion fee, and it only applies when you spend outside the card's own currency. Match the card to the currency you spend in and the meter effectively never starts.

What PlasBit takes in exchange is the entire rewards column. No cashback, no points, no yield. This is a rail, not a rewards program, and the whole product makes sense the moment you evaluate it as one.

We opened an account, verified, and ordered this card ourselves in July 2026; the fee zeros above are what the account showed. The card terms confirm free issuance and plastic delivery, while the current offer waives the standard 0.5% loading fee and monthly fee.

Card Specs: What You Are Actually Getting

Virtual and Plastic Cards

- Virtual: issues within hours of approval and phone verification, EUR or USD, up to 5 per account (the account labels extra slots "Virtual Extra" and "Virtual Spare"; identical terms)

- Plastic: black Visa Platinum with EMV chip and contactless, EUR or USD, up to 2 per account, free DHL delivery in about 5 business days

- Both are valid for 3 years, reloadable, and can unload unspent balances back to the wallet

Payment Network

- Network: Visa, Platinum tier, badged as debit

- Infrastructure: Wirex BaaS partnership, disclosed on PlasBit's cards page

- Acceptance: standard Visa acceptance worldwide; the card holds fiat (EUR or USD), so merchants see an ordinary Visa debit

- Mobile wallets: Apple Pay and Google Pay, shown as supported in-account in July 2026, alongside PayPal linking. (PlasBit's older site FAQ still describes debit as PayPal-only; the account is current.)

