SpendNode Rating

Payy is easier to like if you want a quiet stablecoin card rather than a big ecosystem pitch. That simplicity counts for something.

3.4 on Operational Reliability and 3.5 on Product Utility. Those are the weakest scores in the stablecoin category. Payy is early. The self-custody flavor and the quiet simplicity earn goodwill, but goodwill alone does not move a rating when the product is still catching up to cards that have been live longer and do more.

How It Competes

Cost Efficiency

4.0

Product Utility

3.5

Custody & Trust

3.9

Reliability & UX

3.4

Transparency

3.6

SELF CUSTODY SPEND

Verified

VIRTUAL CARD

Verified

APPLE PAY

Verified

Our Official Verdict

Private Stablecoin Spending: 0% Fees + ZK Proof Settlement

The Payy Card is the only crypto card that genuinely hides your on-chain activity from public view. With Free annual fee, 1% FX on non-USD purchases, and no rewards, it is purpose-built for users who value privacy and self-custody above cashback.

Fees & Charges

Annual Fee

Free

FX Fee

1%

ATM Fee

TBD

Requirements

Supported Regions

GLOBAL

Spendable Assets

USDC, USDT, USDC.e

On This Page

What Is the Payy Card?

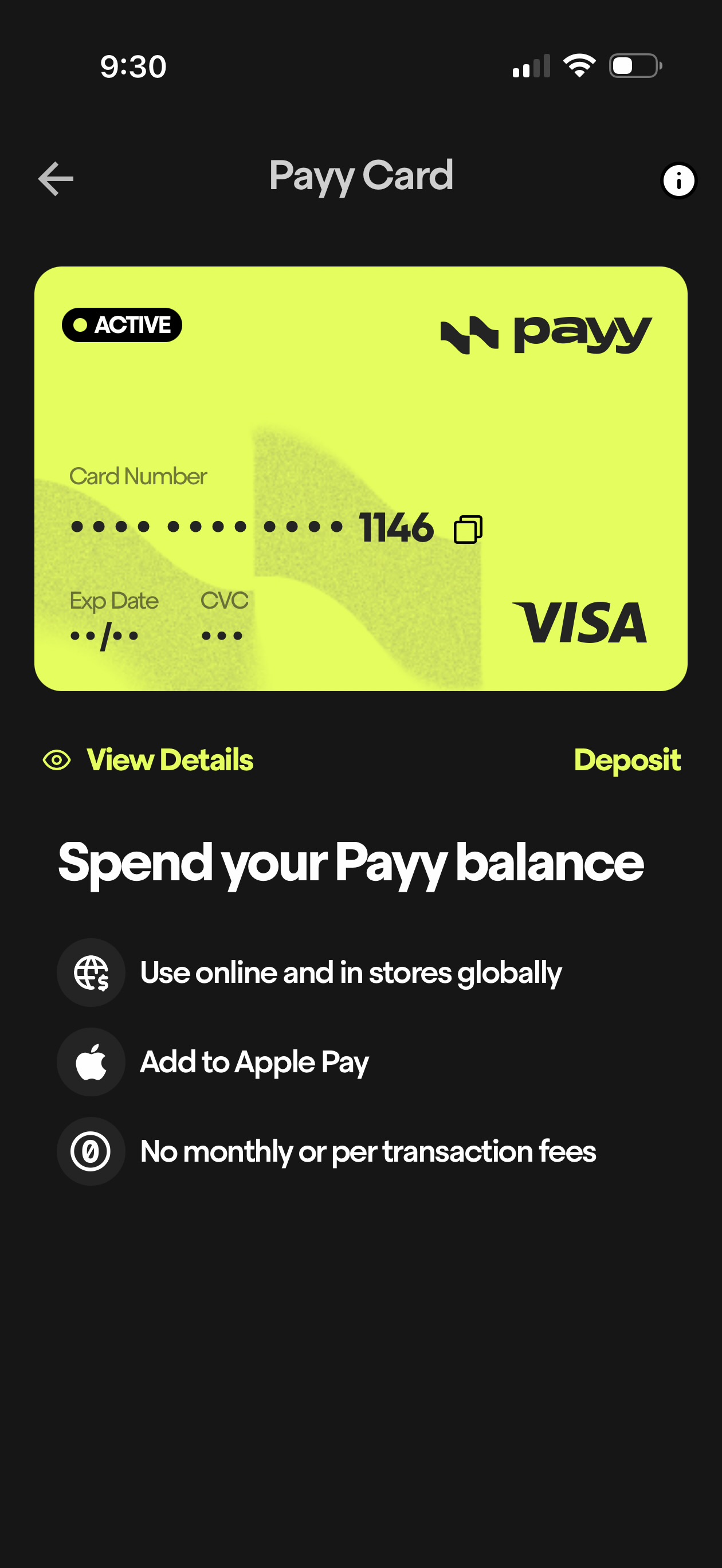

Payy Card is a self-custodial Visa Platinum prepaid card that settles transactions privately on Payy Network using zero-knowledge proofs, hiding wallet balances and spending amounts from public blockchain view.

Payy Card converts USDC to fiat at the point of sale like any other stablecoin card. The difference: every transaction settles on Payy Network through zero-knowledge proofs that hide the sender, receiver, amount, and asset. Your Visa purchases cannot be linked to your on-chain wallet. No other crypto card does this.

The model is deliberately simple. One card tier. Zero fees on USD purchases. 1% FX on everything else. No cashback, no staking, no loyalty program. Privacy and self-custody are the entire value proposition.

Physical and Virtual Cards

The virtual card is issued instantly after KYC verification. You receive the card number in-app and can copy/paste it for online purchases or manually add it to Apple Pay or Google Pay.

A physical "Light-Up Card" exists - a contactless-only Visa with an LED-illuminated Payy logo that glows when tapped. It requires 100,000 Payy Points (earned through referrals at 10,000 points per friend) and is currently sold out with no restock timeline.

