SpendNode Rating for Peanut

Peanut is building the account first and the card second, and the custody mechanism is concrete rather than marketing. The issuer is young and the card is still behind a beta gate.

Fee transparency, the custody design, and the breadth of the money rails all score well, and the launch buzz has made it one of the more talked-about new issuers of 2026. What holds the score back is history: a waitlist-gated beta, terms that reserve future fees, and an operator that still has to prove itself in the open.

Issuer Snapshot

Editorial vendor score stays separate from user reviews. Methodology

Product Quality

4.0

Trust & Custody

4.0

Fee Transparency

4.1

Operational Reliability

3.7

Market Relevance

3.8

On This Page

Peanut is a self-custodial money app built by Squirrel Labs that combines a passkey-secured smart wallet, free bank transfers across SEPA, ACH, UK Faster Payments and Mexico SPEI, QR payments in Argentina and Brazil, and a free virtual Visa Platinum card funded by the user's stablecoin balance. The card is in closed beta as of July 2026.

What Is Peanut?

Most crypto cards are cards first and wallets second. Peanut inverts that. The product is a self-custodial dollar account on the blockchain - your USDC sits in a smart wallet only your passkeys control, and Peanut states plainly that it cannot freeze or seize your funds.

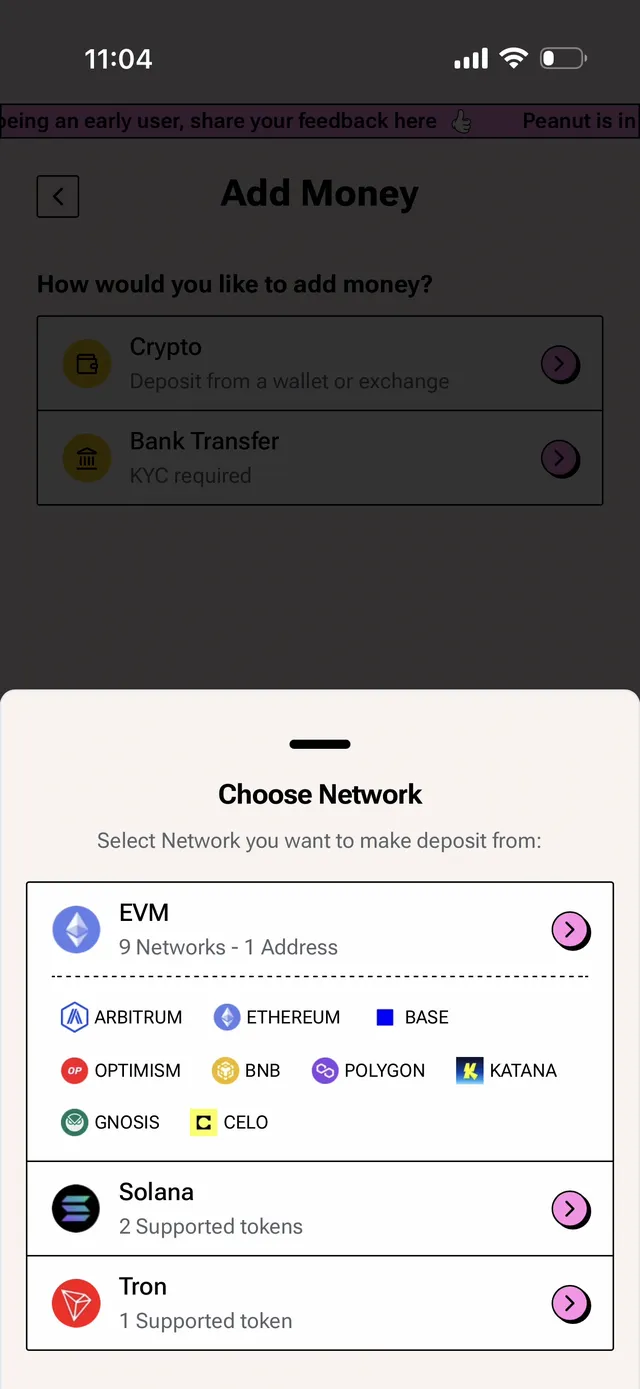

Around that wallet it has built free rails in and out: crypto deposits on 11 networks with gas covered, free SEPA and ACH bank transfers, UK Faster Payments, Mexico SPEI, and QR payments at Mercado Pago and Pix merchants in Argentina and Brazil. The virtual Visa Platinum card, launched into closed beta in May 2026, is simply the newest way to spend that balance - at roughly 150 million Visa-accepting merchants.

