Issued by Solflare

VIRTUAL CARD

Verified

SELF CUSTODY SPEND

Verified

NO ANNUAL FEE

Verified

Our Official Verdict

Native Solana Spend: 0% Reload Fees + Airdrop Access

The Solflare Card is the most integrated way to spend Solana assets in the real world. By offering speculative TBD potential through its 'Benefits' platform and a Free annual fee, it serves the needs of both the daily spender and the ecosystem degen.

Fees & Charges

Annual Fee

Free

FX Fee

1%

ATM Fee

2%

Requirements

Supported Regions

EEA, UK

Spendable Assets

USDC

Solflare Card Review

The Solflare Card is a self-custodial Mastercard debit card integrated with the Solflare Solana wallet, enabling USDC spending at Mastercard merchants with on-chain settlement at Solana speed, 1% FX fee on non-USD transactions, 0% bank reload fee, 1% crypto reload fee, raffle-based rewards via The Benefits platform (direct cashback scheduled for 2026), instant virtual card issuance, Google Pay support, and $0 annual fee, available in the EEA and UK.

Solana's Native Spending Card

The Solflare Card lets you spend USDC directly from your self-custodial Solflare wallet at any Mastercard merchant. Your funds stay in your wallet until the moment of purchase - the card triggers an on-chain Solana transaction that settles in under a second. No exchange, no intermediary balance, no custodial risk on your main holdings.

In this review, we break down the real costs and self-custody trade-offs. This is a pure ecosystem play. If you live in the Solana ecosystem - staking SOL, farming DeFi yields, collecting NFTs - the Solflare Card is the native spending rail that keeps everything in one wallet. There is no cashback yet (raffle-based rewards only), which means every transaction costs you the 1% FX fee without any offset. The card's value is in self-custodial convenience, not economics.

Direct cashback is scheduled for later in 2026. When it launches, the economics should improve significantly. Until then, you are paying 1% for the privilege of self-custodial spending.

