The Plutus Card is a Visa debit card (not a credit card) that combines traditional debit spending with a non-custodial crypto rewards program, allowing users to earn up to 9% cashback in PLU tokens while maintaining full control of their assets through external wallet integration.

What Makes Plutus Different: The Non-Custodial Advantage

Plutus Visa Card - Non-custodial rewards model. Connect your own wallet, earn up to 9% cashback in PLU tokens. No funds ever sent to the platform.

In our exchange card ranking, a market dominated by custodial exchanges like Crypto.com and Binance, Plutus stands alone with a radical trust model: you never send your PLU tokens to the platform. Instead, you connect an external wallet (MetaMask, Ledger, or any Ethereum/Polygon wallet) to the Plutus app, which reads your balance on-chain to determine your reward tier.

Why this matters in 2026: After FTX erased $8B in customer funds and Celsius froze withdrawals for 18+ months, the "not your keys, not your coins" principle has moved from Bitcoin maximalist ideology to mainstream safety protocol. Plutus lets you earn elite-tier cashback (up to 9%) without exposure to exchange bankruptcy risk.

The trade-off: Higher complexity. You're responsible for seed phrase management, gas fees for moving PLU between wallets, and understanding how the "stacking" system calculates your tier. This isn't a beginner card—it's for crypto-native users who already manage self-custody wallets.

How Plutus Works: Subscription + Stacking + Perks

The Three-Tier Revenue Model

Unlike traditional cards that make money on transaction fees and interchange, Plutus operates on a subscription model that creates aligned incentives:

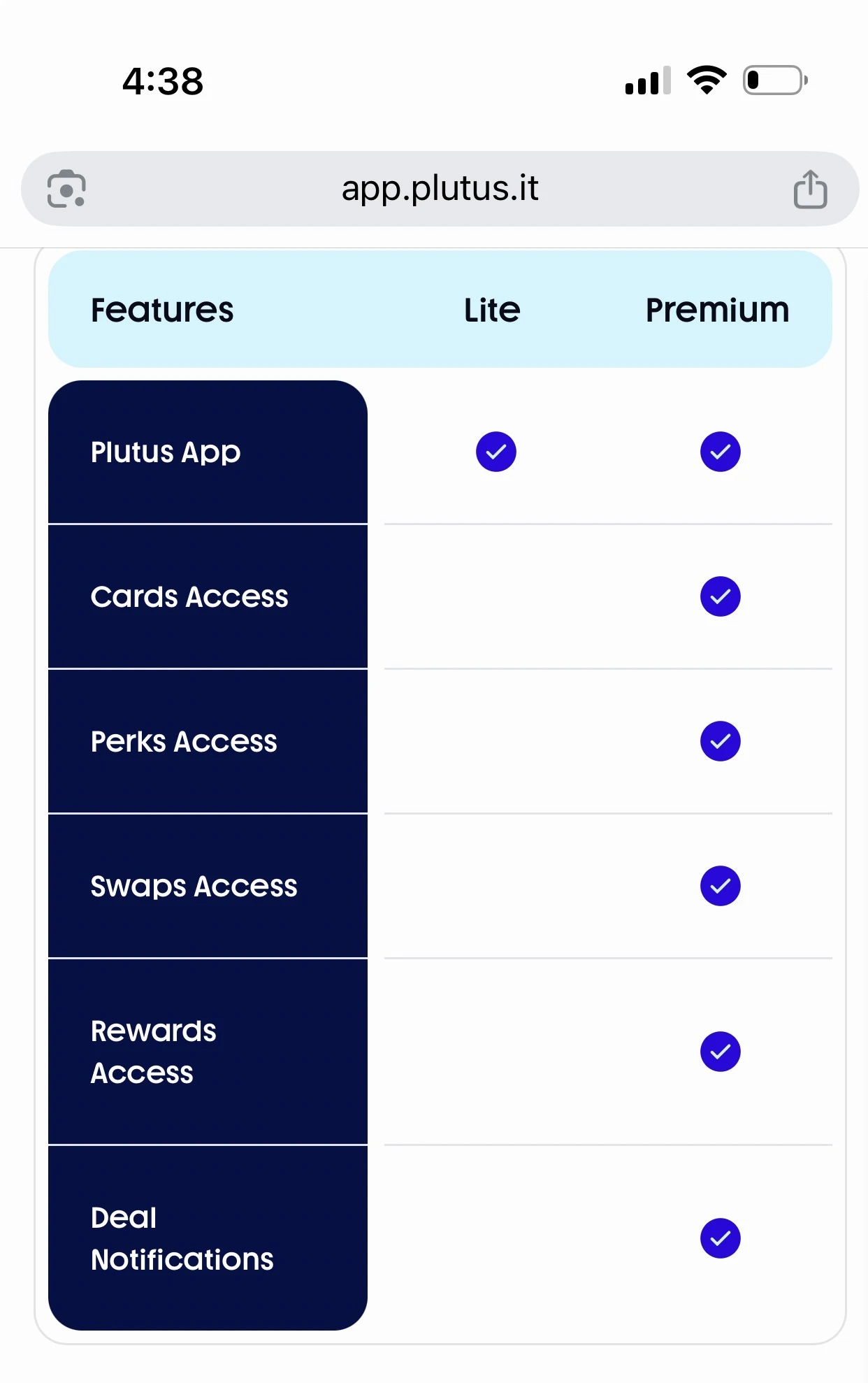

Lite vs Premium - Lite gets app access only. Premium unlocks cards, perks, swaps, rewards, and deal notifications. All plans are now paid (no free tier in 2026).

1. Subscription Plans (2026 Pricing)

-

Starter Plan: £6.99/month

- 3% cashback on up to £250 eligible spend per month

- 1 perk slot (£10 value)

- Best for: Testing the platform before committing to a higher tier

-

Everyday Plan: £9.99/month

- 3% cashback on up to £500 eligible spend per month

- 2 perk slots (£20 value)

- Best for: Regular domestic spenders in the £500-1,500/month range

-

Premium Plan: £19.99/month

- 3% cashback on up to £1,000 eligible spend per month

- 3 perk slots (£30 value)

- Best for: Users who maximize perks and stack PLU for higher rates

2026 pricing note: All plans are now paid - there is no free tier. Plutus states "Promo discount currently applied" on all plans, so these prices may increase further. The annual cost of Premium is approximately £240/year before any rewards.