That ordering matters for how you should evaluate it. There is no cashback program and no token to farm. The pitch is custody, cost, and geography: KYC accepts a passport or national ID from any country, with no local DNI, CPF, or SSN required anywhere. For people whose money lives across borders - nomads, expats, remote workers paid in stablecoins - that combination is rarer than another 2% cashback card.

The Ecosystem

Peanut Visa Platinum Card - Free virtual Visa Platinum funded from the self-custody balance. $0 annual and monthly fees, 0% added on USD purchases, Visa's 1% International Service Assessment on non-USD purchases. Apple Pay and Google Pay via manual add. Closed beta - the app is invite-only, and SpendNode's invite code spendnode gets you in and bumps you up the card waitlist. A physical card is planned.

The card sits inside the broader money app, and the app is what determines where the card is useful:

- Bank rails (via Bridge): free ACH and wire deposits in the US, free SEPA transfers across 41 SEPA-zone countries with 90% arriving in under 20 minutes, UK Faster Payments settling in seconds, and Mexico SPEI. No hard limits; transactions above $100,000 may trigger review.

- LATAM rails (via Manteca): bank deposits and withdrawals in Argentina, Brazil, Colombia, Peru, Costa Rica, Chile and more, with a combined $2,000/month fiat limit that can be raised with additional documentation.

- QR payments: Mercado Pago QR at 1M+ merchants in Argentina and Pix at 150M+ endpoints in Brazil, converting at the direct cripto dolar market rate that Peanut says runs roughly 2-11% better than the regulated MEP rate credit cards use in Argentina, and sidesteps Brazil's IOF tax on transfers.

- Crypto: deposits and withdrawals worldwide with no limits and no verification required. USDC is the balance currency; USDT and DAI auto-convert at market rate with no conversion fee.

Available crypto cards by Peanut in July 2026

1. Peanut Visa Platinum Card

Non-custodial spending at 150M+ Visa merchants

Technology: How the Non-Custodial Card Actually Works

"Non-custodial card" is a claim several vendors stretch. Peanut's mechanism is specific enough to evaluate. Your stablecoins live in your own smart account, deployed on Arbitrum and secured by device passkeys rather than a seed phrase.

At card setup you approve a single scoped, session-key permission - one passkey tap. That permission authorizes exactly two movements: funds into the card program's collateral at the moment a payment is funded, and withdrawals to recipients you sign for. Peanut cannot reach the balance for anything else.

When you tap the card, the quoted amount moves from your wallet into collateral, converts at the rate shown, and settles to the merchant in local currency as a normal Visa transaction. Until that moment, the balance never left your custody.

The card terms describe this as a secured account: the collateral in your linked wallet backs each charge, and your spending capacity equals the balance backing the card. One practical consequence we noted from early user reports: after a card payment there is a short hold before that collateral is usable again, which is the settlement window doing its job.