Card Specs: What You Are Actually Getting

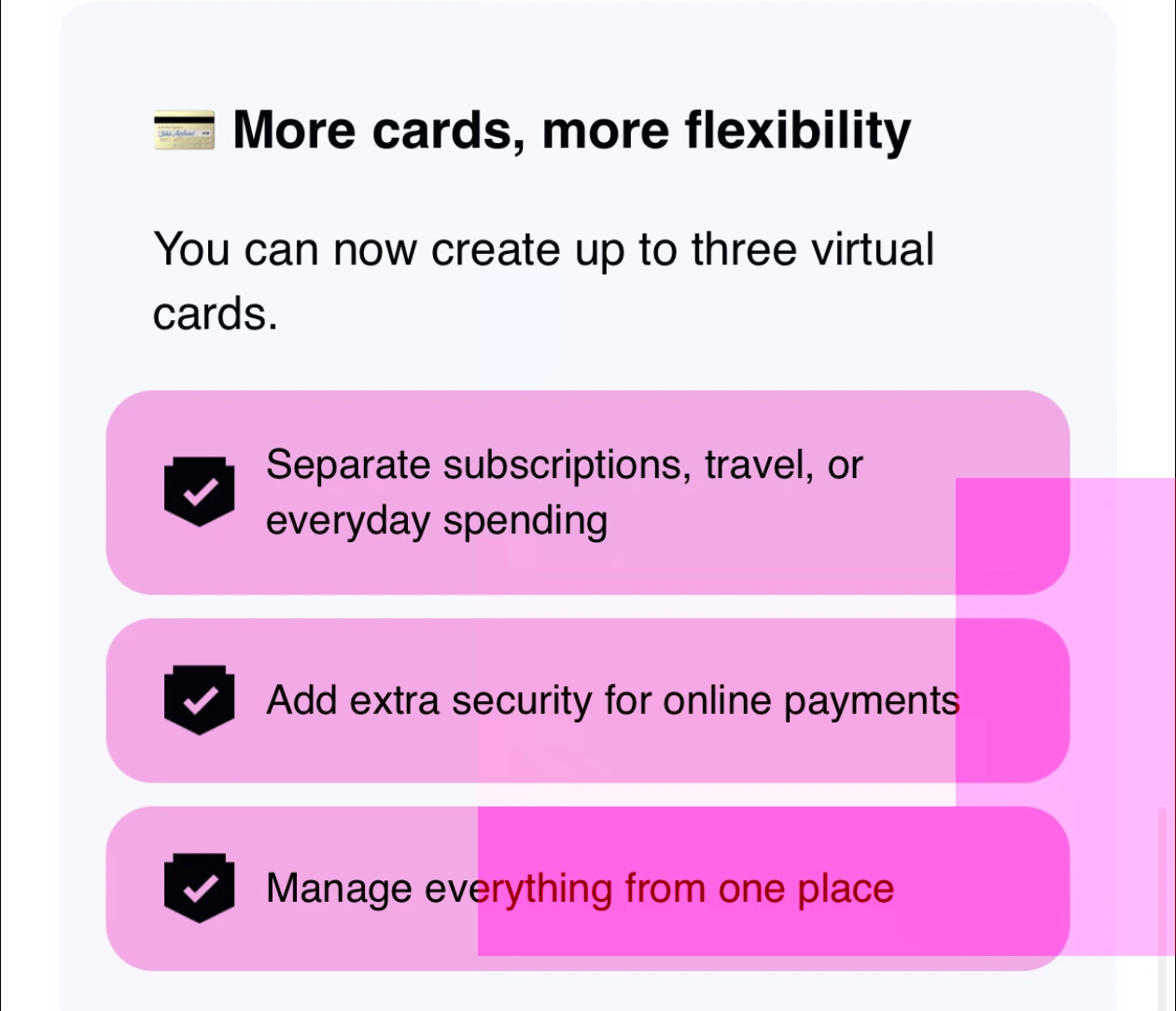

Physical and Virtual Cards

- Virtual card: Instant issuance through the Solflare wallet app

- Up to 3 virtual cards: Separate cards for subscriptions, travel, or everyday spending

- Physical card: Not currently available (virtual only)

- Design: Solflare branding integrated into the wallet app

Payment Network

- Network: Mastercard

- Acceptance: 100M+ merchant locations worldwide

- Contactless: Yes (NFC via Google Pay)

- Mobile wallets: Google Pay (Apple Pay coming soon)

- Card type: Debit (spends USDC from self-custodial Solflare wallet)

