METAL CARD

Verified

SELF CUSTODY SPEND

Verified

CASHBACK

Verified

Our Official Verdict

Ultimate Web3 Luxury: 6% Cashback + Zero ATM Fees

The Tria Premium Card is the best self-custodial card on the market in 2026. The combination of 6%% rewards and zero global ATM fees makes the $250 fee negligible for frequent travelers. It bridges the gap between luxury banking and DeFi sovereignty perfectly.

Fees & Charges

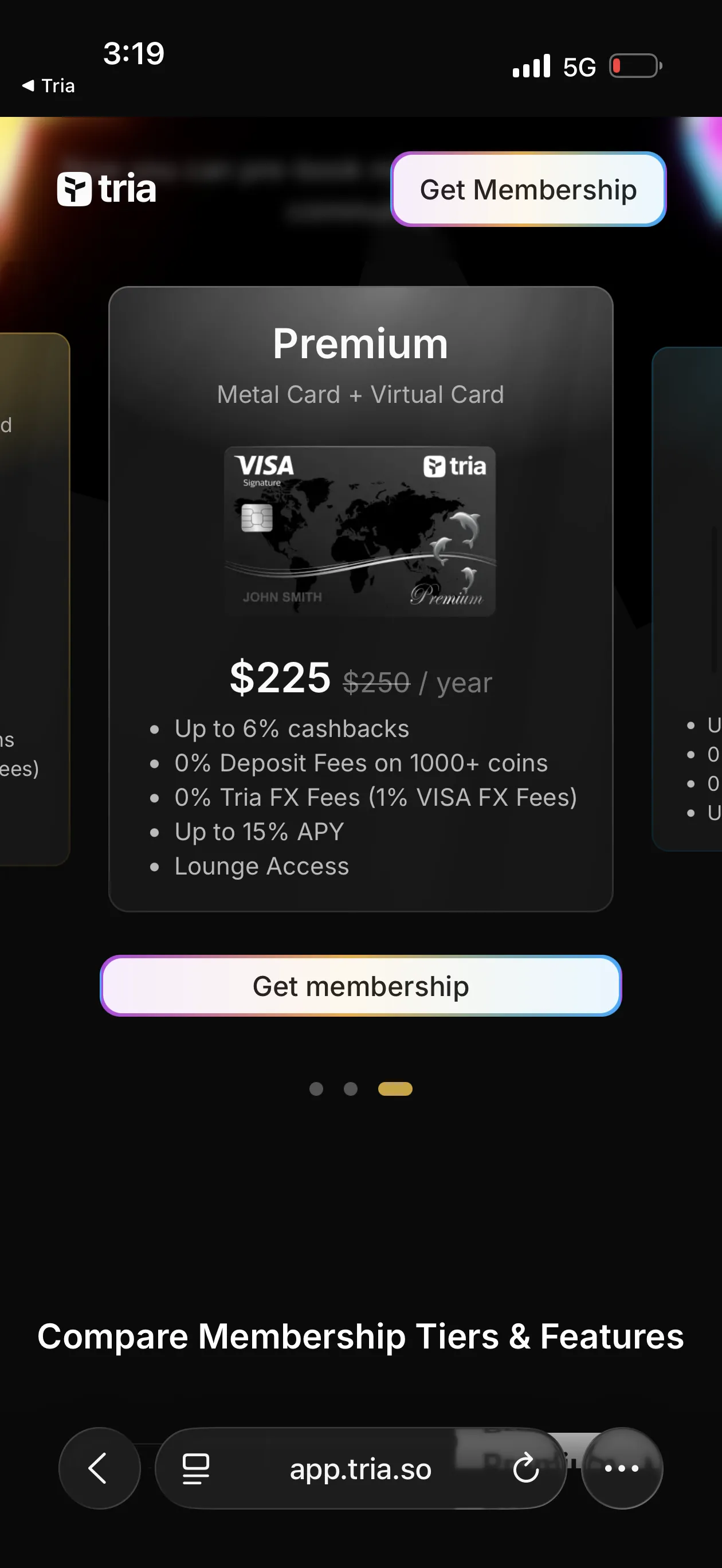

Annual Fee

$250

FX Fee

0%

ATM Fee

0%

Requirements

Supported Regions

EEA, UK, US, GLOBAL

Spendable Assets

ETH, USDC, USDT

Tria Premium Card Review

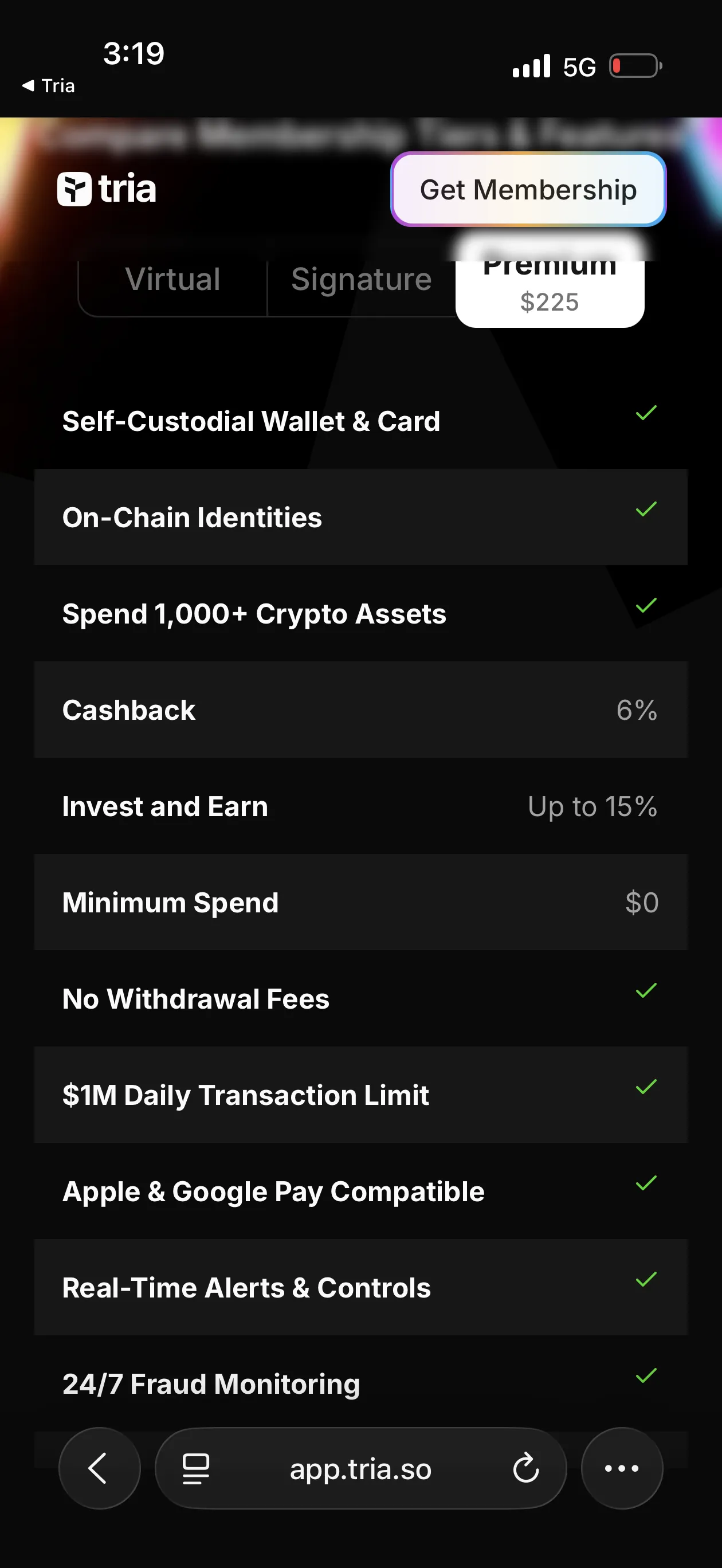

The Tria Premium Card is a self-custodial metal Visa debit card powered by account abstraction, offering 6% cashback on all purchases, 0% FX fee, 0% ATM fee, $250/year annual fee, purchase protection, up to 15% APY on wallet balances, $100,000 monthly spending limit, 1,000+ supported crypto assets on Optimism, Arbitrum, and Solana, and Apple Pay and Google Pay. Available in EEA, UK, US, and global markets.

The Highest Cashback Rate on Any Self-Custodial Card

We reviewed every premium-tier crypto card in 2026, and the Tria Premium Card delivers the highest cashback rate among self-custodial options: 6% on all purchases while keeping your funds in a self-custodial smart account. No other self-custodial card matches this rate. The closest is ether.fi Pinnacle at 3% - half the rate.

