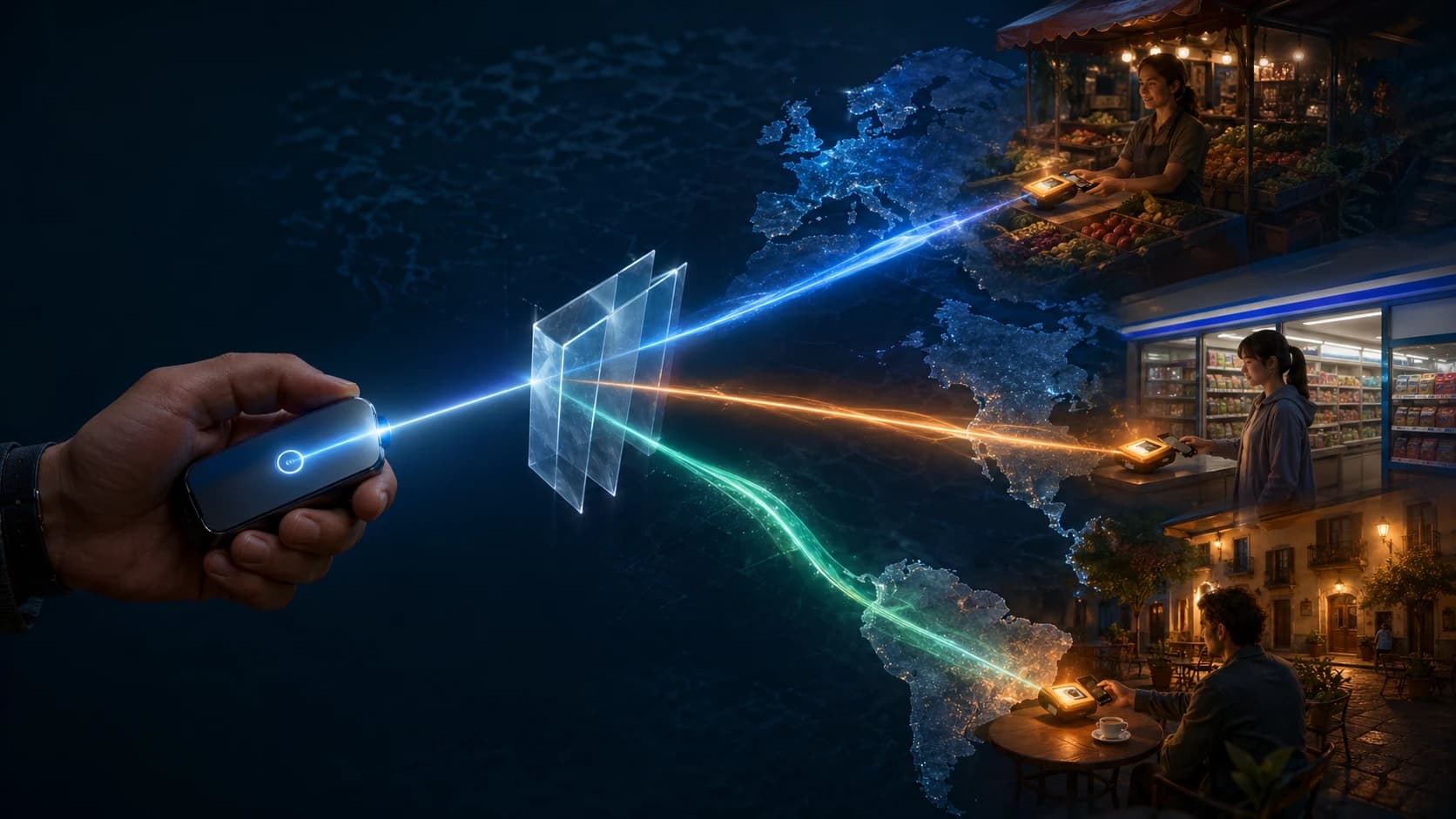

Visa is wiring self-custodied crypto into its payment network through a new partnership with WeFi, the wallet startup led by former Tether CEO Reeve Collins. The deal, announced by Cointelegraph on April 28, 2026, will let users spend tokens directly from their own wallets at any Visa-accepting merchant, starting in select markets across Europe, Asia, and Latin America.

