The Nexo Card is a hybrid Mastercard available in the EEA, UK, and Switzerland that toggles between Debit mode (spend your fiat, stablecoin, or FiatX balance while earning up to 14% APY paid daily) and Credit mode (borrow against crypto collateral at 1.9-13.9% APR depending on loyalty tier), offering 0.5-2% cashback in NEXO tokens or 0.1-0.5% in BTC for accounts with $5,000+ in digital assets.

The Only Card That Lets You Borrow and Spend From One Plastic

Our 2026 review covers every crypto card in Europe. Most crypto cards force a choice: sell your crypto to spend (debit) or lock it up and borrow against it (credit). Nexo eliminates this trade-off with a single card that toggles between both modes in the app. Tap "Credit" and your BTC becomes collateral for instant borrowing. Tap "Debit" and you spend your EUR/GBP/FiatX balance while earning up to 14% APY on idle funds, paid daily.

This dual-mode functionality is Nexo's defining advantage and the reason it attracts a specific type of user: someone who holds significant crypto and wants to spend without selling.

Important qualifier: Cashback on all purchases requires a minimum $5,000 account balance in digital assets. Below $5,000, you earn 0% cashback regardless of tier.

Nexo Card - Up to 2% cashback (requires $5,000+ balance), Apple Pay and Google Pay, instant Credit/Debit toggle, and no minimum repayments or inactivity fees.

The Ecosystem: One Card, Two Modes

Nexo Dual Card - Free Mastercard with instant in-app toggle:

-

Debit Mode: Spend your available EUR, GBP, stablecoin, or FiatX (EURx, USDx, GBPx) balance. Earn up to 14% APY on idle funds, paid daily (rate depends on loyalty tier and asset). Drag-and-drop asset priority lets you choose which assets get spent first. Works like a traditional bank card with yield.

-

Credit Mode: Nexo uses your crypto portfolio as collateral to open an instant credit line. APR ranges from 1.9% (Platinum) to 13.9% (Base), with low-cost rates requiring LTV below 20%. No selling, no taxable event.

Card availability:

- Virtual card: Instant activation with $50 minimum balance

- Physical card: Ordering temporarily paused since January 17, 2025. Requires $5,000+ balance and Gold tier minimum when available

- Card currency: EUR or GBP, chosen once at activation (cannot be changed)

- Network: Mastercard, Apple Pay and Google Pay supported

Fee Structure: Advertised vs Reality

Advertised:

- $0 annual fee

- Up to 2% rewards

- Credit and debit toggle

Actual costs you will encounter:

Reward Tiers and Loyalty Requirements

Cashback is only available on Credit mode purchases and requires $5,000+ account balance.

| Tier | NEXO Required | Cashback (NEXO) | Cashback (BTC) | Credit APR | ATM Free Limit |

|---|---|---|---|---|---|

| Base | None | 0.5% | 0.1% | 13.9% | EUR 200/mo |

| Silver | 1% of portfolio | 0.7% | 0.2% | 6.9% | EUR 400/mo |

| Gold | 5% of portfolio | 1.0% | 0.3% | 3.9% | EUR 1,000/mo |

| Platinum | 10% of portfolio | 2.0% | 0.5% | 1.9% | EUR 2,000/mo |

Low-Cost Credit rates (Gold 3.9%, Platinum 1.9%) require your Credit Wallet LTV to stay below 20%. Above 20% LTV, standard rates apply.

The NEXO token requirement: To reach the 2% Platinum tier, you need 10% of your Nexo portfolio in NEXO tokens. On a $50,000 portfolio, that means holding $5,000 in NEXO - a volatile small-cap token that could lose 50%+ in a downturn.

Foreign Exchange Fees

FX fees apply to all tiers equally - there is no tier-based reduction:

| Region | Weekday FX | Weekend FX |

|---|---|---|

| EEA / UK / Switzerland | 0.2% | 0.7% |

| Rest of World | 2.0% | 2.5% |

On top of Nexo's FX fee, the Mastercard network rate applies (typically 0.2-0.4% spread vs interbank), making the effective total markup 0.4-1.1% for EEA transactions.