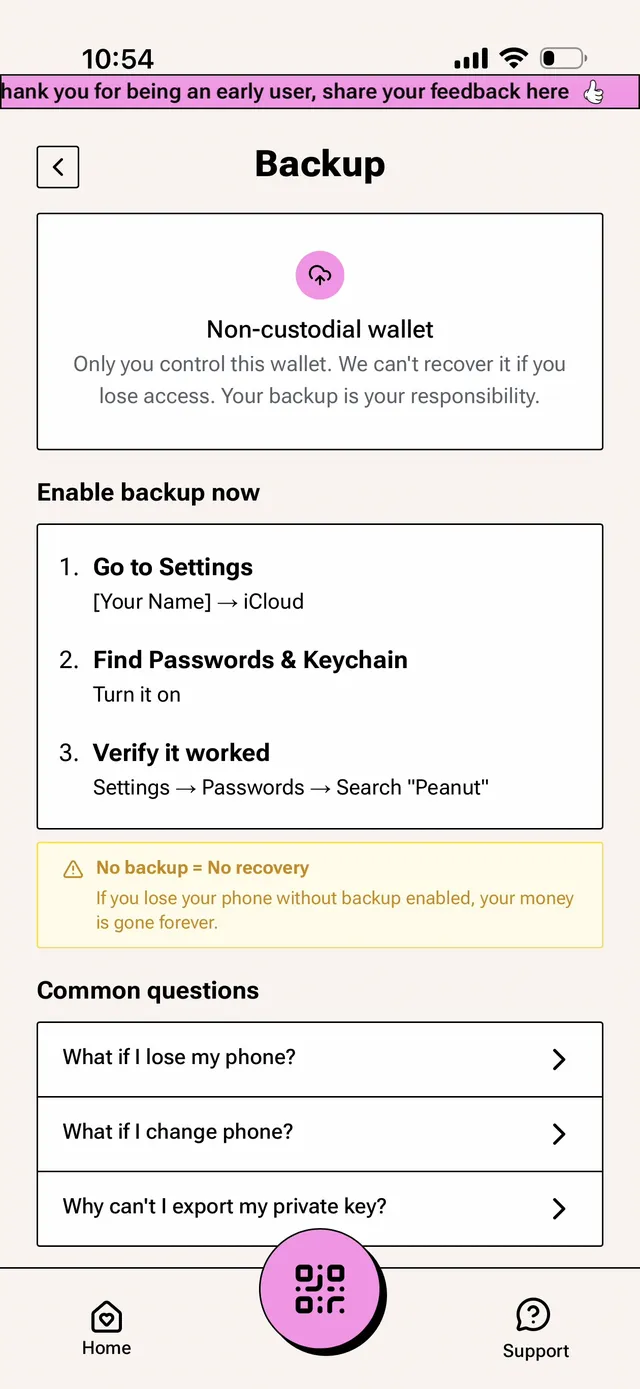

The passkey model deserves equal scrutiny. There is no private key export and no recovery desk. Peanut's own backup screen is blunt about it: no backup means no recovery, and losing your phone without a synced passkey means the money is gone. Passkeys also do not sync automatically between Apple and Google ecosystems, so a platform switch requires deliberate backup steps. This is real self-custody with real self-custody consequences.

Countries and Availability

Peanut is available in 59 countries as of July 2026. We count a country here when at least one active Peanut card variant lists it, so individual product pages may be narrower.

Available Regions

Africa

Kenya (KE), South Africa (ZA), Tanzania (TZ)

Americas

Argentina (AR), Brazil (BR), Canada (CA), Chile (CL), Colombia (CO), Costa Rica (CR), Mexico (MX), Peru (PE), United States (US)

Asia

Indonesia (ID), Japan (JP), Malaysia (MY), Pakistan (PK), Philippines (PH), Singapore (SG), South Korea (KR), Thailand (TH), Turkey (TR), United Arab Emirates (AE), Vietnam (VN)

Europe

Andorra (AD), Austria (AT), Belgium (BE), Bulgaria (BG), Croatia (HR), Cyprus (CY), Czech Republic (CZ), Denmark (DK), Estonia (EE), Finland (FI), France (FR), Germany (DE), Gibraltar (GI), Greece (GR), Hungary (HU), Iceland (IS), Ireland (IE), Italy (IT), Latvia (LV), Liechtenstein (LI), Lithuania (LT), Luxembourg (LU), Malta (MT), Monaco (MC), Netherlands (NL), Norway (NO), Poland (PL), Portugal (PT), Romania (RO), Slovakia (SK), Slovenia (SI), Spain (ES), Sweden (SE), Switzerland (CH), United Kingdom (GB)

Oceania

Australia (AU)

Major Restricted Markets

These major markets are not currently listed for this vendor. Confirm eligibility with the issuer before applying, especially where card tiers have different country rules.