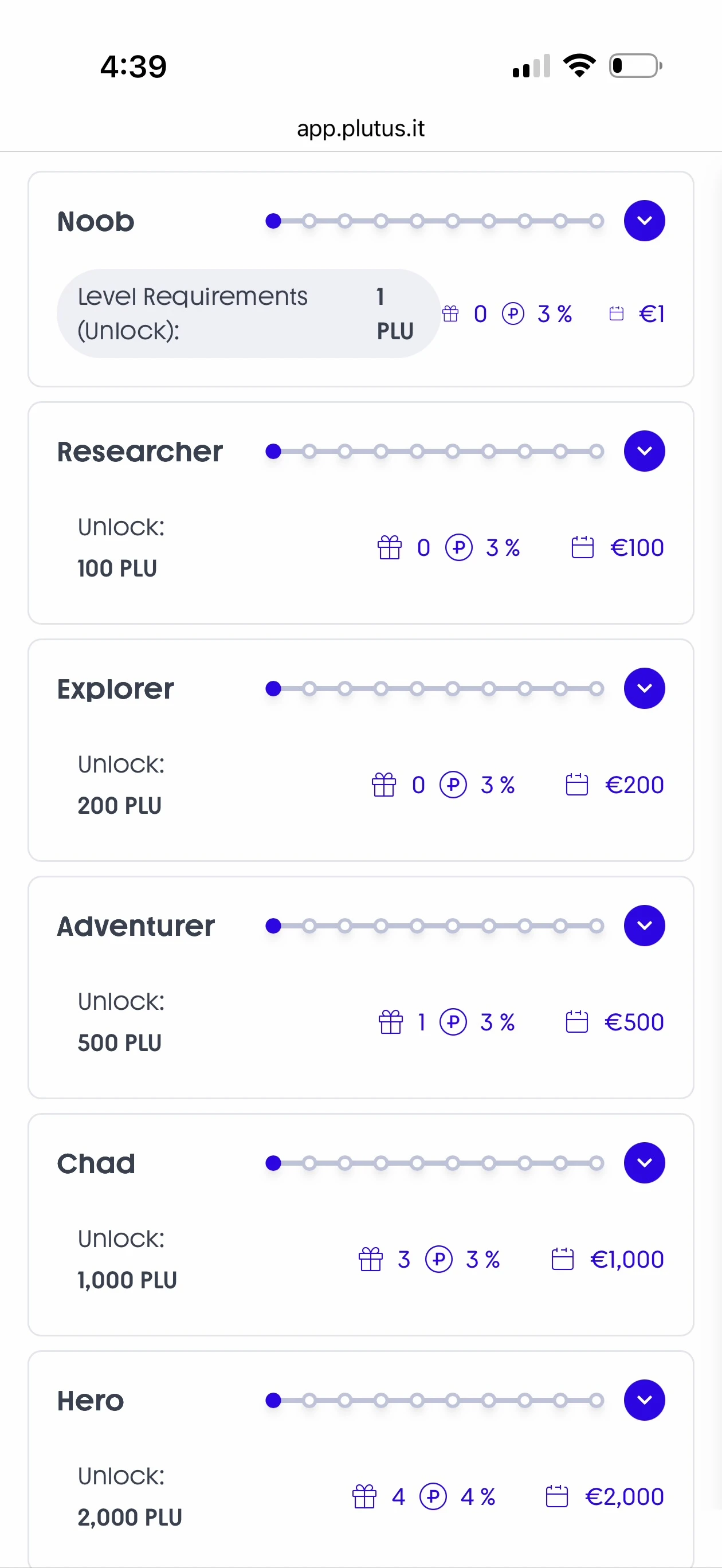

2. Stacking Tiers (Non-Custodial PLU Holdings)

Stacking Tiers (1-6) - Hold PLU in your own wallet to unlock higher rates. From Noob (1 PLU, 3%, EUR 1 cap) to Hero (2,000 PLU, 4%, 4 perks, EUR 2,000 cap). Non-custodial - Plutus reads your on-chain balance.

Hold PLU in your own wallet to unlock higher cashback rates. Plutus calculates your 30-day average balance:

| Tier | PLU Required | Cashback Rate | Perks | Monthly Reward Cap |

|---|---|---|---|---|

| Noob | 1 PLU | 3% | 0 | €1 |

| Researcher | 100 PLU | 3% | 0 | €100 |

| Explorer | 200 PLU | 3% | 0 | €200 |

| Adventurer | 500 PLU | 3% | 1 | €500 |

| Chad | 1,000 PLU | 3% | 3 | €1,000 |

| Hero | 2,000 PLU | 4% | 4 | €2,000 |

| Veteran | 3,000 PLU | 5% | 5 | €3,000 |

| Legend | 10,000 PLU | 6% | 6 | €10,000 |

| Myth | 20,000 PLU | 7% | 7 | €20,000 |

| G.O.A.T | 30,000 PLU | 8% | 8 | €30,000 |

| Honey Badger | 40,000 PLU | 9% | 9 | €40,000 |

PLU price as of March 2026: approx. $0.13 / £0.10. At this price, Legend tier (10,000 PLU) costs approx. £1,000 and Honey Badger (40,000 PLU) costs approx. £4,000. Prices fluctuate significantly.

3. Perks Program: £10 Monthly Rebates

Choose from 50+ merchants. When you spend at a perk merchant, the first £10 (or €10) is rebated 100% in PLU:

- Subscriptions: Netflix, Spotify, Disney+, Amazon Prime, YouTube Premium

- Groceries: Tesco, Aldi, Lidl, Sainsbury's, Waitrose

- Transport: Uber, Bolt, Trainline

- Retail: ASOS, eBay, JD Sports

- Utilities: British Gas, EDF Energy

Key insight: A user with Premium (3 perks from plan) gets £30/month in rebates from the plan alone. If stacking PLU at higher tiers, you unlock additional perk slots (e.g., Legend tier unlocks 6 perks total). Over 12 months, Premium plan perks alone yield £360 - enough to cover £240 annual subscription with £120 to spare. That narrow margin is why stacking is essential for Plutus to make financial sense.

Real-World ROI: The Break-Even Math

Let's calculate actual returns for three user profiles, accounting for subscription costs, PLU staking requirements, and token volatility risk.