There is no chip or magstripe on the physical card. Contactless tap only.

SpendNode app screenshot

Payy Card - Visa Platinum with Apple Pay support, zero fees, and self-custodial spending. Neon-green card design.

Payment Network

Visa Platinum, accepted at 80+ million merchant locations worldwide. The card is US-issued, which means some online merchants in certain countries may reject it (this is a Visa network limitation, not a Payy limitation).

Security Features

- Self-custodial wallet: Keys generated and stored locally on device. No login, email, or password required

- Card freeze/unfreeze: Instant toggle in the app

- ZK privacy: Transaction amounts and wallet balances invisible on-chain

- Planned "Guardians" feature: Social recovery for account backup and fraud prevention (not yet live)

No 3D Secure mentioned in documentation. No virtual card number rotation. We reviewed the full security feature set and found no mention of transaction alerts or spending notifications either.

Fees and Rates

Since Payy has no tiers, no staking, and no rewards, the cost analysis is straightforward:

USD-Only Spending

| Monthly Spend | Annual Cost | Effective Rate |

|---|---|---|

| $500 | $0 | 0.00% |

| $1,500 | $0 | 0.00% |

| $3,000 | $0 | 0.00% |

The only cost is on-chain gas when bridging stablecoins to Payy Network. Using L2s (Base, Optimism, Arbitrum), this is under $0.10 per bridge transaction.

Non-USD Spending (100% foreign currency)

| Monthly Spend | Monthly FX Cost | Annual FX Cost | Effective Rate |

|---|---|---|---|

| $500 | $5 | $60 | 1.00% |

| $1,500 | $15 | $180 | 1.00% |

| $3,000 | $30 | $360 | 1.00% |

Mixed Spending (50% USD, 50% foreign)

| Monthly Spend | Monthly FX Cost | Annual FX Cost | Effective Rate |

|---|---|---|---|

| $1,000 | $5 | $60 | 0.50% |

| $2,000 | $10 | $120 | 0.50% |

| $4,000 | $20 | $240 | 0.50% |

Opportunity Cost (vs 2% Cashback Card)

| Monthly Spend | Payy Annual Cost | 2% Card Annual Return | Net Difference |

|---|---|---|---|

| $1,000 (USD) | $0 | +$240 | -$240 |

| $2,000 (mixed) | $120 | +$480 | -$600 |

| $3,000 (non-USD) | $360 | +$720 | -$1,080 |

Privacy has a price. For a $2,000/month mixed-currency spender, that price is approximately $600/year compared to a 2% cashback alternative like RedotPay or Crypto.com. Whether that cost is justified depends entirely on your threat model.

