CASHBACK

Verified

SELF CUSTODY SPEND

Verified

STABLECOIN SPEND

Verified

Our Official Verdict

Zero Barriers: 3% Back on Every Purchase, No Stake Required

The ether.fi Core Card is the easiest entry point into DeFi spending. With 3%% cashback, a Free annual fee, and no staking requirement, it delivers premium rewards from day one. The trade-off: you miss lounge access and metal card perks reserved for higher tiers.

Fees & Charges

Annual Fee

Free

FX Fee

1%

ATM Fee

2%

Requirements

Supported Regions

GLOBAL, US, UK, EEA

Spendable Assets

USDC, ETH, eETH, weETH

ether.fi Core Card Review

The ether.fi Core Card is a self-custodial Visa card (crypto-backed, runs on Visa credit network) on the free tier of the ether.fi Cash program, offering 3% flat cashback on all purchases, spend-against-staked-ETH functionality for tax-efficient liquidity, Apple Pay and Google Pay support, 3 virtual cards, a $10,000/month fiat-to-crypto onramp at 0.2% fee, and Membership Points earning toward tier upgrades, available globally including US, UK, and EEA.

3% Cashback With No Stake, No Fee, No Lock-Up

We tested every free self-custodial crypto card in 2026, and most that offer 3% cashback require something in return. The Crypto.com Royal Indigo needs $5,000 in CRO staked for 6 months. The Plutus Visa requires a GBP 6.99/month minimum subscription (no free tier). The Bybit card tops out at 2% on the free tier.

The ether.fi Core Card delivers 3% flat cashback on all purchases with zero barriers: no annual fee, no staking requirement, no token lock-up, no minimum balance. You sign up, pass KYC, and start earning 3% immediately.

The catch is that this 3% is not a Core-exclusive advantage. Every tier in the ether.fi Cash program - from Core to VIP - earns the same 3% base cashback. What changes as you climb tiers are the metal card, lounge access, virtual card limits, and fiat-to-crypto onramp capacity. Core gives you the full cashback rate. Higher tiers add lifestyle perks around it.

Card Specs: What You Are Actually Getting

Physical and Virtual Cards

- Physical card: Plastic Pepe-themed Visa card shipped to your address

- Virtual cards: 3 virtual cards (for online purchases, subscriptions, or category separation)

- Design: Distinctive ether.fi branding with Pepe meme theme

Payment Network

- Network: Visa

- Acceptance: 100M+ merchant locations worldwide

- Contactless: Yes (NFC)

- Mobile wallets: Apple Pay, Google Pay

- Card type: Crypto-backed credit (borrow against staked ETH or spend stablecoins)

Security Features

- Self-custodial: You hold the keys. Funds stay in your wallet until transaction settlement

- Card controls: Freeze/unfreeze, spending limits per virtual card, real-time notifications via the ether.fi app