The only card that matches 6% cashback anywhere is KAST Pengu - but KAST is custodial. If self-custody matters to you, Premium stands alone at the top.

At $250/year with 0% FX fees, 0% ATM fees, and a $100,000 monthly spending limit, the card targets high-volume spenders who want DeFi-grade self-custody without sacrificing rewards. The break-even at $347/month is low for what you get: every dollar above that threshold generates 6% net profit.

Tria Premium Card - The highest cashback rate on any self-custodial card. 6% on all purchases, 0% FX, 0% ATM, metal construction, and $100K monthly limit.

$250/yr | 6% cashback | 0% FX | 0% ATM | Metal

Card Specs

Physical and Virtual Cards

- Virtual card: Included with Premium tier

- Physical card: Metal construction

- Wallet integration: Apple Pay and Google Pay

Payment Network

- Network: Visa

- Contactless: Yes (NFC)

- Card type: Debit (self-custodial via account abstraction)

- Custody: Self-custodial (AA smart account on OP, Arbitrum, Solana)

Features

- Cashback: 6% base (up to 8% with TRIA staking bonus)

- FX fee: 0% on all currencies

- ATM fee: 0% (up to $750/day)

- Deposit fee: 0% on 1,000+ crypto assets

- APY: Up to 15% on wallet balances

- Points multiplier: 3x

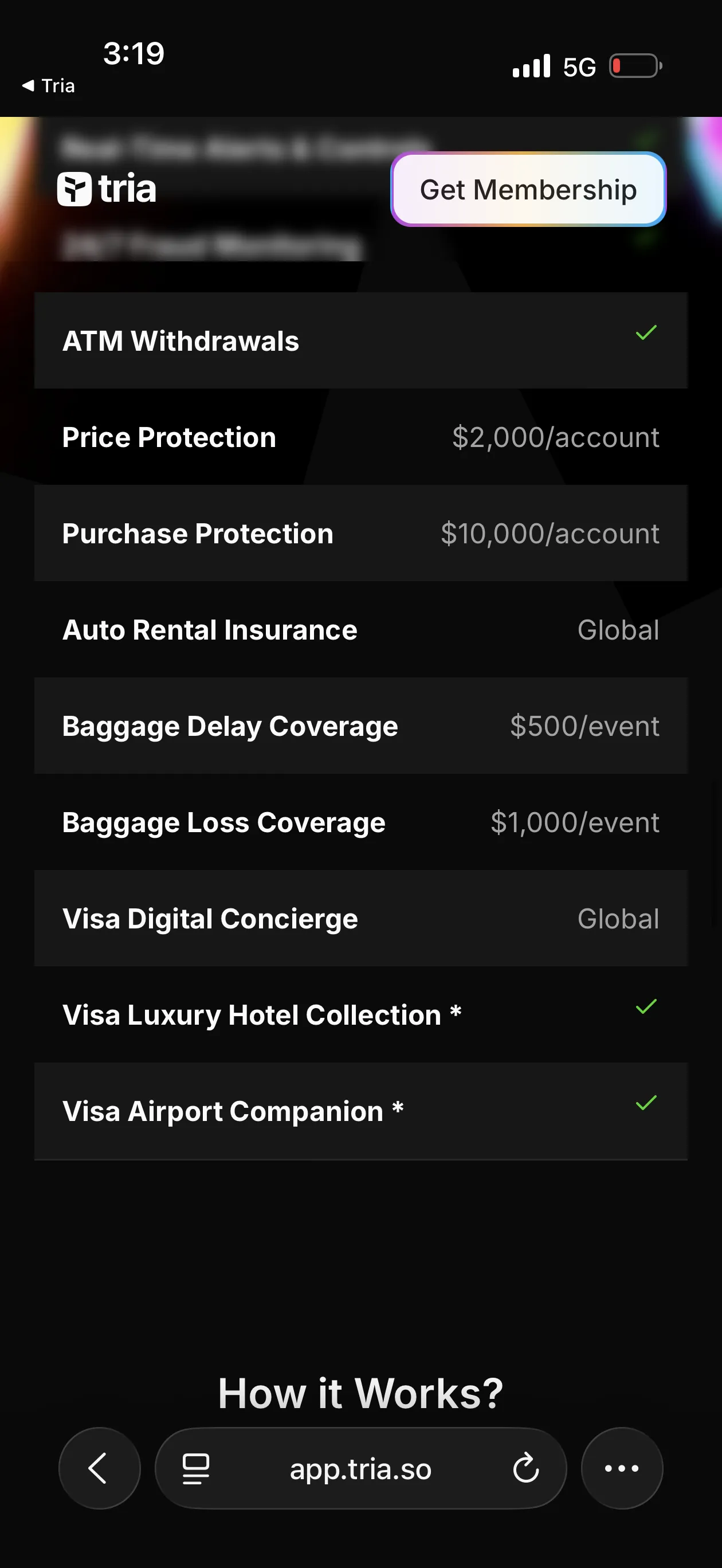

- Price Protection: $2,000

- Purchase Protection: $10,000

- Visa Luxury Hotel Benefits: Included

- Monthly limit: $100,000

- Supported chains: Optimism, Arbitrum, Solana

Premium Features - 6% cashback (up to 8% with staking), 3x points multiplier, up to 15% APY, 0% ATM up to $750/day, and $100,000 monthly limit.

Fee Analysis and Break-Even

| Fee | Amount |

|---|---|

| Annual fee | $250 (paid in crypto) |

| FX fee | 0% |

| ATM fee | 0% |

| Deposit fee | 0% |

| Cashback (base) | 6% |

| Cashback (with staking) | Up to 8% |

| APY on balances | Up to 15% |

| Monthly limit | $100,000 |

| Price protection | $2,000 |

| Purchase protection | $10,000 |

| Points multiplier | 3x |

| Visa Luxury Hotel | Included |

Net Returns at Different Spending Levels

| Monthly Spend | Annual Cashback (6%) | Annual Fee | Net Return |

|---|---|---|---|

| $347 | $250 | -$250 | $0 (break-even) |

| $500 | $360 | -$250 | +$110/yr |