Foreign Exchange: Advertised vs Reality

Payy says "Visa/bank FX" and instructs users to set 1% in Visa's FX calculator. Let us test this:

Example: 100 GBP purchase

- Visa mid-market rate: 1 GBP = 1.2650 USD

- Visa retail rate (with 1% bank markup): 1 GBP = approx. 1.2777 USD

- You pay: $127.77 USDC for 100 GBP

- Actual cost: $1.27 (1.0% of transaction)

After reviewing the conversion math, this checks out. The 1% is clearly disclosed, and Payy does not add a hidden spread on top. Compare:

| Card | FX Fee (advertised) | Actual Total FX Cost |

|---|---|---|

| Payy | 1% bank fee | approx. 1.0% |

| Bybit | 0% + conversion fee | Varies by region |

| RedotPay Virtual | 1.5% | approx. 1.5% |

| Crypto.com Ruby | 0% | 0% (requires $400 CRO stake) |

| Bleap | 0% | 0% (EEA only) |

| MetaMask | 0-0.875% token fee | 1% cross-border (Virtual), 0% (Metal) |

Payy is middle of the pack on FX. Not the cheapest, not the most expensive. The zero-fee claim holds for USD transactions.

Spending Limits

| Limit Type | Amount |

|---|---|

| Daily spending | No preset limit (wallet balance) |

| Monthly spending | No preset limit (wallet balance) |

| ATM withdrawal | Private beta (contactless only) |

Payy does not publish spending caps beyond your wallet balance. We track spending limits across every card in our database, and Payy's approach is consistent with prepaid card models - you cannot spend more than you have loaded.