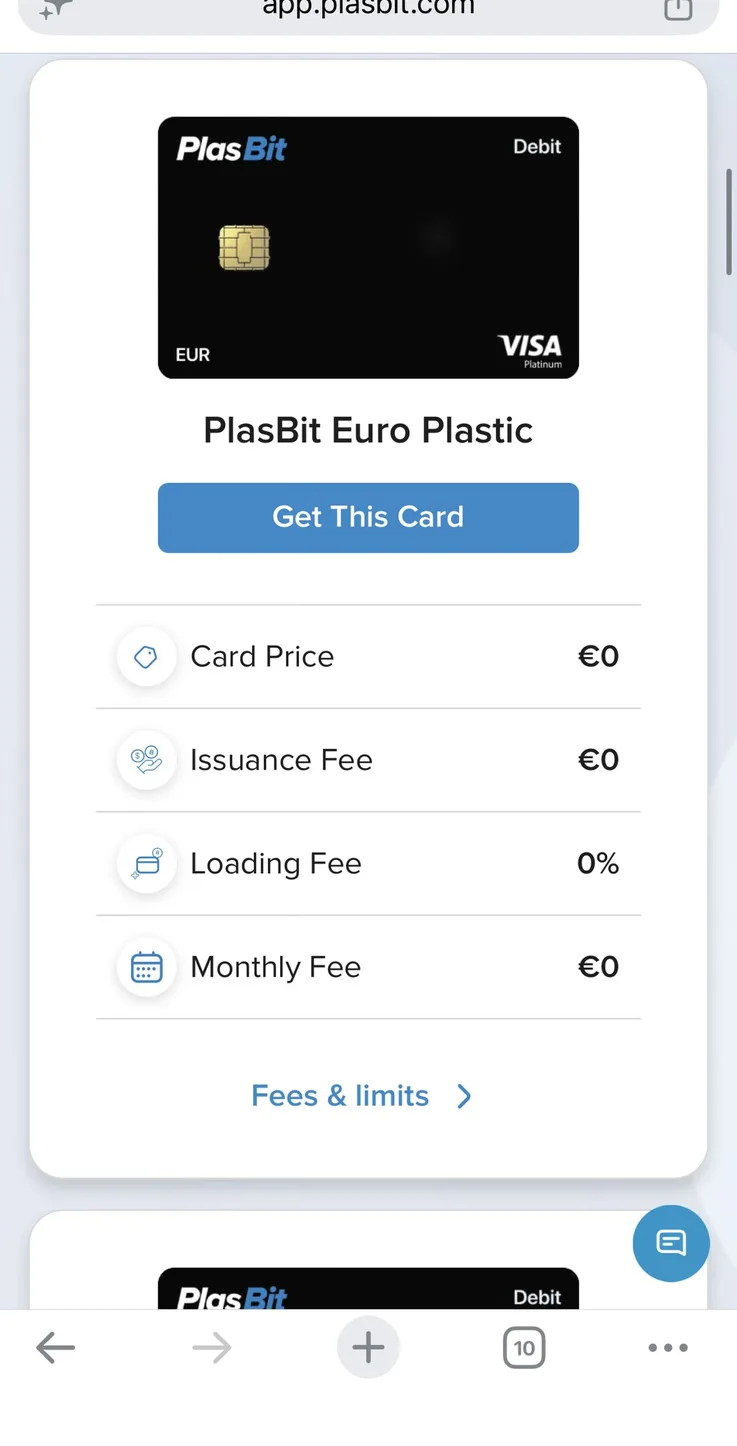

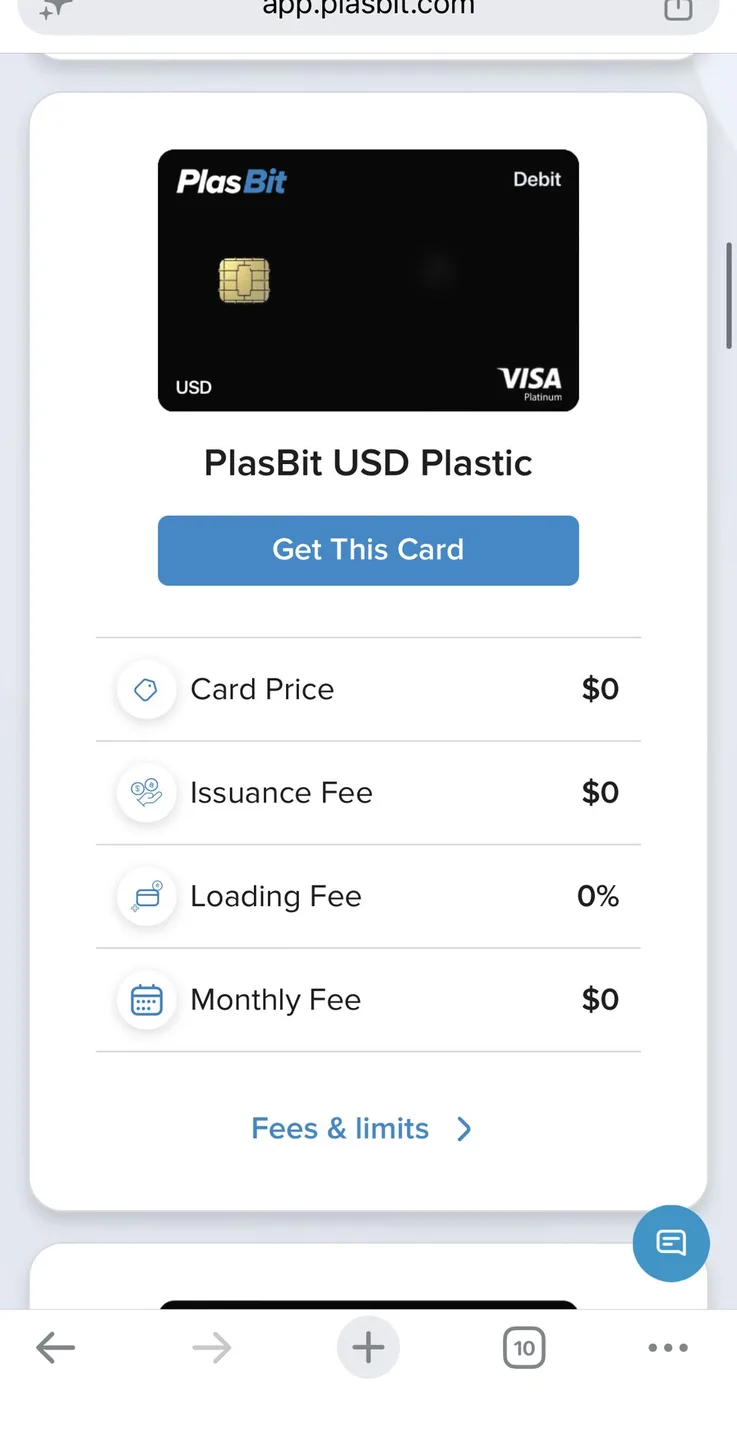

The plastic lineup in-account, July 2026: EUR and USD versions of the same black Visa Platinum, both at zero card price, issuance, loading, and monthly fees.

Security Features

- 3D Secure on online payments

- In-account card controls: lock/unlock, PIN management (PIN change free), instant transaction notifications

- Platform-side: PCI DSS certification, 2FA, withdrawal confirmation codes, and a bug bounty program