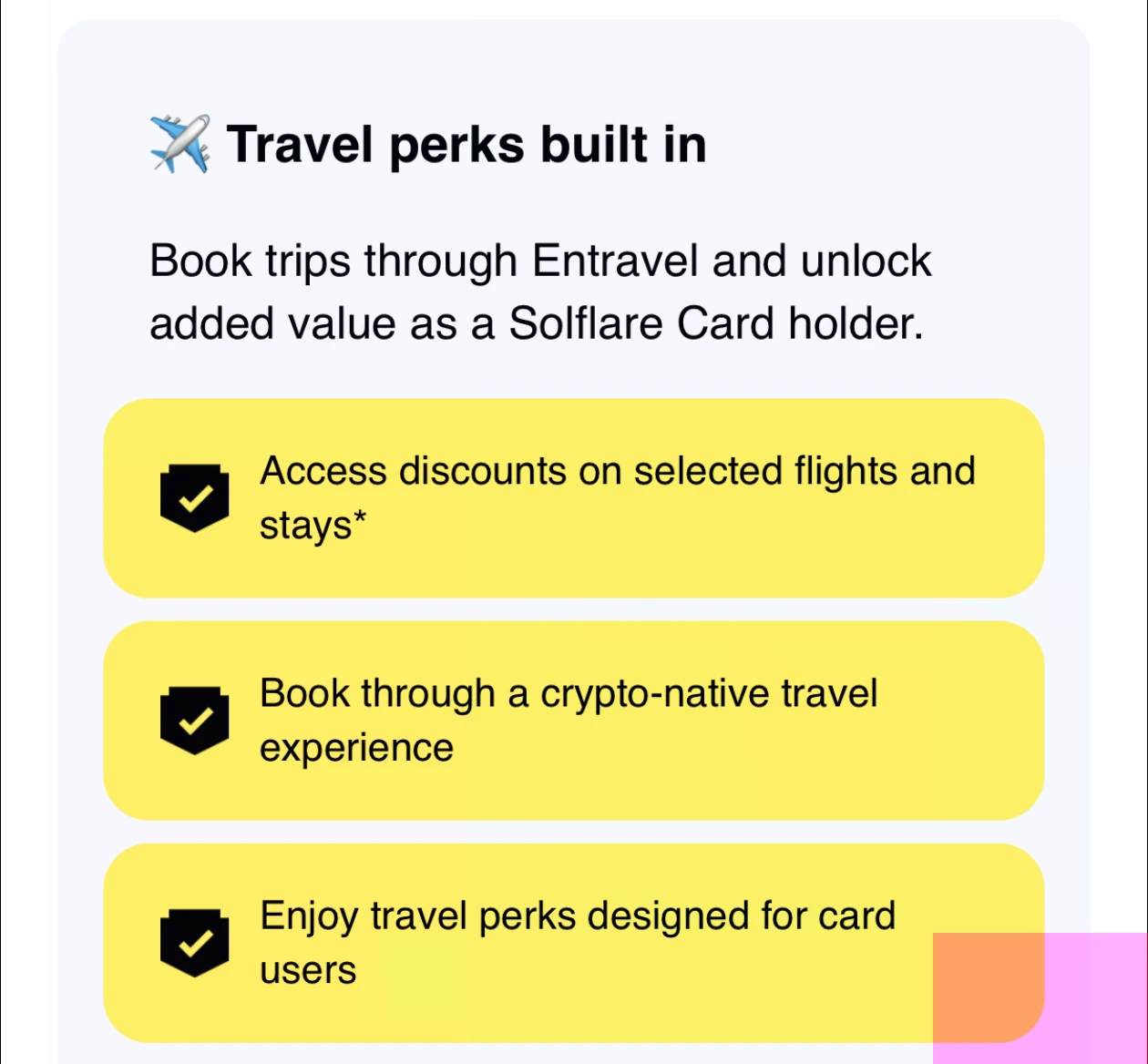

Travel Perks via Entravel

Solflare cardholders get integrated travel booking through Entravel directly in the wallet app. Hotel bookings are live with discounts up to 55% off, and flight bookings across 600+ airlines are coming soon. All bookable with the Solflare Card.

Security Features

- Self-custodial: You hold the private keys. Solflare never has access to your funds

- Solana speed: On-chain settlement in under 1 second

- Card controls: Freeze/unfreeze via Solflare app

- Transaction alerts: Real-time push notifications

- Mastercard protections: Standard zero liability for unauthorized transactions

How Spending Works: Transaction Flow

Example: EUR 120 dinner in Barcelona (paying from USDC balance in Solflare wallet)

Step 1: Have USDC in your wallet

- Hold USDC in your Solflare wallet on Solana

- Your USDC is self-custodial - only you control the keys

- No top-up or transfer to a separate card balance needed

Step 2: Pay at the restaurant

- Open Google Pay or present your virtual card number

- Restaurant charges EUR 120

Step 3: On-chain settlement

- Solflare triggers a Solana transaction from your wallet

- USDC is converted to EUR at the prevailing rate

- Settlement completes in under 1 second (Solana block time)

Step 4: Fees applied

- FX fee: 1% of EUR 120 = EUR 1.20

- Reload fee: 0% (if USDC was loaded via bank transfer) or 1% (if loaded via crypto conversion)