Africa

Egypt (EG), Nigeria (NG)

Asia

China (CN), Hong Kong (HK), India (IN), Taiwan (TW)

Oceania

New Zealand (NZ)

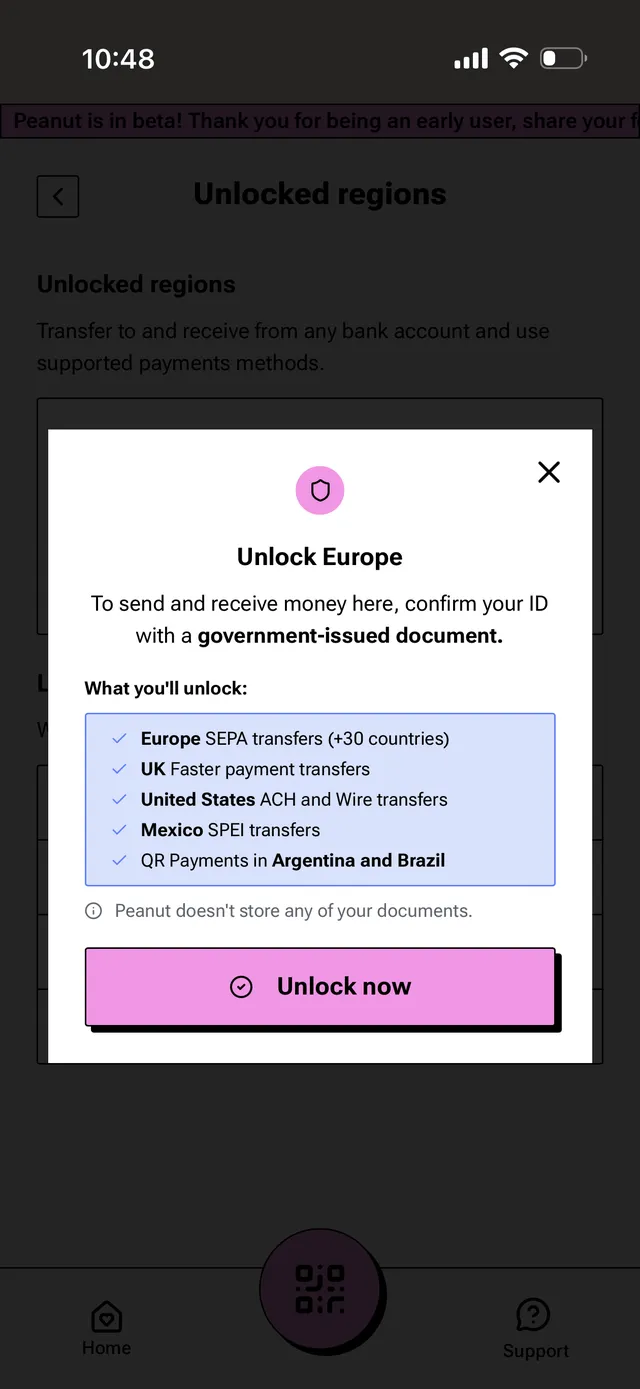

Regions unlock separately in the app. Verifying for Europe or North America unlocks the full Bridge stack - SEPA, UK Faster Payments, US ACH and wire, Mexico SPEI, plus QR payments in Argentina and Brazil. A LATAM verification unlocks local bank transfers and the same QR rails.

Users everywhere else can still verify and use QR payments when traveling, and crypto deposits and withdrawals work worldwide without any verification. Sixteen more markets - from Canada and Australia to the Philippines, Turkey and Kenya - currently get the digital-dollar account with local spending rails on the roadmap (Interac, UPI, PromptPay, GCash, M-Pesa and others are named).

The restricted list is short: North Korea, Iran, Cuba, Syria, Crimea, Russia, Belarus, and Myanmar.

Fees and Rates

Peanut advertises "no fees" loudly. The claim mostly survives contact with the fee schedule, with two honest asterisks.

| Operation | Advertised | Reality |

|---|---|---|

| Card creation, annual, monthly | Free | Free, confirmed in card terms |

| Crypto deposits/withdrawals | Free | Free, gas covered, $1 minimum withdrawal |

| Bank transfers (SEPA, ACH, SPEI, FPS) | Free | Free from Peanut; your bank may charge for outgoing wires ($25-80) |

| Card spend, same currency | Free | Free, no Peanut fee |

| Card spend, non-USD | "No Peanut fee" | Visa's exchange rate + 1% ISA network fee |

| Currency conversion in-app | "No fees" | Provider FX spread of ~0.5% (EUR/USD) to ~0.8% (USD to ARS/BRL), passed through at cost |

The first asterisk is the 1% International Service Assessment on cross-currency card purchases. Peanut is right that it is a Visa network fee rather than a markup, but you pay it either way, so we count Peanut as a 1%-FX card for non-USD spending - the same effective rate as Payy and Rain-issued Jupiter cards, and better than the 1.5-2% many custodial cards charge.