Getting the Card

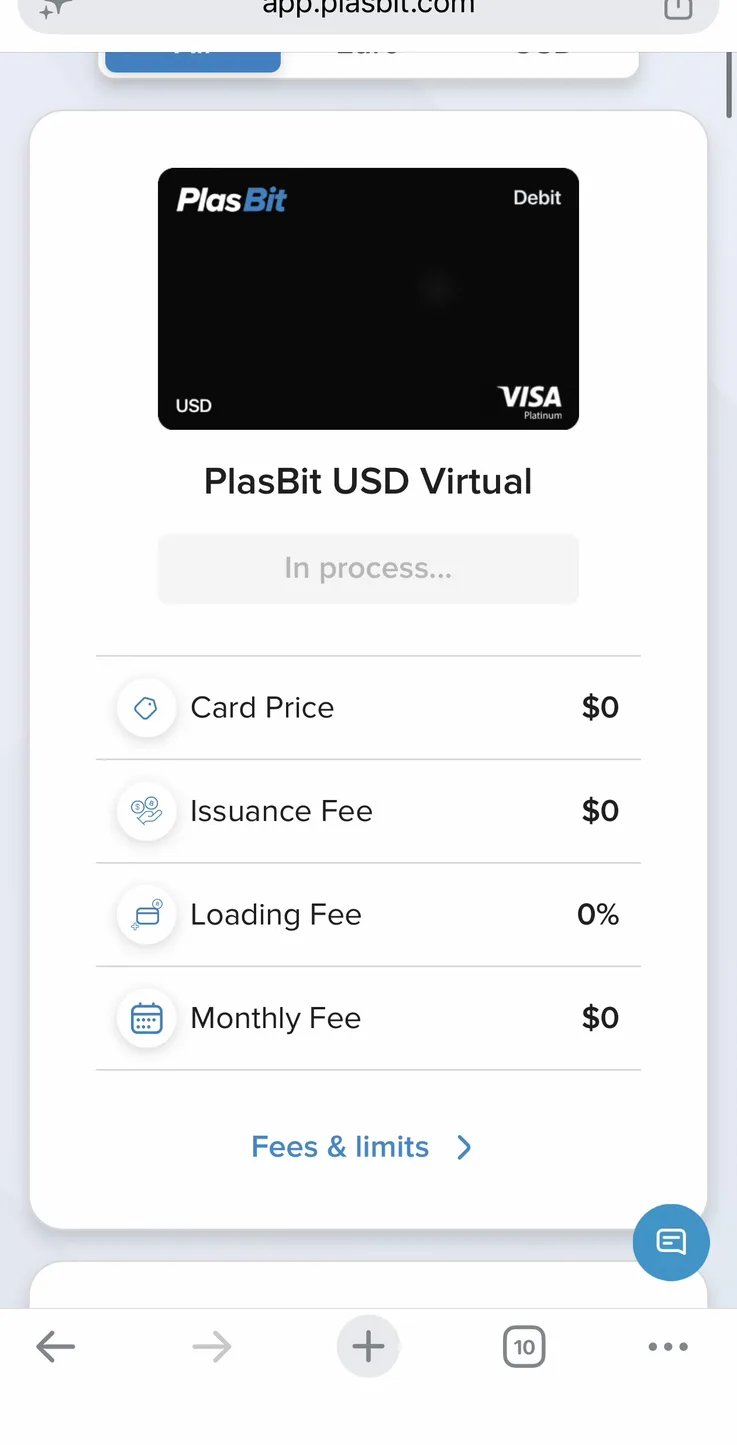

The flow is web-based; there is no mobile app. Register at plasbit.com, clear Sumsub KYC (ID plus liveness for basic, utility bill for full; PlasBit quotes about five minutes), deposit crypto, verify your phone, and order the card from the Cards tab. Virtual cards go to processing immediately; our USD Virtual order showed "in process" within seconds of submitting. The full walkthrough with screenshots lives on the PlasBit hub.

Ordering, July 2026: our USD Virtual went to processing immediately, and extra virtual slots (Spare, Extra) carry the same zero-fee schedule.

One gate to know in advance: registration is barred in 57 prohibited countries including the United States, Japan, Brazil, Pakistan, and Bangladesh, and the KYC flow separates US residents at the first screen. The official list is the reference.