- Total fee: EUR 1.20 (bank-funded) or EUR 2.40 (crypto-funded)

Step 5: Rewards

- Raffle entry earned via The Benefits platform

- No direct cashback on this transaction (coming later in 2026)

- Net cost: -EUR 1.20 to -EUR 2.40 depending on funding method

The self-custody advantage: Your EUR 5,000 in USDC never left your wallet until this EUR 120 transaction. If a centralized exchange went bankrupt overnight, your spending balance is unaffected. You paid EUR 1.20 for that security. Whether that trade-off is worth it depends on how much you value sovereignty over your funds.

Fee Deep Dive: The Real Cost

| Fee | Amount | Notes |

|---|---|---|

| Annual fee | $0 | No subscription |

| FX fee | 1% | On all non-USD transactions |

| Bank reload | 0% | SEPA/bank transfer to fund wallet |

| Crypto reload | 1% | Converting crypto to USDC for card |

| ATM fee | 2% | After initial free allowance |

| Monthly fee | $0 | No maintenance charge |

Net Cost Analysis (No Cashback Currently)

| Funding Method | FX Fee | Reload Fee | Total Cost per EUR 100 |

|---|---|---|---|

| Bank-funded (SEPA) | -EUR 1.00 | EUR 0 | -EUR 1.00 |

| Crypto-funded (SOL to USDC) | -EUR 1.00 | -EUR 1.00 | -EUR 2.00 |

Annual Cost at Different Spending Levels

| Monthly Spend | Bank-Funded Cost | Crypto-Funded Cost |

|---|---|---|

| EUR 500 | -EUR 60/year | -EUR 120/year |

| EUR 1,000 | -EUR 120/year | -EUR 240/year |

| EUR 2,000 | -EUR 240/year | -EUR 480/year |

| EUR 3,000 | -EUR 360/year | -EUR 720/year |

Key insight: After reviewing the fee structure, without cashback every transaction is a net cost. Bank-funded spending minimizes the damage (1% FX only). Crypto-funded spending doubles the cost (1% FX + 1% reload). When direct cashback launches in 2026, these economics should reverse - but do not count on it until it is live.

The Benefits Platform: Raffle Rewards

Instead of traditional cashback, Solflare runs The Benefits - a raffle-based rewards platform. The launch promotion was a Porsche 911 GT3 raffle that ended February 14, 2026. Every card transaction earns points toward periodic draws.

How it works:

- Make purchases with the Solflare Card

- Earn raffle entries proportional to spending

- Winners drawn periodically

- Past prizes have included high-value items and experiences

Honest assessment: Raffle-based rewards have a lower expected value than direct cashback for most users. If 10,000 users each spend EUR 1,000 and one wins a EUR 150,000 Porsche, the expected value per user is EUR 15 - well below the 1% FX fee they each paid (EUR 10). The raffle is exciting but not economically rational compared to a card that pays 1%+ cashback.

Direct cashback is scheduled for later in 2026. When it launches, the Solflare Card's economics should become competitive with other self-custodial options.