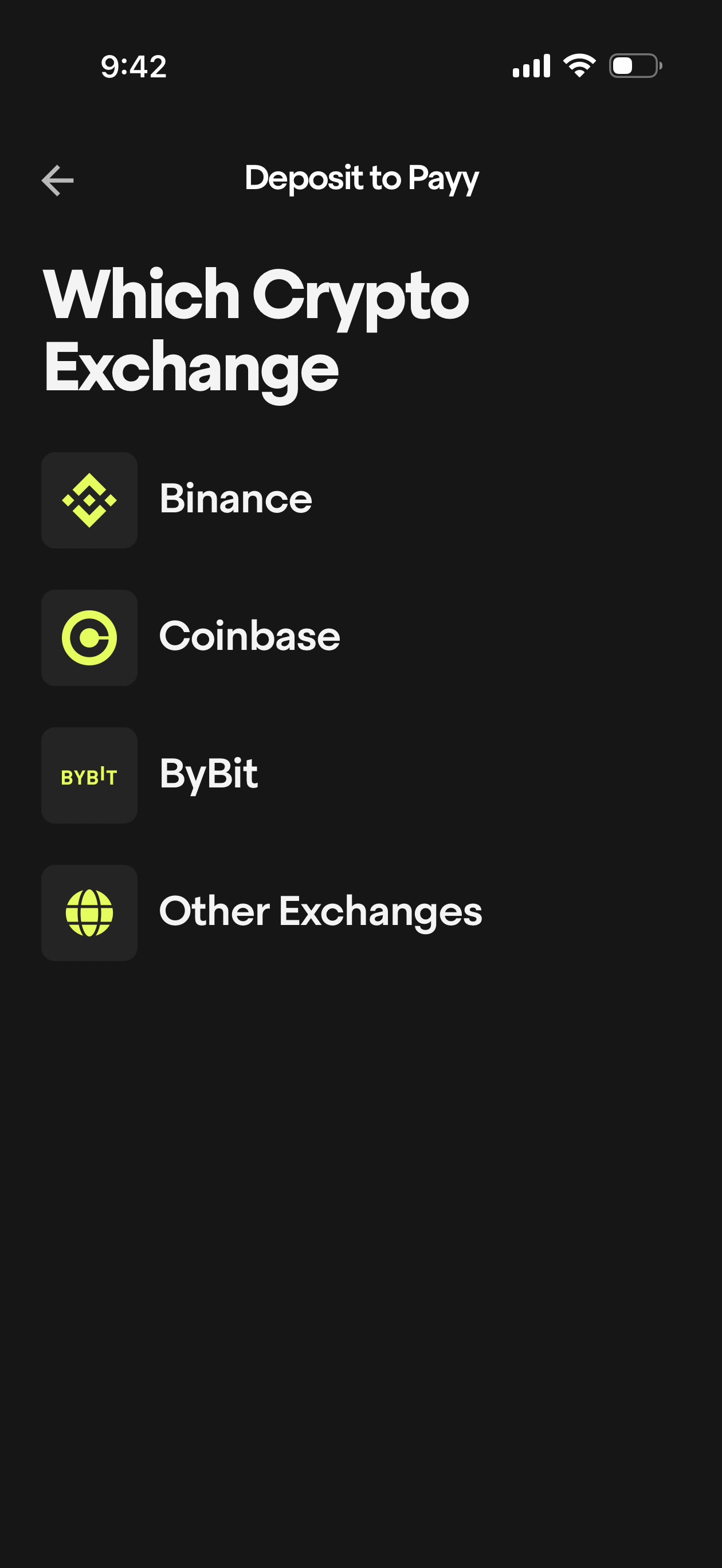

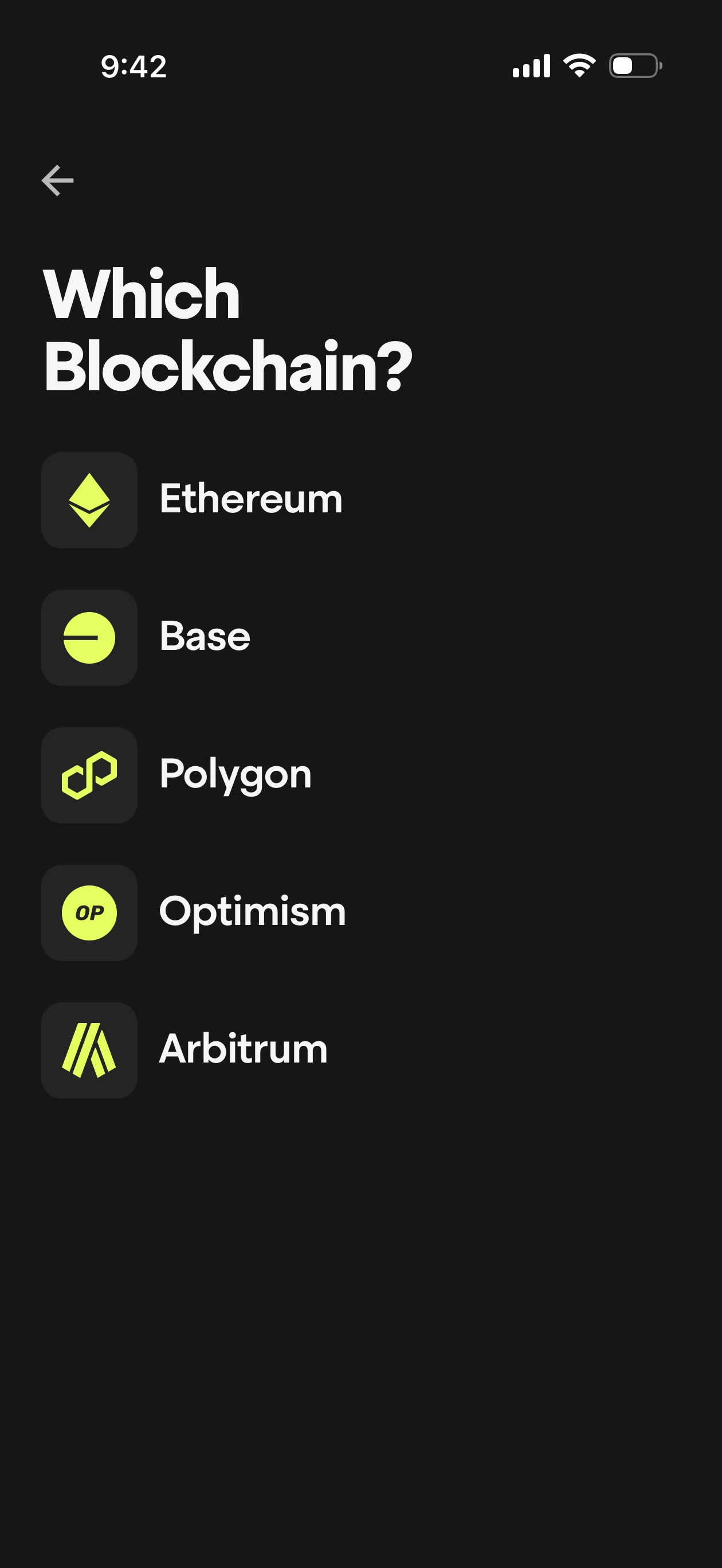

Deposit Networks

We tested the full deposit flow - it guides you through exchange selection (Binance, Coinbase, ByBit) and then chain selection. Five EVM chains are supported with varying gas costs.

Payy deposit flow: choose your exchange (Binance, Coinbase, ByBit) then select chain (Ethereum, Base, Polygon, Optimism, Arbitrum).

| Network | Assets | Estimated Gas |

|---|---|---|

| Ethereum | USDC, USDT, USDC.e | $1-5 |

| Base | USDC, USDT, USDC.e | $0.01-0.05 |

| Polygon | USDC, USDT, USDC.e | $0.01-0.05 |

| Optimism | USDC, USDT, USDC.e | $0.01-0.10 |

| Arbitrum | USDC, USDT, USDC.e | $0.01-0.10 |

Fiat Deposits

| Country | Method | Status |

|---|---|---|

| United States | ACH bank transfer | Beta |

| Argentina | Local bank transfer | Live |

| Europe (SEPA) | Bank transfer | Planned |

| India (UPI) | Mobile payment | Planned |

| Brazil (PIX) | Instant transfer | Planned |

| Kenya (M-Pesa) | Mobile money | Planned |

Restrictions

- Physical card is contactless-only (no chip, no magstripe)

- Some international online merchants reject US-issued cards

- ATM withdrawals require private beta access (contact support)

- Standard Visa prohibited merchant categories apply

How Spending Works

Example: $47.50 grocery purchase at Whole Foods (USD)

Step 1: You hold USDC on Payy Network in your self-custodial wallet. You bridged it from Base earlier (cost: approx. $0.05).

Step 2: You tap your Payy Card (via Apple Pay) at checkout. The terminal communicates with Visa.

Step 3: Payy Network generates a ZK proof from your Privacy Vault. The proof validates: (a) your signed transaction, (b) sufficient balance via UTXO notes, (c) consistency with stored notes. The proof calls PrivacyBridge.transfer() using an ephemeral keypair. The sender, amount, and balance are never exposed.

Step 4: Visa settles $47.50 with Whole Foods in USD. Your USDC balance decreases by $47.50. The on-chain record shows a ZK proof was submitted - nothing else. No amount, no sender address, no receiver.

Cost: $0.00. USD transaction, zero fees.