Credit Mode: The Real Cost of Borrowing

Standard Credit mode APR depends on your tier. The Low-Cost Credit rates (shown in the tier table above) require maintaining LTV below 20%.

| Non-ZiC Scenario | Spend EUR 3,000/month | Annual Credit APR Cost | Cashback Earned | Net Position |

|---|---|---|---|---|

| Base (13.9%) | EUR 36,000/year | -EUR 5,004 | +EUR 180 (0.5%) | -EUR 4,824 |

| Silver (6.9%) | EUR 36,000/year | -EUR 2,484 | +EUR 252 (0.7%) | -EUR 2,232 |

| Gold (3.9%) | EUR 36,000/year | -EUR 1,404 | +EUR 360 (1.0%) | -EUR 1,044 |

| Platinum (1.9%) | EUR 36,000/year | -EUR 684 | +EUR 720 (2.0%) | +EUR 36 |

Critical insight: Credit mode barely breaks even at Platinum (1.9% APR) and loses money at every other tier. If you cannot reach Platinum, use Debit mode or choose a different card entirely. Gold at 3.9% APR costs EUR 1,044/year more than the cashback earns.

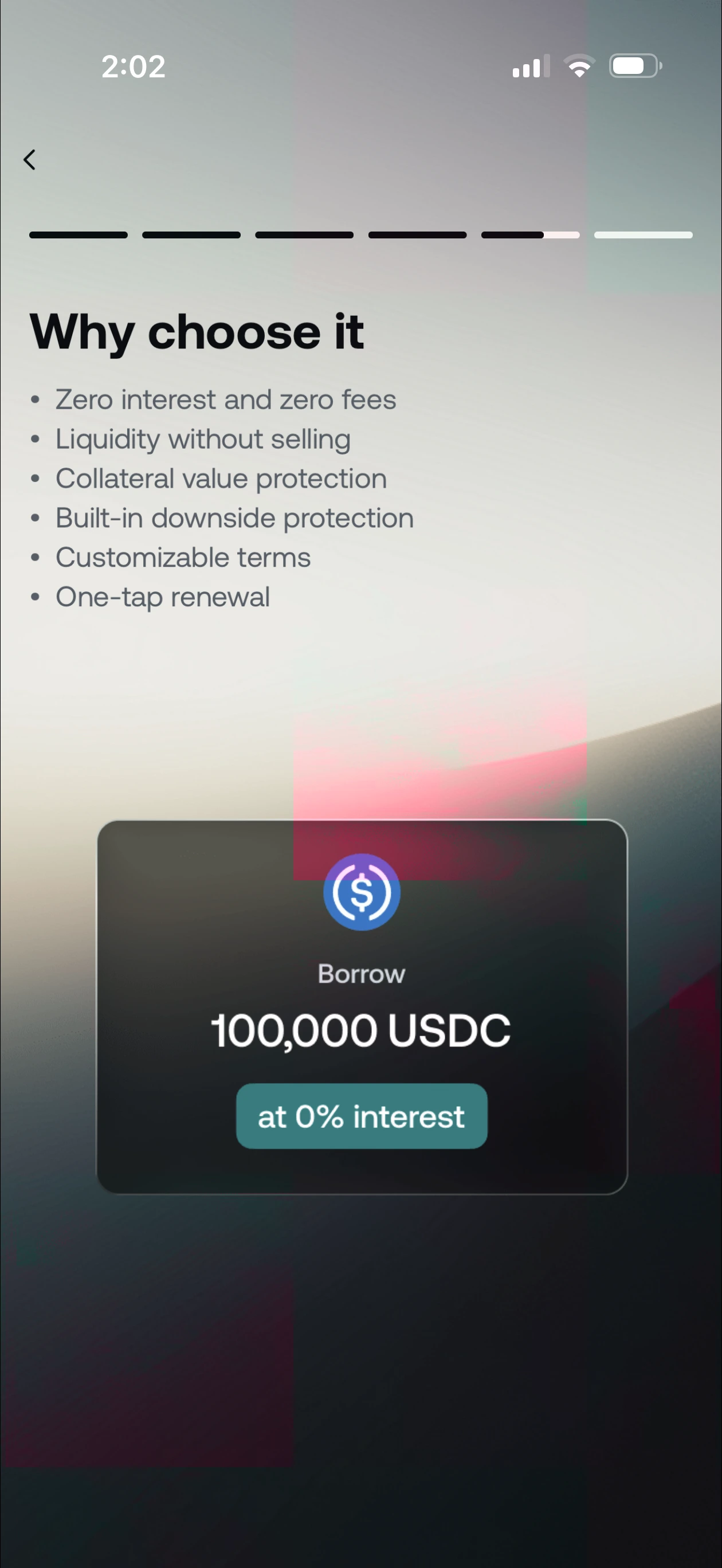

Zero-Interest Credit (ZiC): A Separate Product

Nexo also offers Zero-Interest Credit (ZiC), a structured borrowing feature confirmed by in-app screenshots. ZiC is NOT the standard card Credit mode - it is a separate product with specific terms:

- 0% interest, 0% fees on borrowed amount

- BTC and ETH collateral only

- Fixed duration (not open-ended like standard credit)

- Min-Max Repayment Price range - you set a floor and ceiling for your collateral's price at maturity

- Below minimum: Your collateral settles at the minimum price (downside protection for you)

- Above maximum: Your collateral settles at the maximum price (you give up upside above the cap)

- Repay with BTC or USDC at maturity

ZiC is essentially a collar strategy. The "cost" of 0% interest is capping your BTC/ETH upside. If BTC rallies 100% during your ZiC term, you only benefit up to your maximum repayment price.

Zero-Interest Credit (ZiC) - Borrow at 0% interest against BTC/ETH. The trade-off: a collar strategy that caps your upside. Example shows 100,000 USDC at 0% - but the min-max repayment price range is the hidden cost.

ATM Withdrawals

Free ATM allowance is amount-based (not count-based):

| Tier | Free Monthly Limit | Over-Limit Fee |

|---|---|---|

| Base | EUR 200 / GBP 180 | 2% (min EUR/GBP 1.99) |