| $1,000 | $720 | -$250 | +$470/yr |

| $2,000 | $1,440 | -$250 | +$1,190/yr |

| $5,000 | $3,600 | -$250 | +$3,350/yr |

| $10,000 | $7,200 | -$250 | +$6,950/yr |

Break-even at just $347/month. For a 6% metal card with self-custody, this is an extraordinarily low threshold. At $5,000/month - realistic for a business spender or high-income professional - the net $3,350/year far exceeds what most premium cards deliver at 10x the cost.

The 0% ATM Advantage

Premium is the only Tria tier with free ATM withdrawals. Compare ATM costs across $500/month in withdrawals:

| Card | ATM Fee | Annual ATM Cost on $500/mo |

|---|---|---|

| Tria Premium | 0% | $0 |

| Tria Signature | 2% | $120 |

| Crypto.com Jade | 0% (up to $400/mo) | $24 (overage) |

| Ready Metal | 0% (up to $800/mo) | $0 |

| Traditional bank | $3-5 flat | $180-$300 |

For heavy ATM users, Premium's zero fee saves $120/year over Signature alone - nearly half the price difference between tiers.

Premium vs Signature: When to Upgrade

| Feature | Signature | Premium |

|---|---|---|

| Annual fee | $109 | $250 |

| Cashback | 4.5% | 6% |

| Extra cashback | - | +1.5% |

| ATM fee | 2% | 0% |

| Monthly limit | $50K | $100K |

| Visa travel perks | Full suite | Full suite (identical) |

| Purchase protection | Yes ($10,000) | Yes |

The extra 1.5% cashback costs $141/year ($250 minus $109). At $783/month, the additional 1.5% generates $141 in extra cashback - that is the crossover point. Above $783/month, Premium is strictly better on cashback math.

Note on Visa perks: Both Signature and Premium include identical Visa Signature perks: auto rental CDW (global), baggage delay coverage ($500/event), baggage loss coverage ($1,000/event), Visa Luxury Hotel Collection, Visa Airport Companion, Visa Digital Concierge, purchase protection ($10,000), and price protection ($2,000). Visa perks are not a factor in the upgrade decision - it comes down purely to the cashback math and the 0% ATM benefit on Premium.

Visa Perks (Identical to Signature) - Auto Rental CDW, Baggage Delay ($500), Baggage Loss ($1,000), Visa Digital Concierge, Luxury Hotel Collection, and Airport Companion. The upgrade decision is purely about cashback math and 0% ATM.