Scenario A: Casual User (£1,500/month spend)

Setup:

- Everyday Plan: £9.99/month

- Adventurer tier (500 PLU stacked, approx. £50 at current prices): 3%, 1 tier perk

- Perks: 2 from plan (Netflix £10, Spotify £10)

- Eligible spend: £500 (Everyday plan limit - only the first £500 of the £1,500 earns rewards)

Monthly Math:

- Subscription cost: -£9.99

- Perks value: +£20 (2 perks)

- Eligible spend cashback: £500 x 3% = £15 in PLU

- Gross value: £35

- Net after subscription: £25.01/month = £300.12/year

Risk adjustment:

- If PLU drops 30%: £15 cashback becomes £10.50

- True net: £20.51/month = £246.12/year

Verdict: The eligible spend cap at £500 is the key bottleneck. Two-thirds of this user's spending (£1,000/month) earns zero rewards. Perks alone barely cover the subscription (£20 vs £9.99). For casual domestic spenders, Plutus works but delivers modest returns. For users who spend internationally, the 2.5% FX fee on that £1,000 of non-eligible spend would cost £25/month - wiping out all gains. Plutus only makes sense here for fully domestic spending.

Scenario B: Power User (£3,000/month spend, domestic)

Setup:

- Premium Plan: £19.99/month

- Legend tier (10,000 PLU stacked, approx. £1,000 at current prices): 6%, 6 perks

- Eligible spend: £1,000 (Premium plan limit - only the first £1,000 of £3,000 earns rewards)

- 6 perk slots from stacking tier (overrides plan's 3): £60 value/month

Monthly Math:

- Subscription cost: -£19.99

- Perks value: +£60 (6 perks)

- Eligible spend cashback: £1,000 x 6% = £60 in PLU

- Gross value: £120

- Net after subscription: £100.01/month = £1,200.12/year

Risk adjustment:

- 10,000 PLU staked (approx. £1,000 at-risk capital)

- If PLU drops 30%: £1,000 stake becomes £700 = -£300 loss

- Cashback in PLU also loses 30%: £60 becomes £42 effective

Net scenarios:

- PLU flat: +£1,200/year (120% ROI on staked capital)

- PLU -30%: +£984 - £300 = +£684/year (still positive)

- PLU -50%: +£840 - £500 = +£340/year (marginal)

Verdict: Premium + Legend stacking works for domestic power users. The £1,000 eligible spend cap means spending more than £1,000/month does not increase cashback. The value comes from perks (£720/year) more than cashback (£720/year). At £3,000/month, two-thirds of spending is reward-free. If any of that £2,000 overage is international, the 2.5% FX fee becomes a material cost.

Scenario C: Ultra-Maximizer (£5,000/month spend, domestic)

Setup:

- Premium Plan: £19.99/month

- G.O.A.T tier (30,000 PLU stacked, approx. £3,000 at current prices): 8%, 8 perks

- Eligible spend: £1,000 (Premium plan limit - same as Scenario B)

- 8 perk slots from stacking tier: £80 value/month

Monthly Math:

- Subscription: -£19.99

- Perks: +£80 (8 perks)

- Eligible spend cashback: £1,000 x 8% = £80 in PLU

- Gross: £160

- Net after subscription: £140.01/month = £1,680.12/year

Token risk:

- 30,000 PLU staked (approx. £3,000 at-risk capital)

- 30% drop = -£900 loss on stake + reduced cashback value

- Risk-adjusted (PLU -30%): £1,680 - £900 = £780/year (26% ROI on staked capital)

The eligible spend ceiling problem: At G.O.A.T tier, you earn 8% - but only on £1,000/month regardless of total spending. Cashback is capped at £80/month (£960/year). The extra £4,000/month in spending earns nothing. Compared to Scenario B (Legend), you invest 3x more capital (£3,000 vs £1,000) for only £240/year more cashback (£960 vs £720) plus 2 additional perks (£240/year more). That is a marginal return on 2x the additional capital.

Verdict: G.O.A.T tier only makes sense if you genuinely want 8 perks and believe PLU will appreciate. The diminishing returns above Legend tier are steep because eligible spend does not scale with stacking level.