| Silver | EUR 400 / GBP 360 | 2% (min EUR/GBP 1.99) |

| Gold | EUR 1,000 / GBP 900 | 2% (min EUR/GBP 1.99) |

| Platinum | EUR 2,000 / GBP 1,800 | 2% (min EUR/GBP 1.99) |

Loan Repayment

Credit mode purchases generate loans in xUSD. When repaying with crypto (excluding stablecoins and FIATx), a 0.26% flat fee applies. Stablecoin repayments have no fee.

Technology: The Dual-Mode Engine

Nexo's card is powered by its lending platform, which has been operational since 2018:

- Instant toggle: Switch between Credit and Debit in the Nexo app

- Credit mode settlement: When you tap, Nexo instantly opens a micro-loan against your crypto, converts to fiat, and pays the merchant. Interest accrues on the loan from the moment of purchase.

- Debit mode settlement: Standard fiat spending from your EUR/GBP/stablecoin/FiatX balance with drag-and-drop asset priority

- Supported spending assets: NEXO, BTC, ETH, USDT, USDC, EURx, USDx, GBPx

- Collateral assets (Credit mode): 40+ cryptocurrencies accepted

- Apple Pay / Google Pay: Both supported

- 3D Secure: Push notification verification for online purchases

Up to 14% APY on idle debit balances (paid daily, depending on loyalty tier and asset type) positions Nexo among the highest-yielding card accounts in the market.

Real User Scenarios

Scenario 1: Henrik (HODLer, EUR 4,000/month spend, Credit Mode)

Setup:

- Nexo Dual Card in Credit Mode

- $80,000 BTC portfolio on Nexo (50% LTV = $40,000 credit line)

- Platinum tier (10% portfolio in NEXO = $8,000 in NEXO)

- Uses credit line for all spending (no selling BTC)

Monthly math:

- Rewards: EUR 4,000 x 2% = EUR 80 in NEXO

- Credit APR cost: EUR 4,000 x 1.9% / 12 = -EUR 6.33 (assuming prompt repayment)

- FX fees (30% international, weekday): EUR 1,200 x 0.2% = -EUR 2.40

- Net monthly value: EUR 71.27 in rewards after costs

- Tax savings: Avoids capital gains on EUR 4,000/month in BTC sales

His verdict: "The tax efficiency is the real value. In Germany, selling BTC within a year triggers 26% capital gains tax. Credit mode lets me spend without selling. On EUR 48,000/year in spending, I defer thousands in potential taxes. The 2% NEXO rewards are a bonus, though I wish the FX fee were lower."