Tria Premium vs Every Premium Competitor

| Feature | Tria Premium | KAST Pengu | Crypto.com Obsidian | ether.fi Pinnacle |

|---|---|---|---|---|

| Annual cost | $250 | $0 | $0 ($400K CRO) | $0 (50K pts) |

| Cashback | 6% | 6% | 5% | 3% |

| FX fee | 0% | TBD | 0% | 1% |

| ATM | 0% | N/A | 0% ($400+/mo) | N/A |

| Card material | Metal | Virtual | Metal | Metal |

| Custody | Self-Custodial | Custodial | Custodial | Self-custodial |

| Monthly limit | $100,000 | TBD | Varies | $200K |

| Yield | Up to 15% APY | No | CRO staking | ETH staking |

| Supported assets | 1,000+ | USDC/USDT | 20+ | ETH/USDC |

KAST Pengu matches on 6% cashback at $0 annual fee (but 0.5-1.75% FX on non-USD spending reduces the net rate). KAST is custodial and virtual-only. If self-custody, metal card, 0% FX, and yield matter to you, Tria Premium is the upgrade. If you prioritize $0 annual fee and trust custodial, KAST delivers the same gross rate at $250/year less in subscription - though Tria's 0% FX advantage narrows the net gap for non-USD spenders.

Crypto.com Obsidian requires $400,000 locked in CRO for 5% cashback - one percentage point less than Tria at $250/year. The capital efficiency is staggering: $250 vs $400,000 for a higher rate. Crypto.com wins on ecosystem maturity (7+ years), brand recognition, and the value of the CRO ecosystem perks. But unless you have $400K to lock away, this comparison is theoretical.

ether.fi Pinnacle offers 3% with self-custody on an established platform (4.74 stars, 73K reviews). Half the cashback rate of Tria Premium but on a far more proven platform. For users who prioritize track record over maximum returns, ether.fi remains the safer bet.

Sustainability: Can 6% Last?

6% cashback on all purchases is an aggressive rate. After reviewing the economics honestly:

- Traditional Visa interchange fees are 1.5-3% per transaction

- A 6% cashback rate means the issuer pays out 2-4.5x what it earns per swipe from interchange alone

- The deficit is likely subsidized by: token economics (TRIA token value capture), DeFi yield on idle balances, venture capital runway, and growth-stage user acquisition spend

- This pattern is common in early-stage crypto card programs: ether.fi, KAST, and others launched with rates that may evolve

What to expect: Rates above interchange are inherently time-limited unless offset by other revenue. Tria may adjust rates as the platform scales, introduce caps, or shift the economics toward the staking badge system. KAST's identical 6% is similarly unsustainable long-term without alternative revenue streams.

The smart approach: Maximize the 6% while it is available. Do not build your financial plan around it being permanent. Even if the rate drops to 3-4%, the self-custody, yield, and 1,000+ asset support remain valuable. At 3%, Premium still generates $470/year net on $2,000/month spending.

Yield on Idle Balances

Premium includes access to Tria's yield feature - up to 15% APY on idle wallet balances through integrated DeFi protocols. Your USDC and other assets can earn yield while remaining available for card spending.

Realized yield fluctuates with DeFi market conditions and typically runs below the 15% ceiling. Using a conservative 8-10% assumption for Premium-tier balances:

| Idle Balance | Est. Annual Yield (10%) | Cashback on $3K/mo | Fee | Total Net |

|---|---|---|---|---|

| $2,000 | $200 | $2,160 | -$250 | +$2,110/yr |

| $5,000 | $500 | $2,160 | -$250 | +$2,410/yr |

| $10,000 | $1,000 | $2,160 | -$250 | +$2,910/yr |

| $20,000 | $2,000 | $2,160 | -$250 | +$3,910/yr |

At higher balances, the yield starts to rival the cashback itself. A $20,000 idle balance earning 10% adds $2,000/year - nearly matching the $2,160 in cashback from $3,000/month spending. The combination makes Premium progressively more valuable as your wallet balance grows.

What Happens If Tria Goes Down?

Your $250 annual fee: Non-refundable. This is your primary guaranteed financial exposure, and it is the highest among Tria tiers.

Your wallet funds: Account abstraction smart account persists on-chain. Your assets are recoverable through the blockchain, though you should verify independent access to your smart account without relying on Tria's app. The exact recovery process depends on Tria's AA implementation and whether you have exported recovery credentials.