- Price protection: Up to $2,000 per item

- Purchase protection: Up to $10,000 coverage

- Extended warranty: Up to $10,000 per item

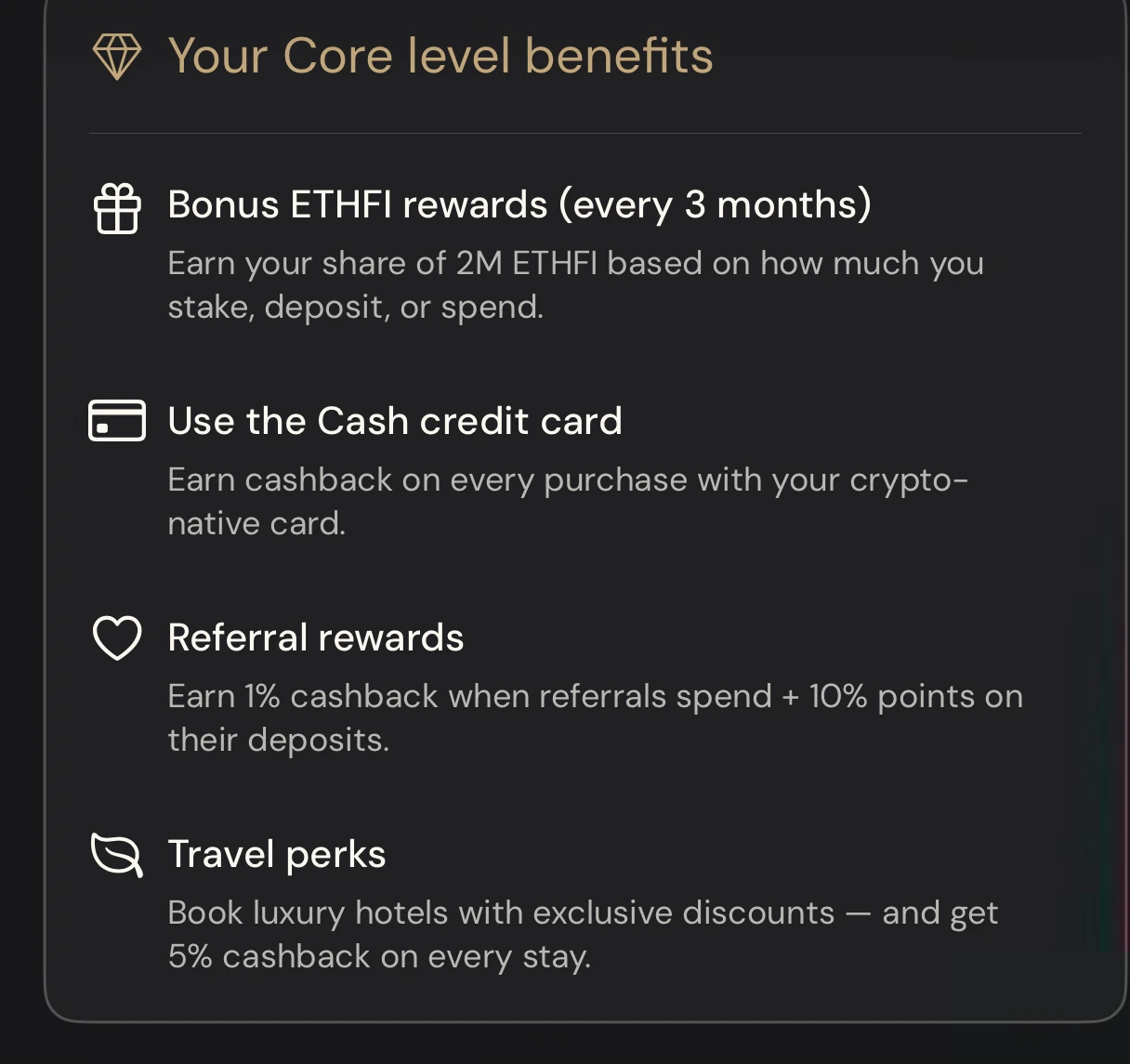

Bonus Perks (Even at Core)

- 5% cashback on hotel stays: Booked through the ether.fi travel portal, this stacks on top of the standard 3% card cashback for an effective 8% return on hotel spend

- Quarterly ETHFI bonus: Share of a 2M ETHFI token pool distributed to active cardholders each quarter

- Referral rewards: Earn 1% cashback on your referrals' card spending plus 10% of their deposit points

Core Benefits - 3% cashback, 5% on hotel stays, quarterly ETHFI bonus from 2M token pool, and referral rewards (1% of referrals' spend + 10% of their deposit points).