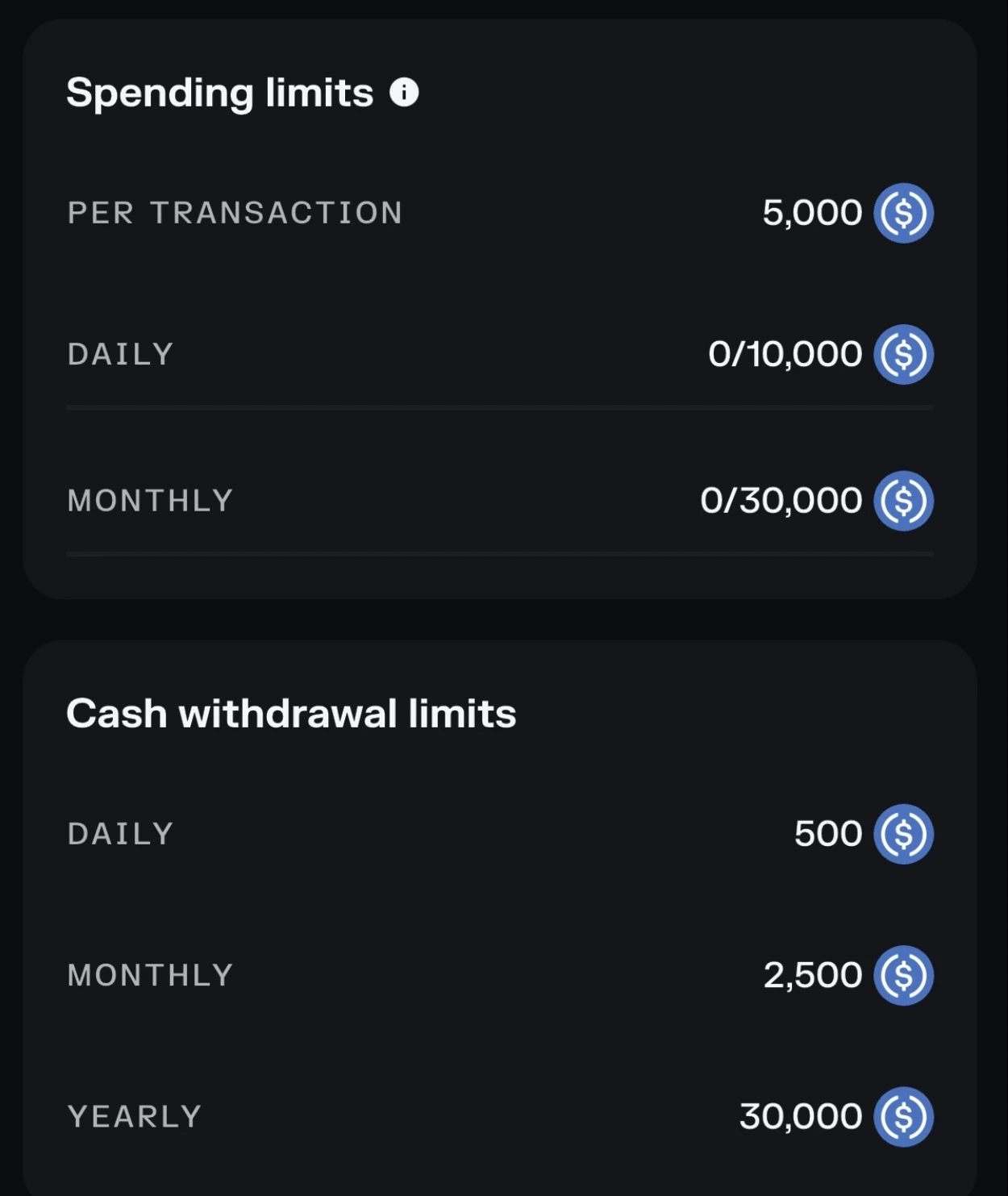

Limits and Restrictions

| Limit | Amount |

|---|---|

| Per transaction | $5,000 |

| Daily spending | $10,000 |

| Monthly spending | $30,000 |

| ATM daily | $500 |

| ATM monthly | $2,500 |

| ATM yearly | $30,000 |

| Supported assets | USDC only (on Solana) |

| Annual fee | $0 |

| Card type | Virtual only |

Availability

- Regions: EEA, UK

- KYC: Standard verification required

- Wallet: Solflare wallet required (self-custodial)

- Chain: Solana only (USDC-SPL)

- Apple Pay: Coming soon (Google Pay live)

What Happens If Solflare Goes Down?