The pitch is simple: the user keeps the keys, the merchant gets paid in fiat, and Visa handles the rails in between.

Balances stay in the user's wallet until authorization

WeFi is a non-custodial wallet built around stablecoin spending. In the Visa integration, balances stay in the user's own wallet until the moment of authorization. When a card is tapped or charged online, WeFi signs the transaction on chain, swaps the required amount into fiat at execution, and Visa settles the merchant in the local currency.

That on-the-fly conversion model is what separates this from the older crypto-card playbook, where users typically pre-fund a custodial account, get hit with a deposit fee, and only then receive a card. Here, balances never leave the user's self-custody setup until the swipe itself.

Reeve Collins, who co-founded Tether more than a decade ago, has framed WeFi as an attempt to make stablecoins behave like a normal bank account without the bank. The Visa tie-up is the first time that thesis has been bolted to a global payment network at scale.

Each launch region has a different last-mile problem

Visa and WeFi are starting in Europe, Asia, and Latin America. The choice is not random. Each region has a population that already uses stablecoins for either remittances, savings, or workaround payments, but lacks easy on-ramps to merchant spending.

In Latin America, USDT and USDC have become de facto savings instruments in Argentina, Venezuela, and parts of Colombia, where local currency volatility has pushed retail users toward dollar-denominated tokens. The friction has always been the last mile: turning that stablecoin balance into a coffee, a grocery bill, or a utility payment without bouncing through a centralized exchange.

In Asia, the Philippines and parts of Southeast Asia rely on stablecoin transfers for inbound remittances. A Visa-WeFi card converts that flow into directly spendable funds.

In Europe, the angle is different. The market is mature, MiCA is now in force, and self-custody users are looking for compliant ways to spend on-chain balances without surrendering custody to an exchange.

The user keeps the keys through every authorization

Most existing crypto cards require some form of trust delegation. Either the user moves funds into the issuer's custody, or the issuer holds an internal balance that maps to user accounts. If the issuer has a counterparty event, the user's balance is at risk. The Wirecard collapse and the FTX bankruptcy are the cautionary references most often cited.

A self-custody model removes that exposure. WeFi acts as a signing client, not a custodian. If WeFi disappears tomorrow, the user's wallet still holds the keys.

The trade-off is operational complexity. Network fees, swap slippage, and authorization timing all have to fit inside the few seconds Visa allows for an authorization response. Existing self-custody card products, including Gnosis Pay and MetaMask's metal card, have already shown the model works at small scale. The question with WeFi is whether Visa's own infrastructure is willing to underwrite it across multiple jurisdictions.

Visa is keeping crypto flow on its rails rather than ceding it

Visa has been quietly running stablecoin settlement pilots since 2023, when it began letting select issuers settle USDC directly with the network. The WeFi deal pushes that further by exposing self-custody flows to ordinary cardholders rather than back-office settlement partners.

For Visa, the strategic logic is defensive as much as offensive. Stablecoin payment flows hit $1 trillion in monthly transfers earlier this month, and a growing share of that volume is bypassing card rails entirely through direct wallet-to-wallet transfers. Building a path that lets crypto holders stay on Visa rails, rather than route around them, is a way to keep the network in the loop as on-chain payments scale.

The launch details still missing from the announcement

The announcement, sourced from Cointelegraph's verified account, did not name specific launch countries inside each region, did not disclose fee structures, and did not specify which tokens or chains WeFi will support at launch. It is also not yet clear whether WeFi's card will be issued directly under its own brand or through a regional banking partner, which is the more common arrangement for a Visa-network program.

Until those details land, the most useful read on the deal is structural: a top-tier payment network has now formally endorsed a self-custody model for retail spending. That is a meaningfully different posture from the custodial-only stance that defined card programs through 2024.

Overview

Visa's partnership with WeFi brings non-custodial crypto spending onto one of the world's largest payment networks. Users keep their keys, WeFi signs transactions at the point of sale, and Visa settles merchants in fiat. The launch covers parts of Europe, Asia, and Latin America. Specific countries, fees, and supported tokens have not yet been disclosed.