How Spending Works: Transaction Flow

Example: $1,200 laptop purchase online (US-based, paying from USDC balance)

Step 1: Fund your spending balance

- Hold USDC, ETH, eETH, or weETH in your ether.fi wallet

- If paying from stablecoins: USDC converts to local fiat at point of sale

- If paying from staked ETH: you borrow against your eETH/weETH collateral - no taxable sale occurs

Step 2: Pay at the merchant

- Use your physical card, virtual card, or Apple Pay/Google Pay

- The merchant charges $1,200

- ether.fi settles the transaction from your wallet

Step 3: Fees applied

- FX fee: 0% (domestic USD transaction)

- Conversion fee: 0% (USDC to USD is 1:1)

- Total fees on this transaction: $0

Step 4: Cashback credited

- 3% of $1,200 = $36 cashback

- Plus 3,000 Membership Points per $1,000 spent = 3,600 points earned

- Points contribute toward tier upgrades (Luxe at 10,000 points/month)

Step 5: The staked ETH advantage

- If you had paid from eETH collateral instead of USDC, the $1,200 in staked ETH continues earning EigenLayer restaking yield (currently 3-5% APY)

- For US holders: borrowing against collateral is generally not a taxable event, unlike selling ETH to fund a debit card

- You get to spend now AND keep your ETH position growing

The tax efficiency play: Spending against staked ETH lets you access liquidity without triggering capital gains. Your collateral earns yield while you spend borrowed value. Over a year of $2,000/month spending, the avoided capital gains tax at 15-20% long-term rates could save $3,600-$4,800 compared to selling ETH to fund a prepaid card.

Fee Deep Dive: The Real Cost

| Fee | Amount | Notes |

|---|---|---|

| Annual fee | $0 | Free tier, no subscription |

| FX fee | 1% | On all non-local currency transactions |

| ATM fee | 2% | No free allowance, flat 2% on all withdrawals |

| Fiat-to-crypto | 0.2% | $10,000/month limit |

| Crypto conversion | Included | No separate spread fee |

Net Return by Scenario

| Scenario | Cashback | FX Cost | Net Annual Return |

|---|---|---|---|

| $2,000/mo domestic only | 3% | 0% | $720/year |

| $2,000/mo, 50% international | 3% | 1% on $1K | $600/year |

| $2,000/mo, 100% international | 3% | 1% on $2K | $480/year |

| $5,000/mo domestic only | 3% | 0% | $1,800/year |

| $5,000/mo, 50% international | 3% | 1% on $2.5K | $1,500/year |

Key insight: When reviewing the fee impact, the 1% FX fee reduces the effective cashback from 3% to 2% on international transactions. For domestic-heavy spenders, Core delivers the full 3%. For international-heavy users, the effective rate of 2% still beats most free cards but falls behind Krak Mastercard (1% cashback, 0% FX) on pure fee avoidance.

Membership Points: The Upgrade Path

Core earns 3,000 Membership Points per $1,000 spent. Points accumulate monthly and determine your tier for the next month.

| Tier | Points Required | Monthly Spend Needed | Or Stake |

|---|---|---|---|

| Core | 0 | $0 | None |

| Luxe | 10,000/month | $3,334/month | 15,000 ETHFI |

| Pinnacle | 50,000/month | $16,667/month | 100,000 ETHFI |

| VIP | Invite only | N/A | N/A |

Points reset monthly. If your spending drops below the threshold and you do not hold the ETHFI stake, you revert to Core. The staking bypass is the stable path for users who want higher tier benefits without worrying about monthly spending fluctuations.

Natural upgrade path: At $3,334/month spending (the Luxe threshold), you earn $1,200/year in cashback at Core. Reaching Luxe adds metal card, conference lounge access, 65% hotel discounts, and $50,000/month fiat-to-crypto limit - all for free if your spending sustains the points threshold.

Limits and Restrictions

| Limit | Amount |

|---|---|

| Fiat-to-crypto monthly | $10,000 |

| Fiat-to-crypto fee | 0.2% |

| Virtual cards | 3 |

| Physical cards | 1 |

| Spending cap | Dynamic (based on collateral) |

Availability

- Regions: US, UK, EEA, and select global markets

- KYC: Full verification required

- Assets supported: USDC, ETH, eETH, weETH

What Happens If ether.fi Goes Down?