How Spending Works

Example: a 60 EUR grocery run in Madrid, funded with USDT, on a EUR virtual card

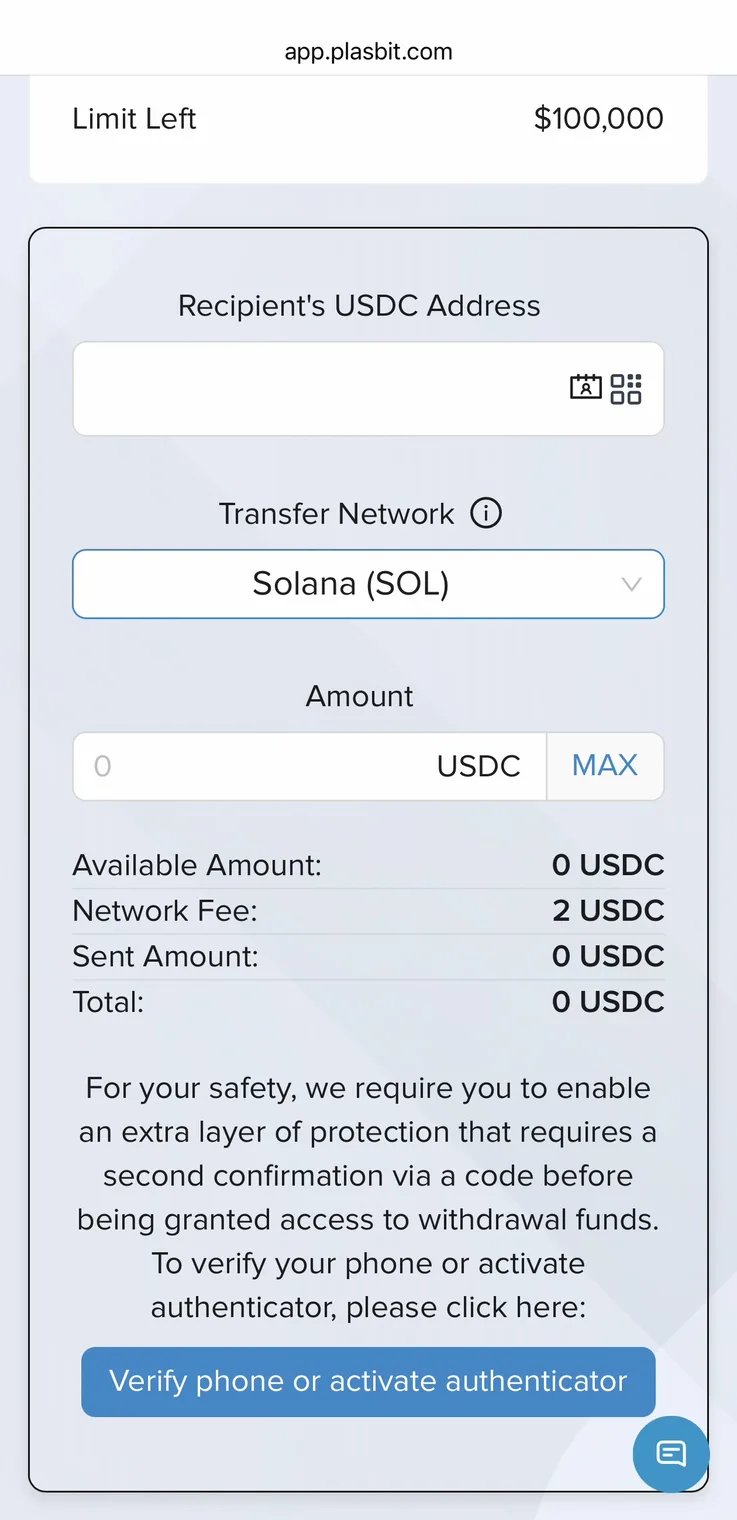

Step 1: Deposit USDT to the PlasBit wallet (TRC20, ERC20, BEP20, Solana, or Bitcoin rails for other assets).

Step 2: Load the card from the Cards tab. Conversion from USDT to EUR happens now, at load time, currently with a 0% loading fee and a 10 EUR minimum. The card holds euros from this point; crypto volatility no longer touches it.

Step 3: Pay. A EUR purchase on a EUR card carries no conversion fee: 60 EUR costs 60 EUR. The same purchase on a USD-denominated card would cross currencies and cost 1.5%, about $1.06 extra on this basket.

Step 4: Rewards: none. The transaction earns nothing, by design. What you saved instead is every fee a typical rewards card would have charged along the way.