Risk: His $8,000 in NEXO tokens could lose 50%, wiping out EUR 4,000. The credit line exposes his BTC to liquidation if markets crash 40%+.

Scenario 2: Marie (Conservative, EUR 2,000/month, Debit Mode)

Setup:

- Nexo Dual Card in Debit Mode

- EUR 15,000 balance earning up to 14% APY (paid daily, rate varies by tier and asset)

- Silver tier (1% NEXO = modest holding)

- Purely domestic EEA spending

Monthly math:

- Rewards: EUR 2,000 x 0.7% = EUR 14 in NEXO

- APY on EUR 15K: varies by tier and asset (at Silver on stablecoins, significantly higher than traditional savings; up to EUR 175/month at the top Platinum rate)

- FX fees: EUR 0 (domestic only)

- Net monthly value: EUR 14 cashback + yield on idle balance = well above traditional card returns

Her verdict: "I use Debit mode exclusively. The daily yield on my idle balance earns more than my cashback rewards alone. I keep a small NEXO position for Silver tier but would not go higher - too much token risk for modest cashback improvement."

Scenario 3: Alex (Mixed Mode, GBP 3,000/month, 40% international)

Setup:

- Gold tier (5% portfolio in NEXO)

- Toggles between Credit (large purchases) and Debit (daily spending)

- GBP 5,000 idle balance for APY

Monthly math:

- Rewards: GBP 3,000 x 1.0% = GBP 30 in NEXO

- APY on GBP 5K: up to 14% APY paid daily (rate varies by tier and asset; at Gold tier, yield is a meaningful addition to card returns)

- FX fees (40% intl, mixed weekday/weekend): GBP 1,200 x 0.35% avg = -GBP 4.20

- Credit APR cost (on GBP 1,500 credit spend): GBP 1,500 x 3.9% / 12 = -GBP 4.88

- Net monthly value: GBP 30 cashback minus fees plus daily yield on idle balance

His verdict: "Credit mode for big purchases keeps my BTC untouched. Debit mode for groceries. The toggle is genuinely useful. The 0.2% FX adds up on my international spending, and Gold's 3.9% APR means credit mode is barely worth it."

Lesson: Nexo's value scales with your tier. Base and Silver are underwhelming. Gold breaks even on credit mode. Only Platinum (2% cashback, 1.9% APR) generates meaningful net value.

2026 Regulatory Status

Licensing:

- Nexo operates through multiple EU-licensed entities

- Regulated in Bulgaria (Nexo Financial LLC)

- MiCA compliance in progress

- Previously faced regulatory challenges in the US (settled with SEC in January 2023 over its Earn product)

Card issuance:

- Card network: Mastercard

- Issuer partner: Not publicly disclosed (third-party white-label)

- Custody: Hybrid (fiat in regulated accounts, crypto on Nexo platform)

- Operating since 2018, $8B+ in assets under management

What is protected:

- Fiat balances in Debit mode (held in segregated accounts per EU electronic money regulations)

- Card transactions under Mastercard's dispute resolution

What is NOT protected:

- Your crypto used as collateral in Credit mode (liquidation risk is yours)

- NEXO token value (volatile, subject to market conditions)

- Yield on idle balances (platform-managed, not insured)

- Credit mode loans (if Nexo fails during an active loan, collateral recovery is uncertain)

What Happens If Nexo Fails?