Your crypto assets:

- Self-custodial. You hold the keys, not ether.fi

- If ether.fi's card program shuts down, your wallet remains yours

- eETH and weETH are liquid restaking tokens on Ethereum L1 - they exist independently of ether.fi's card infrastructure

- You can exit positions through any DEX regardless of ether.fi's operational status

Your pending cashback:

- Cashback earned but not yet settled could be lost in a shutdown

- Mitigation: Cashback is typically credited within 24-48 hours - the exposure window is small

Your outstanding loans (if spending against staked ETH):

- If the card program terminates, loan terms would depend on the smart contract architecture

- In a worst case, you may need to repay the borrowed amount to reclaim collateral

- Your collateral is on-chain and verifiable, not in a custodial black box

Risk comparison:

| Card | Asset Protection | Cashback Risk | Shutdown Impact |

|---|---|---|---|

| ether.fi Core | Self-custodial (you hold keys) | Pending rewards only | Minimal - assets are yours |

| Nexo Card | Custodial (Nexo holds) | Loyalty-dependent | High - assets on platform |

| Crypto.com Basic | Custodial (exchange) | None (0% rewards) | High - balance at risk |

| Gnosis Pay | Self-custodial (Safe) | GNO-denominated | Minimal - assets are yours |

Assessment: Low risk. Self-custodial architecture means the card is the weakest link, not the wallet. If the card stops working, you still have all your crypto. This is the fundamental advantage of self-custody over every exchange-linked card.

Real User Scenarios

Scenario 1: Jake (Austin, TX Software Engineer, $3,500/month spending)

Setup:

- ether.fi Core Card (free tier)

- Holds 10 ETH in eETH for restaking yield (3.8% APY)

- Borrows against eETH collateral for card spending

- 90% domestic spending, 10% international (conference travel)

Results after 12 months:

- Total spending: $42,000

- Cashback (3%): $1,260

- FX cost (1% on $4,200 international): -$42

- Restaking yield on 10 eETH: approx. $2,280 (at $6,000/ETH)

- Capital gains tax avoided (15% on $42,000 if he had sold ETH): approx. $6,300 saved

- Net annual value: $1,218 cashback + $2,280 yield + $6,300 tax savings = $9,798

His verdict: "The tax efficiency is the real story. I would have paid $6,300 in capital gains if I sold ETH to fund a debit card. Instead, I borrowed against it, kept my staking yield running, and still earned $1,218 in cashback. The Core Card is not just a spending card - it is a tax planning tool for ETH holders."

Scenario 2: Maria (Lisbon Digital Nomad, EUR 2,000/month spending)

Setup:

- ether.fi Core Card (free tier)

- Holds USDC in ether.fi wallet

- Spends across EUR, GBP, THB, VND (70% non-EUR)

- Uses 2 of 3 virtual cards for recurring subscriptions

Results after 12 months:

- Total spending: EUR 24,000

- Cashback (3%): EUR 720

- FX cost (1% on EUR 16,800 non-EUR): -EUR 168

- Net annual value: EUR 552

Her verdict: "The 3% cashback is best-in-class for a free card. The 1% FX fee eats into it when I spend in Thai baht or Vietnamese dong, but the effective 2% on international transactions still beats my Portuguese bank card's 0% cashback + 2.5% FX fee. I am considering the upgrade to Luxe for the conference lounge access - I spend $3,500+/month when including conference tickets, which would qualify me automatically."

Scenario 3: Kevin (Singapore DeFi Researcher, $5,000/month spending)

Setup:

- ether.fi Core Card (free tier)

- Holds 50 eETH in liquid restaking

- Borrows against eETH for card spending

- 80% SGD domestic, 20% USD conference travel

- Earns above the Luxe threshold but chooses to stay at Core (does not need lounge or metal card)

Results after 12 months:

- Total spending: $60,000

- Cashback (3%): $1,800

- FX cost (1% on $12,000 non-SGD): -$120

- Membership Points earned: 180,000 (well above Pinnacle threshold)

- Net annual value: $1,680 cashback

His verdict: "I earn enough points for Pinnacle every month but do not bother upgrading because Core gives me the same 3% cashback. The only reason to move up is if you need the metal card, lounge access, or more virtual cards. For pure cashback, Core is the rational choice - the tier system is about perks, not rates."