Your USDC in wallet:

- Self-custodial. Your seed phrase gives you access to your USDC regardless of Solflare's operational status

- USDC on Solana is a Circle-issued stablecoin - it exists on the blockchain independently

- You can import your seed phrase into any Solana wallet (Phantom, Backpack) and access your funds

- Your funds are safe even if Solflare's company fails

Your card functionality:

- The card depends on Solflare's issuing partnerships

- If the card program shuts down, you lose the spending rail but keep all your crypto

- This is the fundamental advantage of self-custody: the worst case is losing the card, not the funds

Your raffle entries and rewards:

- Platform-dependent. Unredeemed raffle entries would be lost in a shutdown

- Future cashback (when launched) would follow the same pattern

Risk comparison:

| Card | Asset Safety | Card Dependency | Fund Recovery |

|---|---|---|---|

| Solflare Card | Self-custody (seed phrase) | Solflare + issuer | Import to any Solana wallet |

| Gnosis Pay | Self-custody (Safe account) | Gnosis + issuer | Access via any Safe interface |

| ether.fi Core | Self-custody (ether.fi wallet) | ether.fi + issuer | On-chain assets recoverable |

| Ready Lite | Self-custody (Starknet) | Ready + Kulipa | Starknet wallet recoverable |

Assessment: Very low asset risk (self-custody), medium card risk (depends on Solflare's partnerships). The self-custodial model means you never lose your USDC - only the convenience of spending it via Mastercard. This is the best possible risk profile for a crypto card.

Real User Scenarios

Scenario 1: Alex (Berlin Solana Developer, EUR 2,500/month spending)

Setup:

- Solflare Card (EEA, virtual via Google Pay)

- Holds 500 SOL + 5,000 USDC in Solflare wallet

- Funds card via bank transfer (SEPA, 0% reload)

- 90% EUR domestic, 10% international

- Active in Solana DeFi (Marinade, Jupiter, Raydium)

Results after 12 months:

- Total spending: EUR 30,000

- FX fees (1% on all transactions): -EUR 300

- Reload fees (0% bank-funded): EUR 0

- Raffle entries: Multiple (no wins)

- Net annual cost: -EUR 300

His verdict: "I pay EUR 300/year for the convenience of spending from my self-custodial Solana wallet. Is it worth it? For me, yes. My SOL and USDC stay in my wallet earning DeFi yield until I spend. I do not trust centralized exchanges after FTX. The EUR 300 cost is my insurance premium for sovereignty. When cashback launches, the math should flip positive. Until then, I accept the cost as part of my self-custody thesis."

Scenario 2: Emma (London NFT Artist, GBP 1,500/month spending)

Setup:

- Solflare Card (UK availability)

- Earns USDC from NFT sales on Solana

- Funds card via crypto reload (1% fee since her income is already in crypto)

- 100% GBP spending

Results after 12 months:

- Total spending: GBP 18,000

- FX fees (1%): -GBP 180

- Crypto reload fees (1%): -GBP 180

- Net annual cost: -GBP 360

Her verdict: "The 2% combined cost (1% FX + 1% crypto reload) is painful. GBP 360/year is a lot to pay for convenience. I am watching for the cashback launch - if they offer even 2% back, I break even. The reason I do not switch to Gnosis Pay (0% fees, 1-5% cashback) is that my entire portfolio is on Solana. Moving to Gnosis Chain means bridging assets, and I do not want the complexity or the bridge risk. I pay the Solflare premium to stay in one ecosystem."

Scenario 3: Marco (Milan DeFi Researcher, EUR 800/month spending)

Setup:

- Solflare Card (EEA, light spender)

- Holds 100 SOL + 2,000 USDC

- Bank-funded (0% reload)

- 100% EUR domestic

- Entered the Porsche 911 raffle (ended Feb 14, 2026)

Results after 12 months:

- Total spending: EUR 9,600

- FX fees (1%): -EUR 96

- Raffle: No win

- Net annual cost: -EUR 96

His verdict: "EUR 96/year is manageable for a card that keeps my funds in my own wallet. I treat it as a small cost for self-custody convenience. The Porsche raffle was fun but I had no realistic expectation of winning. What I am really waiting for is the cashback - at even 1%, this card breaks even on my spending. At 2%+, it becomes genuinely profitable. The Solflare wallet itself is excellent (4.84 stars), and having my card integrated directly into it is elegant. I just wish the economics were better today."