The second is the conversion spread on fiat rails: real, disclosed, and small, but not zero.

The card terms also reserve legal ceilings: a cross-border fee of "up to 1%" on top of FX, and the right to introduce interest later (the card runs at 0% APR with $0 late and returned-payment fees today). The live fee pages and in-app quotes show neither being charged now. We flag them because terms-reserved fees have a way of materializing after betas end.

Rewards and Cashback

There is no cashback program, and Peanut does not pretend otherwise. The incentive layer is one welcome credit: complete KYC, spend your first $100 on the card, and $10 lands in your balance, subject to eligibility and program terms. Refer a friend who activates the same way and you both collect $10.

The app's points and achievements are gamification, and Peanut's own terms are unusually blunt about it: points are promotional only, carry no cash value, and can be modified or revoked at any time. No token, no airdrop, and no redemption path has been announced. If earning on spend is what you want from a card, look at our cashback rankings instead - Peanut competes on custody and cost, not rewards.

How to Apply for the Peanut Crypto Card

Peanut is invite-only during closed beta, and the card adds its own waitlist on top. Three ways in:

- Badge holders. Peanut OG, Devconnect BA, and Arbiverse badge holders (about 3,400 whitelisted wallets) go straight through - sign in and the badges are checked automatically.

- SpendNode's invite code. Signing up through our link applies the code spendnode, which opens the app (a code is required to create an account at all) and bumps you up the card waitlist.

- The plain waitlist. Without a code or badge, admission runs in waves of roughly 20 people per week, in order.

Once your turn comes: complete KYC via Persona with a passport or national ID from any country (under 2 minutes for most users), and the virtual Visa Platinum is issued free. Fund it with USDC, USDT, or DAI on any of the 11 supported networks and it is ready to spend.

Trust, Security, and Regulation

The corporate structure takes some assembling. The app and platform belong to Squirrel Labs Ltd, London. The card program is issued by Third National under a Visa license, with the card terms governed by Puerto Rico law and disputes routed to AAA arbitration. The international card program requires cardholders to attest they are not US citizens - the US is served as an app market (ACH, wires), but the card program itself is aimed outside the US.

Fiat rails run through named, established providers: Bridge (the Stripe-owned stablecoin infrastructure company) for US, Europe, UK and Mexico, and Manteca for LATAM. Identity verification runs through Persona, which is SOC 2 Type 2 and ISO 27001 certified; Peanut stores only the verification result, not your documents.

What Peanut is not: a bank, an e-money institution, or a deposit-taker. There is no FSCS or FDIC protection because there is no deposit - your USDC is in your own wallet. The protections that matter here are Circle's USDC reserve backing and the correctness of Peanut's smart contracts, not a government scheme. The terms are equally direct that Peanut Protocol is an "experimental project."

What Happens If Peanut Fails?

This is where the self-custody architecture earns its keep, and the analysis differs sharply from custodial competitors.

Your balance: held as USDC in your own smart account on Arbitrum. If Squirrel Labs shut down tomorrow, the funds would still be yours, controlled by your passkeys, withdrawable to any external wallet.

The realistic failure risk is operational rather than custodial: if the Peanut app disappeared, you would need the smart account to remain accessible through standard tooling, and recovering a passkey-controlled account without the vendor's interface is harder in practice than holding your own seed phrase. Non-custodial removes the exit-scam and bankruptcy-estate scenarios; it does not remove smart-contract and access-tooling risk.

The card: dies with the program. Any $10 welcome credit not yet claimed and any in-app points (which carry no cash value by design) would be lost. Collateral mid-settlement at the moment of failure is the one sliver of funds actually exposed, and it is bounded by whatever single payment was in flight.