How Plutus Compares: Head-to-Head Analysis

| Feature | Plutus Premium | Crypto.com Pro | Wirex Elite |

|---|---|---|---|

| Max Cashback | 9% (with 40,000 PLU) | 3% (with $5K CRO stake or $29.99/mo) | 8% (with 7.5M WXT locked 180 days) |

| Custody Model | ✅ Non-custodial (connect wallet) | ❌ Custodial (funds on exchange) | ❌ Custodial |

| Monthly Fee | £6.99-£19.99 | $29.99/mo or $5K CRO stake | £14.99 |

| Perks/Rebates | 50+ perks (£10 each), 1-3 plan slots | Spotify + Netflix rebates | None |

| FX Fees | ❌ 2.5% non-domestic | ❌ 1% FX markup | ✅ 0% |

| Regions | UK + EEA only | Global (except US) | Global |

| Best For | UK/EU domestic perk optimizers | Global travelers | High spenders abroad |

Plutus wins on:

- Highest cashback ceiling (9% vs 3-8%)

- Non-custodial security model

- Perk variety and flexibility (50+ merchants)

Plutus loses on:

- 2.5% FX fee on non-domestic transactions (Wirex and many competitors charge 0%)

- Geographic availability (UK/EEA only)

- No free tier - all plans require £6.99-£19.99/month subscription

- Low eligible spend caps (max £1,000/month on Premium) limit actual cashback earned

- Complexity (subscription + stacking + eligible spend + perks = steep learning curve)

- Token liquidity (PLU has lower volume than CRO or WXT)

The Perks Strategy: How to Maximize £10 Rebates

The real art of Plutus is perk selection strategy. With Premium's 3 plan slots (expandable to more via stacking tiers), every perk choice matters more than before.

Strategy 1: Subscription Stack (3 perks, Premium plan only)

- Netflix (£10)

- Spotify (£10)

- Disney+ (£10)

- Total saved: £30/month = £360/year on subscriptions you already pay for

- This alone covers 75% of the Premium subscription cost (£240/year)

Strategy 2: Grocery Focus (3 perks, Premium plan only)

- Tesco (£10)

- Aldi (£10)

- Sainsbury's (£10)

- Strategy: Rotate stores. Shop at least £10 at each monthly to trigger all perks = £30/month

Strategy 3: High-Stacker Hybrid (6+ perks, Legend tier or above)

- Netflix (£10) + Spotify (£10) + Tesco (£10) from plan/base perks

- Uber (£10) + Shell (£10) + Amazon Prime (£10) from stacking tier perks

- Total saved: £60/month = £720/year

- This is where the economics genuinely work: £720 in perks vs £240 subscription = £480 net

Pro tip: Change perks monthly. If you will not use Netflix this month, swap it for something you will. With only 3 plan slots (unless stacking), the flexibility is more important than ever - every idle perk is £10 wasted.

2026 Regulatory Status: UK FCA Compliance

E-Money Institution (EMI) License: Plutus operates under a UK Electronic Money Institution license, issued by the Financial Conduct Authority (FCA) in 2021 and renewed in 2024. This means:

- ✅ Your fiat GBP/EUR balance is safeguarded (held in segregated accounts at Modulr FS Limited)

- ✅ Regulatory oversight for KYC/AML compliance

- ✅ Customer protection under UK Electronic Money Regulations 2011

What's NOT protected:

- ❌ Your PLU tokens (held in your own wallet, not covered by EMI license)

- ❌ PLU price volatility

- ❌ Smart contract risk (PLU is an ERC-20 token on Ethereum/Polygon)

2026 Update: Post-Brexit, Plutus operates separately in UK vs EEA. EEA users are serviced through a Lithuanian EMI license (secured Q3 2025), which covers MiCA compliance.

Red flag watch: If Plutus loses its EMI license, the card stops working within 90 days. However, your PLU tokens in your own wallet remain accessible—you just lose the spending utility.

What Happens If Plutus Fails?

Bankruptcy Scenario Analysis:

Your fiat balance (GBP/EUR on card):

- Held in segregated accounts at Modulr (third-party banking partner)

- Protected under EMI regulations

- You'd likely recover 100% within 30-90 days through FCA claims process

Your PLU tokens:

- Held in YOUR wallet (MetaMask, Ledger, etc.)