Your fiat balance (Debit Mode):

- Held in segregated accounts at regulated banks

- Protected under EU electronic money regulations

- Expected recovery: 90-100% within 30-90 days

Your crypto on Nexo:

- Risk level: Moderate-high (hybrid custodial)

- Nexo maintains insurance on custodial assets via BitGo and Ledger Vault

- In bankruptcy, crypto holders are unsecured creditors

- Nexo's lending and borrowing activities add counterparty risk beyond simple custody

Your active Credit Mode loans:

- This is the critical risk. If Nexo fails while you have an active loan:

- Your collateral is locked on their platform

- Bankruptcy proceedings could freeze collateral for months or years

- You might owe the loan amount but lose access to collateral

- Historical comparison: Celsius users with active loans faced 18+ months of uncertainty

Your NEXO tokens:

- Would likely lose 90%+ of value if the platform fails

- This compounds losses for high-tier users who hold 5-10% in NEXO

Mitigation strategy:

- Keep Credit mode borrowing to amounts you could repay if collateral is frozen

- Never hold more NEXO tokens than needed for your target tier

- Withdraw BTC rewards to self-custody regularly

- Use Debit mode for most spending; reserve Credit mode for tax-strategic large purchases

Nexo stability indicators (2026):

- Operating since 2018 (8 years)

- Insurance on custodial assets via BitGo and Ledger Vault

- $8B+ in assets under management

- SEC settlement completed (2023)

- MiCA compliance in progress

- No major security breaches

How Nexo Compares: Head-to-Head

| Feature | Nexo | Crypto.com | Plutus | Kraken |

|---|---|---|---|---|

| Credit Mode | Yes (1.9-13.9% APR) | No | No | No |

| Max Cashback | 2% NEXO / 0.5% BTC | 8% in CRO | 9% in PLU | 1% in BTC/EUR |

| Cashback Minimum | $5,000 balance | None | None | None |

| Token Requirement | 10% portfolio in NEXO | $500-$1M CRO stake | PLU stacking | None |

| APY on Idle | Up to 14% (paid daily) | 0% | 0% | 0% |

| FX Fee (EEA) | 0.2% weekday / 0.7% weekend | 0% | 0% (paid tier) / 2.5% (free) | 0% |

| Regions | EEA, UK, CH | Global (95+) | UK, EEA | EEA, UK |

| Best For | Tax-efficient HODLers | Lifestyle + global | UK/EU perk maximizers | Zero-fee simplicity |

After reviewing the alternatives:

Nexo wins on:

- Only card with instant Credit/Debit toggle (unique in the market)

- Tax efficiency in high-tax jurisdictions (Germany, France, UK) - borrowing is not a taxable event

- Up to 14% APY on idle debit balances, paid daily (highest yield-on-card in the market)

- No staking lockup (hold NEXO, do not stake it - sell anytime, though tier drops)

- ZiC structured borrowing at 0% for BTC/ETH holders (separate feature)

Nexo loses on:

- Lower reward ceiling (2% max vs 4-9% for competitors)

- Requires $5,000 minimum balance for ANY cashback

- FX fees on every international transaction (0.2-2.5% vs 0% for Crypto.com and Kraken)

- Requires holding volatile NEXO tokens for best rates

- EEA/UK/CH only (no US, no APAC, no LATAM)

- Complex product (Credit mode adds liquidation risk, APR varies by tier)

- Physical card ordering paused since Jan 2025

Who Should Use Nexo Card in 2026?

Ideal user profile:

- EEA/UK resident with significant crypto holdings ($20K+)

- Account balance above $5,000 (otherwise zero cashback)

- Wants to spend without selling crypto (tax efficiency)

- Comfortable holding 5-10% portfolio in NEXO tokens

- Values the Credit/Debit toggle for flexible spending

- Lives in a high capital gains tax jurisdiction

Who should avoid:

- Users who want maximum cashback (2% ceiling is modest - use Plutus 9% or Crypto.com 8%)

- Users with under $5,000 on Nexo (zero cashback - use Kraken for 1% with no minimum)

- Users who do not want NEXO token exposure (use Kraken for 0% fees and 1% cashback with zero token requirement)

- Self-custody advocates (Nexo is hybrid custodial - use Gnosis Pay or Ready)