Compare that to custodial cards: an exchange card's balance is a claim on the company; in an insolvency you join the creditor queue, as CoinFLEX and FTX users learned. Peanut's worst case is losing a spending tool. A custodial vendor's worst case is losing the money.

Real User Scenarios

Mariana, Argentine designer paid in USDC ($1,500/month). She deposits USDC on Solana (free, under a minute), pays daily expenses by Mercado Pago QR at the cripto dolar rate, and keeps the card for online purchases.

Versus running pesos through a credit card at the MEP rate, Peanut's rate advantage of roughly 2-11% saves her somewhere between $30 and $165 a month on $1,500 of spending - $360 to $1,980 a year, with the exact figure swinging with Argentina's rate gap. Her fiat operations sit under the $2,000/month LATAM limit. "The QR rate is the product for me. The card is a bonus."

Tomas, EU-based nomad ($2,500/month, half in EUR). His EUR spending routes through the card as non-USD purchases: Visa's rate plus the 1% ISA costs him about $12.50 a month on $1,250 of EUR spend, roughly $150 a year.

A typical EU bank card charging 2% FX on the same pattern costs $300; a 0%-FX specialist like Gnosis Pay beats him on rate but requires an EEA/UK footprint and a different custody setup. Free SEPA in and out means moving money costs him nothing. "I pay about 1% for spending dollars in Europe with nobody able to freeze the account. Fine trade."

Dev, remote worker in the Philippines paid in USDT ($1,000/month). The Philippines is a digital-dollar-only market for Peanut today - no local bank rails yet. He deposits USDT on Tron (free), holds dollars in self-custody, and spends through the card at Visa merchants and ATMs.

For him the card is not a bonus but the only Peanut spending rail that works locally, at 0% added on USD-denominated online spend and ~1% on peso purchases. GCash integration is on Peanut's roadmap but not live. "It replaced the exchange-withdraw-to-bank loop, which is what I wanted gone."

Peanut vs Other Cards

- vs Payy Card: The closest architecture - self-custodial, no rewards, $0 fees, ~1% on non-USD. Payy leans on zk-privacy rails; Peanut counters with far broader money rails (SEPA, ACH, FPS, SPEI, LATAM QR), 11 deposit networks, and any-nationality KYC. Both are virtual-only and beta-gated.

- vs Gnosis Pay Card: Gnosis Pay pairs self-custody (Safe wallet) with up to 5% cashback for GNO stakers and true 0% FX on the base rate, but it is EEA/UK-centric and physical-card oriented. In Europe, Gnosis Pay wins on spending economics; Peanut wins the moment your life leaves Europe.

- vs Plasma One Card: Plasma One is the stablecoin-neobank comparison - 166-country reach and banded cashback, but a custodial-style app model with tiered FX markups. Peanut trades the rewards for custody and cheaper rails.

Who Should Use Peanut?

Peanut fits you if you hold stablecoins and want to spend them without giving up custody - the wallet-until-payment model survives a reading of the card terms - and if your financial life crosses borders, since any-nationality KYC plus SEPA, ACH, Faster Payments, SPEI and LATAM QR all sit under one balance.

It is an especially strong fit in Argentina and Brazil, where the cripto dolar QR rate and IOF avoidance are worth more than most cashback programs, and for anyone who wants a $0-fee card and accepts ~1% on non-USD spending as the total cost.

It is a weaker fit if rewards drive your choice, because there is no cashback and the $10 welcome credit is the entire incentive program. The same goes if you want a mature, generally-available product (this is a closed beta, and even a boosted waitlist spot still means waiting), if you are not confident managing passkey backups (lose the passkey, lose the wallet, no recovery desk), or if you need a physical card or push-provisioned mobile wallets today - both are still on the roadmap.

Verdict

Peanut is the most credible attempt we have reviewed at a self-custodial bank-account replacement, and the card is best understood as its spending arm rather than as a standalone product competing on rewards.

The fee posture is honest ($0 everywhere Peanut controls, ~1% where Visa's network takes its cut), the custody mechanism is concrete rather than marketing, and the geography - any-nationality KYC, free bank rails on three continents, QR spending in LATAM - targets people the incumbents systematically bounce.