- Not at risk from Plutus bankruptcy

- You could sell PLU on Uniswap or continue holding

Your reward history:

- Earned PLU is distributed monthly

- If Plutus fails mid-month, you might lose that month's pending rewards

- Estimated max exposure: approx. £90 (Premium £1,000 eligible spend at 9% max rate)

Comparison to FTX/Celsius:

- FTX users: Lost 100% of custodial balances (3+ years to recover 10-30%)

- Plutus users: Would lose current month's pending rewards only (up to approx. £90 + perk rebates)

The non-custodial moat: We track every card's failure scenario, and this is clearly Plutus's core value proposition. Even catastrophic failure affects only your pending monthly rewards, not your stacked PLU or historical earnings.

How the Transaction Flow Actually Works

Scenario: You buy £50 of groceries at Tesco

Step 1: You load fiat onto Plutus card

- Bank transfer (GBP) → Modulr banking partner → Your Plutus card balance

- Instant via UK Faster Payments

Step 2: You tap to pay at Tesco

- Visa network processes £50 charge

- Funds debited from your GBP balance (no crypto touched)

Step 3: Plutus calculates rewards (behind the scenes)

- You have Tesco as a perk: £10 rebated 100% = £10 in PLU

- Remaining £40 earns 6% (Legend tier) = £2.40 in PLU

- Total earned: £12.40 in PLU

Step 4: PLU distributed monthly

- All purchases from the month are tallied

- Around the 5th of next month, PLU is sent to your connected wallet

- You receive PLU directly on Polygon (low gas fees)

Step 5: You decide what to do with PLU

- Hold: Maintain stacking tier for next month

- Sell: Swap on Uniswap for USDC/ETH

- Stake: Some users stake PLU in DeFi for additional yield

Gas costs: Plutus pays the gas to send you PLU. You only pay gas if you move it later.

Tax Implications (UK/EEA Context)

In the UK (HMRC guidance):

-

Earning PLU rewards:

- Treated as miscellaneous income

- Taxable at the GBP value when received

- If you earn £1,000 PLU rewards in 2026, you owe income tax on £1,000

-

Spending the PLU later:

- Capital gains tax applies

- Cost basis = value when you received it

- Example: Received £10 PLU → Now worth £15 → You owe CGT on £5 gain

- UK CGT allowance 2026: £3,000 (reduced from £6,000 in 2023)

-

Perks treatment:

- HMRC considers perks as purchase rebates (non-taxable)

- Netflix rebate = not taxable

- But the PLU you receive for the rebate IS taxable

Record-keeping nightmare: Every purchase generates a taxable event - a fact that rarely surfaces in typical Plutus card reviews. Premium users making 100 transactions/month have 1,200 annual tax events. Use Koinly or CoinTracker for automatic reporting.

EEA variation: Germany, France, and Netherlands have similar frameworks. Some countries (Portugal, Malta) don't tax crypto-to-crypto transactions, making PLU rewards more tax-efficient.

Advanced Strategies: Gaming The System

Strategy 1: The Stacking Ladder

- Start month at Veteran tier (3,000 PLU)

- Mid-month, PLU price drops 20%

- Buy 7,000 more PLU cheaply

- Next month, qualify for Legend tier at below-market cost

- When PLU recovers, you've captured both the tier upgrade and price appreciation

Strategy 2: The Dual-Card Setup (Essential in 2026)

- Plutus for domestic GBP/EUR spending within perk merchants and eligible spend cap

- A 0% FX card (Crypto.com, Wirex, or Gnosis Pay) for all international spending

- Switch based on merchant and currency

Example monthly allocation (UK resident, Premium + Legend):

- Domestic perk merchants: Plutus (£500) → £60 perks + £30 cashback (6%)

- Domestic non-perk spend: Plutus (£500, hitting eligible cap) → £30 cashback (6%)

- International spending: Wirex/Crypto.com (£1,000) → 0% FX vs Plutus's 2.5% = £25 saved

- Combined: £120/month Plutus + no FX penalties = best of both worlds

The 2.5% FX fee makes a dual-card approach mandatory for anyone who travels or shops internationally.

Who Should Use Plutus in 2026?