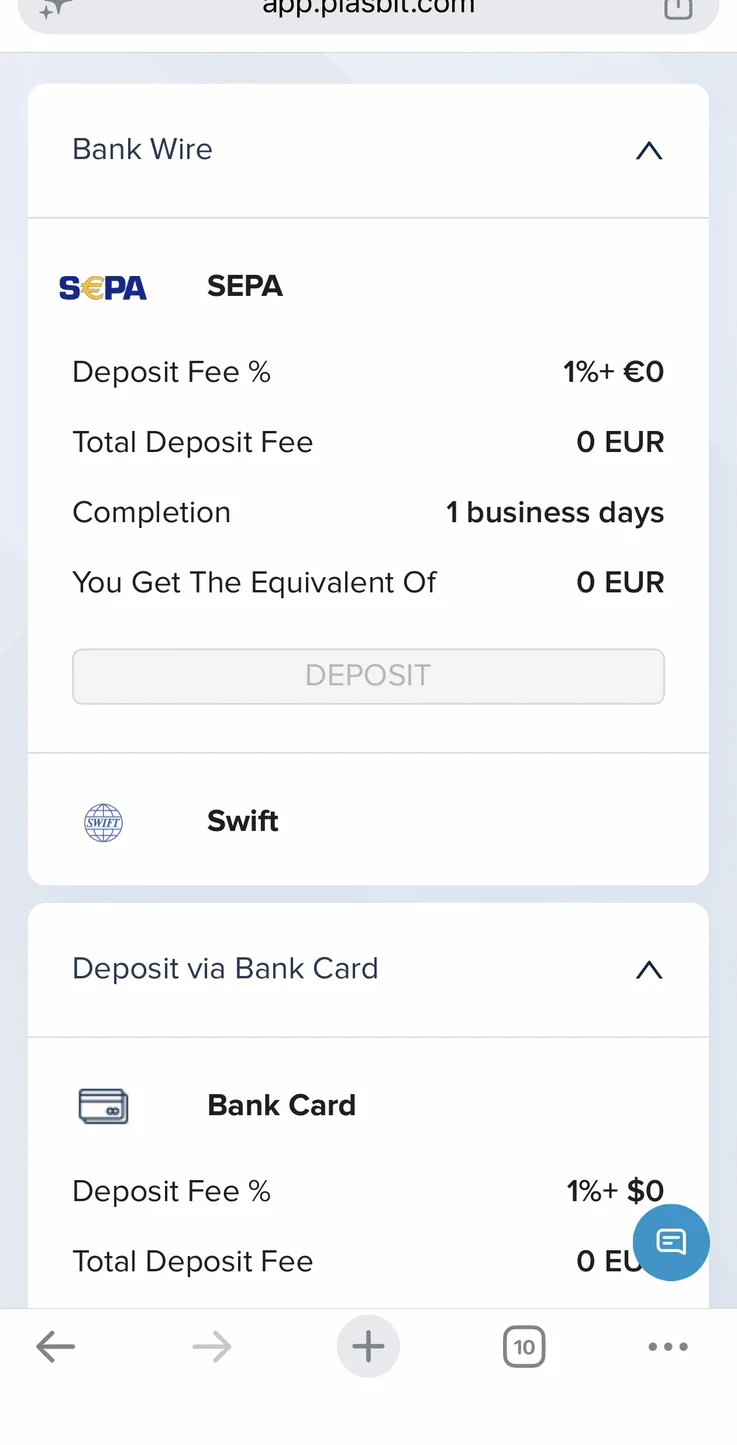

The money rails around the card, July 2026: SEPA deposits at 1% + 0 EUR, and USDC withdrawals priced per network (2 USDC on Solana, 3 on ERC20, 0.5 on BEP20).

The design decision to understand is that conversion happens at loading, not at spending. You take your crypto exit price when you load, and afterward the card behaves like an ordinary fiat debit card. That is the opposite of spend-time-conversion cards, and better for anyone who wants to convert on their own schedule rather than at the checkout counter.

Fees and Rates

| Fee | Amount |

|---|---|

| Card price / issuance | 0 (verified in-account, July 2026) |

| Loading fee | 0% |

| Monthly fee | 0 |

| FX conversion (outside card currency) | 1.5% |

| ATM (plastic only) | Free up to €200 per month, then 2% (the published schedule quotes the allowance in EUR on both denominations) |

| Plastic delivery | Free (DHL, ~5 business days) |

| PIN change | Free |

| Chargeback | 25 EUR/USD |

| Minimum load / withdrawal | 10 EUR/USD |

The zeros split into two kinds. Issuance and plastic delivery are priced at zero in the card's own Terms and Conditions, so those are contractual, not promotional. The loading and monthly fees are where the launch offer does the work: the terms list 0.5% loading and 1 EUR/USD monthly on virtual (2 on plastic) as the standard schedule, currently waived in the account. If the offer ends, that schedule is the reference point; even it would sit at the cheap end of the market. We re-verify the account regularly.

The FX fee, honestly priced

The 1.5% conversion fee is mid-pack: better than RedotPay's effective ~2.2% international cost, worse than the 1% tier of cards like Tria, far from the true-zero-FX products. But the comparison misses the point of a free dual-denomination card. Since both EUR and USD cards cost nothing, the rational setup is to hold both and route spending by currency: euros through the EUR card, dollars through the USD card, and the 1.5% applies only to third currencies. A user who spends in EUR and USD exclusively runs this card at 0% FX in practice.

For third currencies there is no way around the meter: a EUR-card user spending 1,000 EUR-equivalent in Thai baht pays about 15 EUR in conversion. Frequent spenders in unsupported currencies should weigh a lower-FX card for that slice of their spending.

ATM math

The plastic card's allowance is one of the more generous published ATM deals in our catalog: €200 free per month, then 2%, with limits of 500/day, 5,000/month, and 5 withdrawals daily. The allowance is written into the card's Terms and Conditions, quoted in EUR even on the USD card, so it is a contractual term rather than a promotion. A user withdrawing €200/month pays nothing; at €500/month the blended cost is €6, or 1.2%. ATM operators may add their own surcharges, which no card vendor controls.