Same purchase in EUR (Berlin grocery store, 44.20 EUR):

- Visa converts EUR to USD at mid-market rate

- Payy/bank FX markup: 1% = approx. $0.49

- Total cost: $49.29 (USDC debited) for a 44.20 EUR purchase

Rewards on This Tier

Payy offers zero cashback, zero staking rewards, and zero loyalty perks on card spending. This is by design - the entire value proposition is transaction privacy and self-custody, not monetary rewards. Payy Points exist for referrals (10,000 per friend) but have no monetary value and cannot be converted to cashback.

Privacy Architecture

Payy Network is purpose-built for private stablecoin payments. Three mechanisms work together:

Private Transfers (Privacy Layer): All ERC-20 transfers on the Privacy Layer are fully private. Zero overhead on the EVM Layer. Zero gas fees. The sender, receiver, amount, and asset are all hidden. This is where card settlements happen.

Stealth Transactions (EVM Layer): When you need to interact with smart contracts, funds move from the Privacy Layer to a fresh one-time stealth address. After the interaction, funds return to the Privacy Layer. It is impossible to determine the true sender or receiver.

PUSD Native Gas: Payy Network uses PUSD (a US treasuries-backed stablecoin, Genius Act compliant) as its native gas token. Gas is stable, predictable, and denominated in USD. No volatile gas token to hold.

Why this matters for card users: On Ethereum, if you hold $50,000 in USDC and buy a $5 coffee, anyone can see your full balance. On Payy Network, the $5 coffee transaction is a ZK proof - your balance, the amount, and the merchant address are all hidden.

Encrypted Lineage for compliance: Payy uses nullifiers to prevent transaction chain tracking. If law enforcement presents a valid on-chain governance proposal, encrypted lineage can be decrypted. This is the compliance escape valve that separates Payy from fully anonymous systems like Tornado Cash.

How This Tier Compares

For US users spending in USD: Payy is effectively free. The only comparable zero-cost option is MetaMask Card which also charges no fees on USD. MetaMask settles on Linea (public), Payy settles privately. If privacy matters, Payy wins. If you want DeFi integration, MetaMask wins.

For EEA users: Bleap offers 0% FX and 2% USDC cashback with self-custody in the EEA. On $2,000/month, Bleap returns $480/year while Payy costs $240/year in FX. That is a $720/year swing in Bleap's favor. Choose Payy only if on-chain privacy justifies $720/year.

For global stablecoin holders: RedotPay supports more chains (including Solana), offers up to 2% cashback, and has physical cards readily available. RedotPay is the better general-purpose stablecoin card. Payy is the specialist privacy card.

For self-custody purists: Payy, MetaMask, and Bleap are the three self-custodial options. Payy adds ZK privacy. MetaMask adds DeFi wallet integration. Bleap adds cashback. Pick your priority.

Payy Card unique value: It is the only crypto card where your spending is cryptographically private on-chain. No other card offers this.

Real User Scenarios

Scenario 1: David, a US Software Engineer ($2,500/month)

Setup: Holds USDC from freelance crypto payments. Bridges from Base to Payy Network weekly. All spending in USD (groceries, gas, subscriptions).

Results after 6 months:

- Total spent: $15,000

- FX costs: $0 (all USD)

- Bridge gas: approx. $3 (24 weekly bridges on Base)

- Rewards earned: $0

- Net cost: $3

Verdict: "Basically free. My Coinbase card would have earned me $300 in cashback, but it also shows my entire USDC balance to anyone who looks up my address. I will take the privacy."

Scenario 2: Sofia, an Argentine Remote Worker ($1,200/month)

Setup: Receives salary in USDT on Arbitrum. Bridges to Payy Network. Spending split: 30% USD (online subscriptions), 70% ARS (local purchases).

Results after 6 months:

- Total spent: $7,200

- USD portion ($2,160): $0 FX

- ARS portion ($5,040): $50.40 FX (1%)

- Bridge gas: approx. $2

- Rewards earned: $0

- Net cost: $52.40

Verdict: "The fiat deposit from Argentine bank accounts is a huge plus. Most crypto cards make me go through an exchange first. The 1% FX is standard - I pay the same or more with traditional cards here."