Your yield deposits: At risk if the underlying DeFi protocols fail or Tria's yield infrastructure goes offline. With Premium's higher limits, users tend to hold larger balances - making this the most impactful risk vector. Keep yield deposits to amounts you can afford to have temporarily locked.

Your cashback: Any pending cashback not yet distributed may be lost. Tria does not guarantee pending rewards in a shutdown scenario. Withdraw promptly when credited.

Your purchase protection claims: May not be honored post-shutdown depending on whether the coverage is through Visa or through Tria directly. Clarify the terms before relying on this benefit for high-value purchases.

Mitigation: Despite the $100K/month limit, do not keep $100K loaded. Load what you plan to spend in the next 30 days. Hold long-term savings in a hardware wallet or fully independent self-custodial solution. The Premium tier enables high spending but does not require high balance holding.

Real User Scenarios

Scenario 1: Daniel (Zurich Fintech Founder, CHF 8,000/month spending)

Setup:

- Tria Premium Card (EEA, $250/year)

- 60% CHF domestic, 40% international (conferences, team dinners, travel)

- Uses 0% ATM for cash withdrawals in emerging markets

- Holds $15,000 idle balance for business liquidity

- $100K/mo limit handles large vendor payments

| Item | Amount |

|---|---|

| Domestic cashback (6% on CHF 4,800/mo) | CHF 3,456/yr |

| International cashback (6% on CHF 3,200/mo, 0% FX) | CHF 2,304/yr |

| ATM savings vs 2% Signature (CHF 500/mo withdrawals) | CHF 120/yr |

| Yield on CHF 15,000 balance (est. 10%) | CHF 1,500/yr |

| Annual fee | -CHF 250 |

| Net annual return | +CHF 7,130 |

His verdict: "At CHF 8,000/month, Premium nets over CHF 7,000/year. Signature would net approximately CHF 3,600 on the same spending - half as much. The $100K monthly limit matters because I occasionally pay quarterly invoices through the card. ether.fi Pinnacle caps at $200K but only gives 3% - on my volume, Premium earns CHF 2,880 more per year in cashback alone. The yield on my CHF 15,000 business float adds CHF 1,500 that no competitor offers at this tier."

Scenario 2: Yuki (Tokyo Remote Developer, $4,000/month spending)

Setup:

- Tria Premium Card (Global, $250/year)

- 50% JPY domestic, 50% international (subscriptions, online services, travel)

- Holds diverse portfolio: ETH, USDC, ARB, OP, SOL, and 20+ DeFi tokens

- Uses 0% ATM when traveling across APAC

- Testing Premium for 6 months before committing long-term

| Item | Amount |

|---|---|

| Monthly spend | $4,000 |

| Annual cashback (6%) | $2,880 |

| Yield on $8,000 balance (est. 10%) | $800 |

| Annual fee | -$250 |

| Net annual return | +$3,430 |

| Signature would net (4.5%) | +$2,401 |

| Premium advantage over Signature | +$1,029/yr more |

Her verdict: "The 1,000+ asset support is essential for me. I hold 25 different tokens across Optimism and Solana. With ether.fi, I would need to swap everything to ETH or USDC first - losing 0.3-1% on each swap. With Tria, I spend directly from whatever I hold. The 6% rate on $4,000/month generates $2,880/year versus $2,160 at Signature's 4.5%. The $141 difference in annual fees pays for itself within 3 months of spending."

Scenario 3: Marcus (Berlin DeFi Strategist, $6,000/month spending)

Setup:

- Tria Premium Card (EEA, $250/year)

- 80% EUR domestic, 20% international

- Previously on Crypto.com Icy White ($50K CRO stake, 5%)

- Freed up $50K by switching to Tria ($250/year vs $50K locked)

- Runs yield strategies on freed capital

| Item | Amount |

|---|---|

| Monthly spend | $6,000 |

| Annual cashback (6%) | $4,320 |

| vs Crypto.com Icy (5%) | $3,600 |

| Extra cashback from 6% vs 5% | +$720/yr |

| Capital freed (no $50K CRO stake) | $50,000 |

| Yield on freed capital (est. 10%) | $5,000/yr |

| Tria yield on $5K balance (est. 10%) | $500 |

| Annual fee | -$250 |

| Net annual return | +$4,570 |

| Total advantage vs CdC Icy (incl. freed capital) | +$6,690/yr |

His verdict: "The math is clear. Crypto.com Icy required $50,000 locked in CRO - a volatile asset that dropped 90% from its peak. Tria costs $250/year with no capital lockup. I freed $50,000 and now earn yield on it separately. Even ignoring the freed capital, Tria's 6% beats Icy's 5% by $720/year. Crypto.com has a 7-year track record which I respect, but self-custody eliminates my exchange risk entirely. The only thing I lost was the Icy airport lounge access."