- US/APAC/LATAM residents (not available - EEA, UK, and Switzerland only)

- Users who need zero FX fees (0.2%+ on every international purchase - use Crypto.com or Kraken for 0% FX)

Key takeaway: Our side-by-side comparison confirms that Nexo is the most sophisticated crypto card for tax-conscious European investors with $20K+ in crypto. The Credit mode toggle is genuinely unique - no other card lets you instantly switch between spending your balance and borrowing against your portfolio. For a Platinum-tier user who spends EUR 4,000/month, the tax deferral alone can save thousands per year in high-tax jurisdictions. The trade-off: $5,000 minimum for any cashback, 0.2%+ FX fees, holding NEXO tokens for tier benefits, and the complexity of managing a lending-backed card.

Fees and ROI framework

$0 annual fee. FX: 0.2% weekday / 0.7% weekend (EEA/UK/CH), 2% / 2.5% (ROW). ATM: free up to EUR 200-2,000/month by tier, then 2%. Credit APR: 1.9% (Platinum) to 13.9% (Base). Cashback requires $5,000 minimum balance. Rewards range from 0.5% NEXO (Base) to 2% NEXO (Platinum, requires 10% portfolio in NEXO). At Platinum with EUR 3,000/month domestic spend in Credit mode: EUR 720/year cashback minus EUR 684 APR cost = EUR 36 net. Adding up to 14% APY (paid daily, tier-dependent) on idle balance significantly boosts total returns. Virtual card: $50 minimum to activate. Physical card: $5,000+ balance and Gold tier required (ordering paused since Jan 2025). The true cost is NEXO token exposure - a 30% NEXO price drop on a $5,000 holding wipes out more than a year of net card value.

Competitor comparison

- vs Crypto.com: Crypto.com offers 2-8% CRO with staking ($500-$1M). Nexo offers 0.5-2% NEXO with portfolio allocation (no lockup). Crypto.com wins on max rewards, lifestyle perks (lounge, rebates), global availability, and 0% FX. Nexo wins on credit mode (tax efficiency), up to 14% APY on idle balances (paid daily), and no staking lockup.

- vs Plutus: Plutus offers 3-9% PLU with subscription + stacking (UK/EEA). Both reward in native tokens. Plutus wins on max rewards and subscription rebates. Nexo wins on credit mode, up to 14% APY on idle balances, and no subscription fee.

- vs Kraken: Kraken offers 1% in BTC/EUR with zero fees, zero token requirement, no minimum balance. Kraken wins on simplicity, 0% FX, and accessibility. Nexo wins on credit mode and higher max cashback (2% vs 1%).

Availability and compliance notes

EEA (30 countries) and UK only. Not available in US, APAC, or LATAM. Standard KYC required. Loyalty tiers based on NEXO token portfolio percentage (1-10%). Virtual card requires $50 minimum. Physical card ordering paused since January 2025 (requires $5,000 + Gold tier when available). Card currency EUR or GBP, chosen once at activation. Mastercard network. Apple Pay and Google Pay supported. Insurance on custodial assets via BitGo and Ledger Vault. MiCA compliance in progress.

Sources and Verification

Frequently Asked Questions

What is Zero-Interest Credit (ZiC)?

ZiC is a separate structured borrowing feature where you borrow against BTC or ETH at 0% interest for a fixed duration. You set a min-max repayment price range: if the collateral price falls below the minimum, it settles at the floor (downside protection). If it rises above the maximum, it settles at the cap (you give up upside). ZiC is NOT the standard card Credit Mode APR, which is 1.9% (Platinum) to 13.9% (Base).

Is the Nexo Card a credit card or debit card?

Both. The Nexo Dual Card is a hybrid Mastercard that toggles between Debit mode (spend your fiat/stablecoin balance) and Credit mode (borrow against your crypto portfolio). In Credit mode, the APR depends on your loyalty tier: 1.9% for Platinum, 3.9% for Gold, up to 13.9% for Base. No taxable disposal event occurs in Credit mode since you are borrowing, not selling.

App Store (1.6K ratings)

Source: Apple App Store - Updated Invalid Date