How the Solflare Card Compares

For self-custodial spending cards:

- Gnosis Pay: 0% all fees, 1-5% GNO cashback, self-custodial via Safe, EEA only. Gnosis Pay is strictly superior on economics (0% fees + cashback vs 1% fees + no cashback). Solflare wins only for Solana ecosystem users who do not want to bridge to Gnosis Chain

- ether.fi Core: 3% cashback, 1% FX, self-custodial, Ethereum ecosystem. ether.fi wins on rewards (3% vs none) with the same 1% FX cost. Solflare wins for Solana users only

- Ready Lite: 0.5% STRK cashback, 1% FX, self-custodial on Starknet. Ready wins on having at least some cashback (0.5% vs 0%). Similar fee structure. Different chain ecosystem

For Solana users specifically:

- The Solflare Card is the only self-custodial Solana card. There is no alternative that spends directly from a Solana wallet. If you must stay on Solana and want self-custody, this is your only option

- The Gemini Solana Edition earns SOL rewards but is a custodial credit card (US only) - fundamentally different product

Solflare's unique value: The only self-custodial spending card on the Solana blockchain. If you live in the Solana ecosystem and refuse to bridge to Ethereum or Gnosis Chain, this is your only option for self-custodial Mastercard spending. The economics are currently negative (1-2% cost per transaction), but the self-custody value proposition and upcoming cashback launch make it a card to watch.

The Verdict: Is the Solflare Card Worth It in 2026?

Use the Solflare Card if:

- You hold USDC on Solana and want to spend without bridging to another chain or using a centralized exchange

- You value self-custody enough to pay the 1% FX premium

- You are in the EEA or UK where the card is available

- You want to be positioned for the upcoming cashback launch

Skip the Solflare Card if:

- You want positive returns on spending - without cashback, every transaction is a net cost. Use Gnosis Pay (0% fees + cashback) or ether.fi (3% cashback)

- You are not in the Solana ecosystem - there is no reason to use this over multi-chain alternatives

- You need Apple Pay - only Google Pay is currently supported

- You want a physical card - virtual only at this time

- Your spending is crypto-funded - the combined 2% cost (1% FX + 1% reload) is prohibitive

Final verdict: Our review confirms that the Solflare Card is a self-custody convenience tool, not a rewards product. It costs 1-2% per transaction with zero cashback return. Its value is entirely in keeping your USDC in your own Solana wallet until the moment of purchase - a genuine benefit for users who prioritize sovereignty over economics. For Solana-native users who refuse to use centralized exchanges or bridge to other chains, it is the only option. The upcoming cashback launch could transform the economics from negative to positive. Until then, treat the 1% FX fee as the price of self-custodial convenience on Solana, and evaluate whether that premium is worth it against alternatives like Gnosis Pay (0% fees, 1-5% cashback) that require a different chain.

Sources and Verification

All card specs, fees, and limits verified from:

FAQ

How do you choose Solflare Card crypto cards?

We compare verified issuer sources, fees, and eligibility. Availability can change, so confirm with the issuer before applying.

Do all cards in this list offer the same benefits?

No. Each issuer defines its own program terms. Review the sources on each card profile.

Are these rankings or recommendations?

No. Lists are filtered views of cards in our database and do not imply rankings.

This is a debit card. Some merchants with pre-authorization holds (hotels, car rentals) may temporarily hold funds beyond the transaction amount.

You retain custody of your funds until the moment of spending. Your balance is not exposed to provider insolvency risk.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Last verified: Mar 5, 2026 · Data sourced from official Solflare documentation. · Methodology

★★★★★4.8/5 App Store (9.2K ratings)