The Full Tier Comparison

| Feature | Virtual | Signature | Premium |

|---|---|---|---|

| Annual fee | $20 | $109 | $250 |

| Cashback (base) | 1.5% | 4.5% | 6% |

| Cashback (with staking) | Up to 3.5% | Up to 6.5% | Up to 8% |

| FX fee | 0% | 0% | 0% |

| ATM | N/A | 2% | 0% ($750/day) |

| Points multiplier | 1x | - | 3x |

| Monthly limit | $10K | $50K | $100K |

| Card type | Virtual | Metal | Metal |

| Auto rental CDW | Global | Global | Global |

| Baggage coverage | No | $500 delay / $1,000 loss | $500 delay / $1,000 loss |

| Price protection | $2,000 | $2,000 | $2,000 |

| Purchase protection | $10,000 | $10,000 | $10,000 |

| Visa Luxury Hotel | No | Yes | Yes |

| Visa Airport Companion | No | Yes | Yes |

| Visa Digital Concierge | Global | Global | Global |

Recommended progression: Start with Virtual ($20/year) to validate the platform. Upgrade to Signature ($109/yr) at $247/month spending for 4.5% cashback and the full Visa Signature perk suite (baggage coverage, luxury hotel, airport companion). Upgrade to Premium ($250/yr) at $783/month over Signature for 6% cashback and 0% ATM - both tiers include identical Visa perks.

Limits and Restrictions

| Limit | Amount |

|---|---|

| Annual fee | $250 |

| Monthly spending | $100,000 |

| ATM fee | 0% |

| FX fee | 0% |

| Cashback | 6% |

| APY | Up to 15% (variable) |

| Supported assets | 1,000+ |

| Supported chains | Optimism, Arbitrum, Solana |

| Card type | Virtual + Physical metal |

| Mobile wallets | Apple Pay, Google Pay |

| KYC | Required |

| Regions | EEA, UK, US, Global |

The Verdict

This review makes one thing clear: the Tria Premium Card is the most aggressive self-custodial crypto card in the market. 6% cashback, 0% FX, 0% ATM, metal card, $100K/mo limit, 1,000+ supported assets, purchase protection, and up to 15% APY - all for $250/year with your funds staying under your control.

The break-even at $347/month is low. At $2,000+/month, the returns are significant: $1,190/year net before yield. At $5,000/month, that grows to $3,350. Add yield on idle balances and the total climbs further.

As reviewed in our sustainability section above, the 6% rate may not be permanent - no above-interchange cashback rate is. But even at reduced rates, the self-custody, yield, multi-chain support, and 1,000+ asset coverage make Premium a compelling card for high-volume DeFi-native spenders.

For pure cost efficiency without annual fees, KAST Pengu matches at 6% but is custodial. For free self-custodial cashback, ether.fi Core delivers 3% with a proven platform. For the same Visa Signature perks at a lower price, the Signature tier at $109/year includes identical Visa benefits at 4.5% cashback. Choose based on what matters most: maximum rate + 0% ATM (Premium), zero cost (KAST/ether.fi), or lower annual commitment (Signature).

Sources and Verification

All card specs, fees, and limits verified from:

- Tria App

- In-app screenshots verified March 2026

FAQ

How do you choose Tria Premium Card crypto cards?

We compare verified issuer sources, fees, and eligibility. Availability can change, so confirm with the issuer before applying.

Do all cards in this list offer the same benefits?

No. Each issuer defines its own program terms. Review the sources on each card profile.

Are these rankings or recommendations?

No. Lists are filtered views of cards in our database and do not imply rankings.

This is a debit card. Some merchants with pre-authorization holds (hotels, car rentals) may temporarily hold funds beyond the transaction amount.

This card requires token staking to unlock higher reward tiers. If the staked token's price drops, your losses may exceed the cashback earned. Consider the break-even math before locking funds.

You retain custody of your funds until the moment of spending. Your balance is not exposed to provider insolvency risk.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?