Limits and Restrictions

Spending Limits

| Limit | Amount (EUR or USD) |

|---|---|

| Per transaction | 30,000 |

| Per day | 30,000 (max 15 purchases) |

| Per month | 30,000 |

| Per 3 months | 75,000 |

| Per 6 months | 100,000 |

| Per year | 200,000 |

| Load per day / month | 30,000 (unlimited load count) |

ATM Withdrawals

500 per day, 5,000 per month, 5 withdrawals per day, plastic only. The virtual card cannot withdraw cash.

Restricted Merchants

The card terms block online casinos, betting platforms, and gambling sites. Everything else follows standard Visa acceptance; no other category exclusions appear in the in-app Terms and Conditions.

The shape of the limit table matters: 30,000 in a single day is possible, but the same 30,000 is also the monthly ceiling, and the year caps at 200,000. Heavy spenders bump into the monthly ceiling well before the daily one. For a card this cheap, those are high walls: 30,000 a month covers all but the largest personal spending patterns, and volumes beyond it simply call for a second card running alongside.

Is the PlasBit Debit Card Safe?

The card is custodial end to end: PlasBit holds the crypto in the wallet, and the fiat on the card sits in the Wirex-infrastructure card program. PlasBit states user balances are backed 1:1, separated from company funds, and kept substantially in cold storage; the platform is PCI DSS certified with a bug bounty, and the company carries FINTRAC MSB registration C100000920 and Bank of Canada PSP registration RPS0014438. Registrations enroll it in AML and payments supervision; they do not insure deposits.

The failure modes to price: if PlasBit failed, wallet balances would depend on the company's stated segregation actually holding; if the card program terminated, loaded fiat would follow the program's wind-down process. Both are the standard custodial-card risks, mitigated the standard way: load what you plan to spend, keep the rest in your own wallet. The full trust analysis, including the Wirex relationship and what the Canadian registrations do and do not mean, is on the PlasBit hub.

Real User Scenarios

Scenario 1: Marta (Freelancer in Warsaw, ~900 EUR/month)

Setup: Paid in USDT by international clients. EUR virtual card for online spending, EUR plastic for stores. Monthly flow: Loads 900 EUR-equivalent of USDT (free), spends in euros (0% FX), withdraws €200 cash (inside the free allowance). Annual cost: 0 on the card itself. Her only cost is the USDT-to-EUR conversion spread at load time. Against a card charging 1% FX plus a 2 EUR monthly fee, she saves roughly 132 EUR a year. Verdict: "It does nothing except work, which is the entire reason I keep it."

Scenario 2: Tunde (Business owner in Lagos, ~$1,500/month)

Setup: Keeps working capital in USDT against naira depreciation. USD plastic card. Monthly flow: Loads $1,500 (free), spends about $1,200 at USD-priced merchants (0% FX), withdraws $300 in cash; the free allowance is published as €200 (roughly the first $215), so the overflow costs about $2. Annual cost: about $24, effectively all of it ATM overflow. The card's role is a dollar rail his local banks cannot provide at this price. Verdict: "My savings stay in stablecoins; the card is just the tap."

Scenario 3: Elena (Traveler from Vienna, ~500 EUR/month on trips)

Setup: Holds both EUR and USD virtual cards (both free) and matches the card to the destination currency. Monthly flow: In the eurozone and the US, 0% FX. On a Thailand trip, her 800 EUR of baht spending crosses currencies and costs about 12 EUR at 1.5%. Annual cost: roughly 25-40 EUR depending on how much of her travel is in third currencies. Verdict: "Free where I mostly go, priced where I occasionally go. I can plan around that."

Scenarios are composite illustrations at published rates, not customer accounts.

PlasBit Debit Card vs Other Cards

-

vs RedotPay: RedotPay has the mobile app, Apple Pay, and coverage of major markets PlasBit prohibits (Japan, Brazil, Pakistan). PlasBit is cheaper on every published line: 0 issuance against $8-10, 1.5% FX against an effective ~2.2% international, and the €200/month ATM free allowance. In markets both serve, PlasBit wins on cost and RedotPay on app experience.