Scenario 3: Kenji, a Tokyo-Based DeFi Trader ($5,000/month)

Setup: Large USDC holdings across multiple chains. Bridges from Ethereum. All spending in JPY.

Results after 6 months:

- Total spent: $30,000

- FX costs: $300 (1% on all JPY transactions)

- Bridge gas: approx. $30 (monthly bridges on Ethereum mainnet)

- Rewards earned: $0

- Net cost: $330

Verdict: "For $330 I get complete separation between my DeFi portfolio and my daily spending. My wallet holds seven figures - I do not want that visible every time I buy lunch. But I would prefer to bridge from a cheaper L2."

Is the Payy Card Safe?

USDC balance (risk: LOW-MODERATE): Your funds are self-custodied. Private keys are on your device. Payy cannot access or freeze them. However, your USDC lives on Payy Network - a custom chain operated by Polybase Labs. If the chain stops producing blocks, you would need a migration path. The bridge infrastructure (Across, Mayan) is third-party, but the Polygon lock-and-mint bridge is Payy-controlled.

Pending card settlements (risk: MINIMAL): Visa settlements are near-instant. Maximum exposure is one or two unsettled transactions.

Payy Points (risk: ZERO): Points have no monetary value. Nothing to lose.

Comparison to alternatives:

- Custodial cards (Binance, Bybit): If the exchange fails, you lose your entire balance. Payy is significantly safer.

- Self-custodial on public chains (MetaMask on Linea, Bleap on Polygon): If the card vendor fails, your funds are on a public chain with multiple exit paths. Payy's single-chain risk is higher.

- Self-custodial on vendor chain (Payy on Payy Network): Unique risk profile. Funds are safe from company access but dependent on chain liveness.

Who Should Choose This Tier

Use Payy Card if:

- You hold significant stablecoin balances and want spending privacy

- You primarily spend in USD (zero effective cost)

- You value self-custody and do not trust custodial card providers

- You are in a region where financial transaction privacy has practical importance

- You accept zero rewards as the cost of privacy

Skip Payy Card if:

- You want any form of cashback or rewards on your spending

- You spend primarily in non-USD currencies and want to minimize costs

- You need regular ATM withdrawals (private beta only)

- You prefer your funds on established chains (Ethereum, Polygon) rather than a vendor-specific chain

- You need a physical card (sold out)

Our view: Payy Card is not competing with cashback cards. It is competing with financial privacy tools. For users who understand what on-chain transparency costs them - whale wallets being tracked, spending patterns being analyzed, portfolio sizes being inferred from card transactions - Payy offers something genuinely new. The question is whether that privacy is worth the $240-$1,200/year you could earn in rewards elsewhere.

For US-based stablecoin holders who spend in USD, the math is simpler: Payy costs nothing. The only sacrifice is forgone rewards. For everyone else, the 1% FX fee and zero rewards make it a premium product where the premium is privacy.

Sources and Verification

All card specs, fees, and limits verified from:

- Payy Network

- Payy Card Documentation

- First-party app testing (Feb 2026)

User scenarios are composite illustrations using verified fee structures. Actual results depend on spending patterns, currency mix, and bridge gas at time of transaction.

FAQ

How do you choose Payy Card crypto cards?

We compare verified issuer sources, fees, and eligibility. Availability can change, so confirm with the issuer before applying.

Do all cards in this list offer the same benefits?

No. Each issuer defines its own program terms. Review the sources on each card profile.

Are these rankings or recommendations?

No. Lists are filtered views of cards in our database and do not imply rankings.

This is a prepaid card. Merchants that require pre-authorization holds (gas stations, hotels, car rentals, toll booths) may decline it. Fund only what you plan to spend.

You retain custody of your funds until the moment of spending. Your balance is not exposed to provider insolvency risk.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?

User Reviews

Reviews are moderated and may take a moment to appear.

Recent Updates to Payy Card

- Re-verified the page against the current structured card data

- No material data or logic changes were required in this pass