Against it: no rewards at all, a product still in closed beta, passkey risk that shifts responsibility entirely onto you, and a young company whose card terms reserve room to add fees later. On access, the invite code spendnode through SpendNode's link opens the app and moves you up the card queue - the wait shrinks, though it does not vanish.

If your life fits its map, few accounts cover more of it. If you are optimizing rewards per dollar in one country, a cashback card will serve you better.

Fees and ROI framework

There is no annual fee at any level, so break-even is immediate - the card cannot cost you standing fees. The working costs are transactional: ~1% (Visa ISA) on non-USD card purchases, a ~0.5-0.8% provider spread on fiat conversions, and $0 on same-currency card spend, deposits, withdrawals, and transfers.

- At

$500/monthof non-USD spending: ~$5/month, ~$60/year in network FX cost - At

$1,500/monthmixed (one-third non-USD): ~$5/month, ~$60/year - At

$3,000/monthUSD-denominated: $0 in Peanut-side costs

With no cashback, the ROI question is savings-based, not earnings-based: what you keep versus your current card's FX markup (typically 2-3% at banks), plus the LATAM rate advantage where it applies. A user replacing a 3%-FX bank card for $1,000/month of foreign spending keeps about $240/year with Peanut.

Availability and compliance notes

Available across 55+ countries: the US, UK, 41 SEPA-zone countries, Mexico, and named LATAM markets (Argentina, Brazil, Colombia, Peru, Costa Rica, Chile) with full fiat rails; Canada, Australia, nine Asian markets, UAE, Turkey, Kenya, Tanzania and South Africa currently as digital-dollar accounts with card spending. Restricted: North Korea, Iran, Cuba, Syria, Crimea, Russia, Belarus, Myanmar.

KYC via Persona with any passport or national ID; verification is per payment provider (Bridge and Manteca separately). Card network: Visa. The card program is issued by Third National and is in closed beta - waitlist admission runs in small weekly waves, with Peanut OG, Devconnect BA, and Arbiverse badge holders whitelisted. The app itself is invite-only: signing up through SpendNode's link applies the code spendnode, which opens the app and improves your card waitlist position.

Sources and Verification

- Peanut official site

- Peanut card page

- Peanut fees and pricing

- Peanut supported countries and regions

- Peanut card launch announcement

Data verified against Peanut's published pages, card terms (effective 2026-06-01), and our own walkthrough of the beta app in July 2026. Named user scenarios are composite illustrations based on published rates.

Written by Aleksandar Dukic

Frequently Asked Questions

Is Peanut crypto card available in the United States?

Yes. Peanut crypto card is available in the United States.

What is Peanut?

Peanut is a self-custodial money app from Squirrel Labs that combines a passkey-secured smart wallet with free bank transfers (SEPA, ACH, UK Faster Payments, Mexico SPEI), QR payments in Argentina and Brazil, and a virtual Visa Platinum card. Your stablecoin balance stays in your own wallet, and the card spends it wherever Visa is accepted - roughly 150 million merchants.

Is Peanut custodial?

No. Funds sit in a smart wallet only you control, secured by device passkeys. Peanut states it cannot freeze, seize, or move user funds; a scoped session-key permission authorizes movement only into the card program's collateral at payment time or out to recipients you sign for.

The flip side is responsibility: there is no private key export and no recovery desk. If you lose your device without a passkey backup, the wallet is gone.

How do I get the Peanut card?

Peanut is invite-only: the app itself requires an invite code, and the card sits behind a closed-beta waitlist that admits roughly 20 people per week, with Peanut OG, Devconnect BA, and Arbiverse badge holders whitelisted. Signing up through SpendNode's invite link with code spendnode gets you into the app and moves you up the card waitlist. Once your turn comes, you complete KYC with a passport or national ID from any country and the virtual card is issued free.

Does Peanut have an invite code?

Yes. The Peanut invite code is spendnode. The app is invite-only, so a code is required to sign up at all. Join through SpendNode's Peanut link and the code is applied automatically - it opens the app for you and bumps you up the card waitlist.

User Reviews

Reviews are moderated and may take a moment to appear.