-

vs KAST: KAST's free tier pays 1.5% cashback, which this card cannot answer. But KAST is USD-centric; PlasBit's EUR denomination with 1% SEPA rails serves European spending KAST does not, and its ATM allowance beats KAST's cash story. A EUR-based user can reasonably run both: KAST for USD cashback spending, PlasBit for EUR rails.

-

vs Plasma One: Plasma One's free tier pays 2% XPL cashback with an app-first, self-custodial design; it is the better product for users who want rewards and ecosystem upside. PlasBit answers with EUR support, fiat-at-load-time simplicity, and no token exposure anywhere in the stack. Choose by temperament: yield and rewards versus a flat utility.

PlasBit Debit Card unique value: the only card in our catalog offering free dual EUR/USD denomination with zero issuance, loading, and holding costs, priced for people who want a spending rail rather than a rewards program.

Who Should Use the PlasBit Debit Card?

This card fits spenders whose economics are simple and who want them to stay that way. Europeans holding stablecoins who want a EUR Visa with SEPA rails and no line items eating idle months. Users in served African, Gulf, and Southeast Asian markets who bank in USDT and need a dollar card that costs nothing to keep. Dual-currency households that can put the free EUR and USD cards side by side and route spending by denomination, running the card at effectively zero FX.

It also suits anyone building a card stack: because holding it is free, it costs nothing to keep as the EUR leg or the ATM leg of a multi-card setup, alongside a cashback card for the spending that earns. The users it does not reward are the ones optimizing for rewards; there are none here, and KAST or xPlace serve that goal better.

Sources and Verification

Fees, limits, and the card flow verified in a live PlasBit account in July 2026, including signup, Sumsub KYC, funding, a virtual-card test, and an accepted plastic-card order. Issuance and plastic delivery are contractually free; the current offer waives the standard loading and monthly fees, and we re-verify that waiver regularly.

Written by Aleksandar Dukic

FAQ

Is there a referral code for the PlasBit Debit Card?

Yes. SpendNode's PlasBit referral code is GBbiS8yG, and it applies automatically when you sign up through SpendNode's PlasBit link. The card itself is currently free to issue, load, and hold, so there is no checkout step where a code would even be needed.

What does the PlasBit Debit Card cost?

In our account in July 2026: card price 0, issuance 0, loading 0%, and monthly 0 for both EUR and USD in virtual and plastic form. Issuance and plastic delivery are contractually free. The current offer waives the terms' standard 0.5% loading fee and 1 EUR/USD virtual or 2 EUR/USD plastic monthly fee. The running costs are 1.5% FX outside the card currency, 2% on plastic ATM withdrawals past the free €200 monthly allowance, and a 25 EUR/USD chargeback fee.

Can I withdraw cash with the PlasBit Debit Card?

Only with the plastic card. ATM withdrawals are free up to €200 per month (the published schedule quotes EUR on both denominations), then cost 2%, with limits of 500 per day, 5,000 per month, and 5 withdrawals per day. The virtual card cannot be used at ATMs.

Does the PlasBit Debit Card work with Apple Pay and Google Pay?

Yes. Apple Pay and Google Pay showed as supported on the debit cards in our account in July 2026, alongside PayPal linking. PlasBit's older site FAQ still describes the debit cards as PayPal-only; the account is the current source. The plastic card also pays in-store through its contactless EMV chip.

How do I load the PlasBit Debit Card?

From the PlasBit wallet: deposit any of the 48 supported cryptocurrencies (USDT, USDC, BTC, ETH, SOL, TRX, and others across 5 networks), then transfer to the card in the Cards tab. Loading is instant, currently free, and the minimum is 10 EUR/USD per load. Conversion from crypto to the card's fiat currency happens at the point of loading.

This is a debit card. Some merchants with pre-authorization holds (hotels, car rentals) may temporarily hold funds beyond the transaction amount.

Your funds are held by PlasBit. If the provider faces insolvency, your balance may be at risk. This card does not offer self-custody protection.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?

User Reviews

Reviews are moderated and may take a moment to appear.