Ideal user profile:

- ✅ Lives in UK or EEA

- ✅ Spends primarily in domestic currency (GBP or EUR) - NOT a travel card

- ✅ Already uses self-custody wallets (MetaMask, Ledger)

- ✅ Has subscriptions to Netflix, Spotify, etc. (to maximize perk value)

- ✅ Comfortable with PLU token volatility

- ✅ Willing to actively manage perk selections monthly

- ✅ Values non-custodial security over simplicity

Who should avoid:

- ❌ Frequent international spenders (2.5% FX fee eliminates travel value)

- ❌ Beginners new to crypto (stacking + perks + eligible spend = high complexity)

- ❌ Users outside UK/EEA

- ❌ Low monthly spending (under £500 - Starter plan barely breaks even)

- ❌ Wants "set it and forget it" simplicity

- ❌ Cannot handle seed phrase responsibility

Where it lands in 2026: Plutus is a niche card for dedicated domestic perk optimizers. The 2026 pricing changes (no free tier, 2.5% FX, lower perk counts per plan) narrowed its value case significantly compared to 2024-2025. It is no longer a general-purpose European card and definitely not a travel card.

For crypto-native users in the UK/EEA who already manage wallets and will actively optimize perk selections, Plutus still offers the highest theoretical cashback rate in the market (9%). For everyone else - especially travelers or casual users - a simpler card like Crypto.com, Wirex, or Gnosis Pay delivers better value with less effort.

Fees and ROI framework

All plans paid: Starter (£6.99/month, £250 eligible spend, 1 perk), Everyday (£9.99/month, £500 eligible spend, 2 perks), Premium (£19.99/month, £1,000 eligible spend, 3 perks). Annual cost of Premium: approx. £240. Non-domestic FX fee: 2.5%. ATM fee: 2.5%. Physical card: £9.99. Stacking tiers (1-40,000 PLU in your own wallet) boost cashback from 3% to 9% and unlock additional perks beyond plan limits. At £3,000/month domestic on Premium + Legend (10,000 PLU stacked, approx. £1,000), expect approx. £1,200/year net. Perk value is critical: at Legend (6 perks x £10 = £60/month = £720/year), perks exceed subscription cost by £480.

Competitor comparison

- vs Crypto.com Pro: Crypto.com offers 3% CRO with $5K stake or $29.99/mo (custodial, locked), 0% FX, and lounge access. Plutus offers up to 9% PLU with non-custodial stacking but 2.5% FX fee, no lounge access, and eligible spend capped at £1,000/month. Plutus wins on max cashback rate and custody model. Crypto.com wins on global availability, 0% FX, uncapped eligible spend at higher tiers, and lounge access.

- vs Wirex: Wirex offers up to 8% WXT cashback (custodial) with 0% FX and 35-country availability. Plutus matches or beats on max rate (9%) and offers non-custodial custody. But Wirex's 0% FX and simpler setup make it the better all-purpose European card. Plutus wins only for dedicated domestic perk optimizers.

- vs Gnosis Pay: Both non-custodial European cards. Gnosis offers up to 5% in GNO with 0% FX and full on-chain transparency. Plutus has a higher max rate (9% vs 5%) but 2.5% FX makes it domestic-only. For mixed domestic/international spending, Gnosis is the better non-custodial option.

- vs Bybit: Bybit offers 2-10% with 0% FX (custodial). Plutus offers 3-9% with 2.5% FX (non-custodial). For international spending, Bybit wins decisively. For domestic UK/EEA perk optimization, Plutus offers non-custodial security.

Availability and compliance notes

UK and EEA only. Not available in US, APAC, or LATAM. UK users under FCA EMI license. EEA users under Lithuanian EMI license (MiCA-compliant, secured Q3 2025). Fiat balances safeguarded at Modulr FS Limited. PLU tokens remain in user's wallet (non-custodial). Standard KYC required. Transaction limits: £500K single transaction, £1M per 30 days (all plans).

Sources and Verification

Frequently Asked Questions

Do I need to send my PLU to Plutus to earn rewards?

No. Plutus uses a non-custodial model. You connect your external wallet (e.g., MetaMask) to the Plutus app to verify your balance and unlock reward tiers.

Where is Plutus available?

Plutus is available to residents of the United Kingdom and the European Economic Area (EEA).

Is the Plutus Card a credit card?

No. The Plutus Card is a Visa debit card, not a credit card. You spend from your Plutus account balance - there is no credit line, no APR, and no credit check. For crypto-backed credit card options, see our reviews of Gemini, ether.fi, Nexo, and Avici.

App Store (4 ratings)

Source: Apple App Store - Updated Feb 2026