How the ether.fi Core Card Compares

For free self-custodial cards:

- Gnosis Pay: 1-5% GNO cashback, 0% FX, self-custodial via Safe. Gnosis wins on FX (0% vs 1%) and has a higher cashback ceiling (5% at top GNO tier). Core wins on base rate (3% vs 1% at Gnosis entry), no token holding required, and US availability (Gnosis is EEA-only)

- Ready Lite Card: 0.5% STRK cashback, 1% FX, self-custodial on Starknet. Core crushes on cashback (3% vs 0.5%). Ready wins only on the Starknet ecosystem angle

For free cards in general:

- Nexo Card: 0-2% cashback (tier-dependent), 0.2% FX (EEA weekday). Nexo wins on lower FX for EEA international users (0.2% vs 1%). Core wins on cashback rate (3% vs 2% max) and self-custody. Nexo requires Platinum loyalty tier (10% portfolio in NEXO) for the full 2% and $5,000 minimum balance for any cashback

- Krak Mastercard: 1% cashback, 0% all fees. Krak wins on simplicity and zero FX. Core wins on raw cashback (3x the rate). For domestic spenders, Core earns $720/year vs Kraken's $240 on $2,000/month

Core's unique value: The only free crypto card with 3% flat cashback, self-custody, and spend-against-staked-ETH tax efficiency. No other card combines all three. You pay for this combination with the 1% FX fee on international transactions - a fair trade for most users whose spending is primarily domestic.

The Verdict: Is the ether.fi Core Card Worth It in 2026?

Use the ether.fi Core Card if:

- You hold ETH, eETH, or weETH and want to spend without selling (tax efficiency)

- You want the highest flat cashback rate available on a free, self-custodial card

- Your spending is primarily domestic (where the 1% FX fee is irrelevant)

- You value holding your own keys over trusting an exchange

Skip the ether.fi Core Card if:

- You spend heavily abroad and need 0% FX - the Krak Mastercard or Wirex Standard eliminate FX costs entirely

- You want diversified crypto rewards (Core pays in ether.fi ecosystem tokens, not BTC or ETH). For BTC rewards, consider the Gemini Credit Card

- You need ATM access - the 2% ATM fee with no free allowance is expensive. The Crypto.com Royal Indigo offers $400/month free ATM

- You want a metal card - Core is plastic only. Upgrade to Luxe ($3,334/month spend threshold) or consider Plutus for metal

Final verdict: We confirmed that the ether.fi Core Card is the highest-cashback free card in crypto. At 3% flat with $0 annual fee and self-custodial architecture, it outearns every free-tier competitor on domestic spending. The 1% FX fee is the one weakness, making it a 2% effective card for international transactions - still competitive but no longer dominant. For Ethereum holders who can use the spend-against-staked-ETH feature, the tax savings alone can exceed the cashback value by multiples. It is the best free entry point into DeFi-native spending available in 2026.

Sources and Verification

All card specs, fees, and limits verified from:

FAQ

Do I need to stake ETHFI for the Core tier?

No. Core is the free default tier. All new users start at Core with no staking or points requirement.

How do I upgrade from Core to Luxe?

Earn 10,000 Membership Points in a calendar month or stake 15,000 ETHFI. Points accumulate at 3,000 per $1,000 spent.

This card requires token staking to unlock higher reward tiers. If the staked token's price drops, your losses may exceed the cashback earned. Consider the break-even math before locking funds.

You retain custody of your funds until the moment of spending. Your balance is not exposed to provider insolvency risk.

Fees shown above are the card's disclosed fees. Additional costs may apply: Visa/Mastercard network spread (typically 0.5-0.9%), crypto-to-fiat conversion spread at point of sale, and blockchain gas fees for on-chain top-ups.

Found any issues?