The U.S. Department of Labor published a Notice of Proposed Rulemaking on March 30, 2026, titled "Fiduciary Duties in Selecting Designated Investment Alternatives." The rule creates a safe harbor framework under ERISA that would give 401(k) plan fiduciaries legal protection when evaluating cryptocurrency, private equity, real estate, and other alternative investments for inclusion in retirement menus.

Americans held $10.1 trillion in 401(k) plans as of December 31, 2025. None of that money has had a practical path into crypto, because the litigation risk for fiduciaries has been too high. This rule is designed to change that calculus.

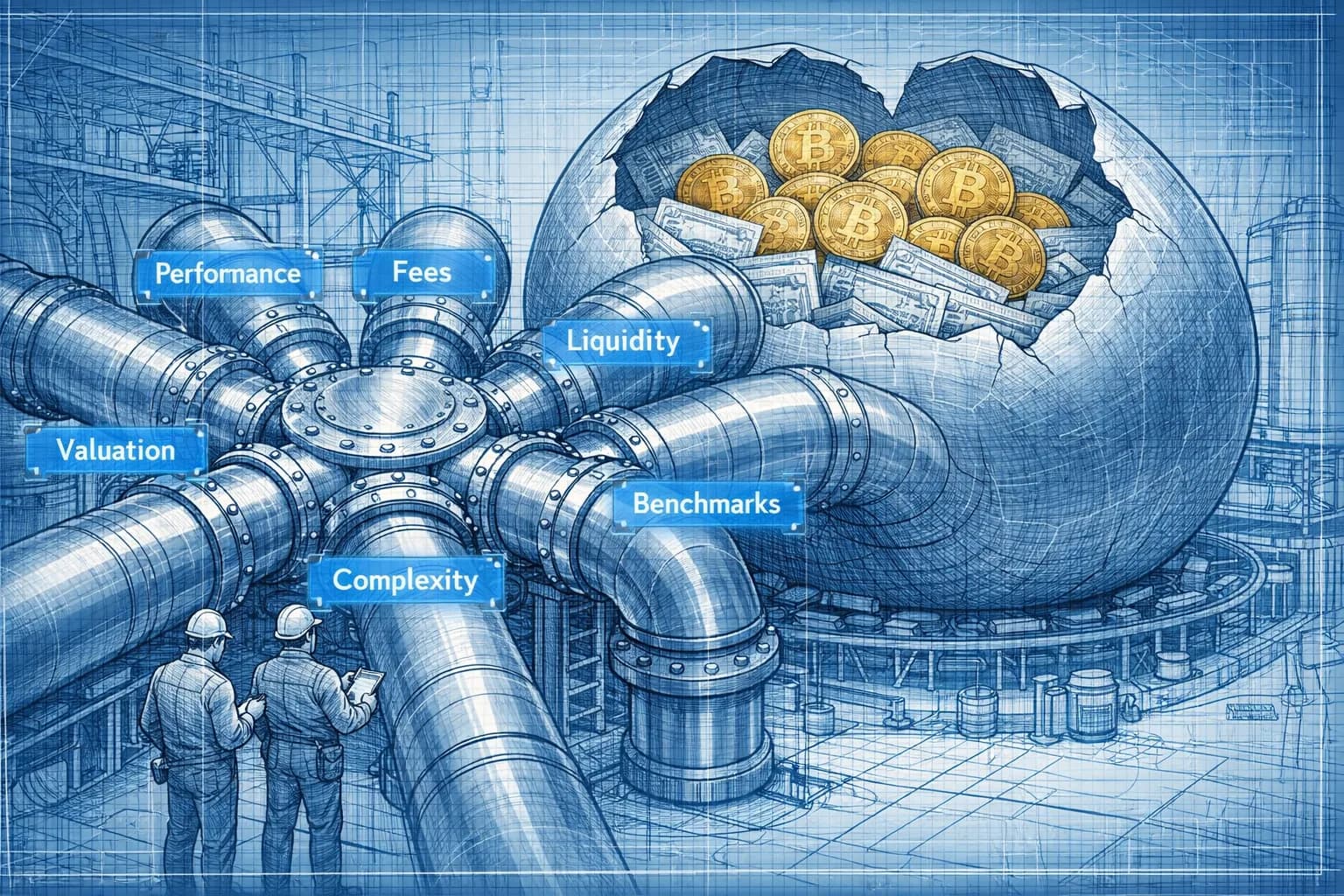

The Six-Factor Framework That Replaces the Biden-Era Warning

In March 2022, the Biden administration's Employee Benefits Security Administration issued Compliance Assistance Release 2022-01, which warned fiduciaries to "exercise extreme care" before adding cryptocurrency to any retirement plan. The release did not ban crypto outright, but the message was clear enough: add Bitcoin to your 401(k) menu and expect a lawsuit.

The new proposed rule reverses that posture. It establishes six factors a fiduciary must evaluate when considering an alternative investment: performance history, fees, liquidity, valuation methods, benchmarking, and complexity. If a fiduciary documents a thorough analysis across all six and reaches a reasoned conclusion, the rule grants a rebuttable presumption that they satisfied their ERISA duty of prudence.

In plain terms: follow the process, and you get legal cover. The DOL is not telling plan sponsors to add Bitcoin. It is telling them they will not be punished for seriously evaluating it.

What This Does Not Do

The rule does not mandate crypto in any retirement plan. It does not create a Bitcoin allocation default. It does not override individual plan sponsor discretion or state-level fiduciary standards.

It also does not guarantee protection in court. The Supreme Court's 2024 decision eliminating Chevron deference means agency rules like this one receive less judicial deference than they once did. A plan sponsor who follows the six-factor framework could still face litigation, though the safe harbor creates a stronger defense than anything that existed before.

Industry skeptics have noted on CNBC that the practical effect may take years to materialize. Most large 401(k) administrators use conservative investment committees that move slowly, and the six-factor safe harbor covers selection only. The DOL has signaled it will issue separate guidance on ongoing monitoring, which fiduciaries will likely want before committing.

The 60-Day Comment Window

The proposed rule is open for public comment until June 1, 2026. After that, the DOL will review submissions and potentially revise the rule before issuing a final version. The timeline from proposed rule to final rule typically runs six to eighteen months, meaning the earliest realistic effective date is late 2026 or early 2027.

The comment period is where the real battle happens. Expect submissions from the Investment Company Institute (which represents mutual fund managers holding $5.8 trillion of the 401(k) market), crypto-native asset managers, ERISA litigation attorneys, and consumer advocacy groups. The crypto industry's challenge is not convincing the DOL, which already proposed the rule. The challenge is building a comment record strong enough to survive the inevitable legal challenge.

How Trump's Executive Order Got Here

This proposal traces back to an executive order President Trump signed in August 2025, directing the Labor Secretary to review ERISA guidance on alternative investments within 180 days. Deputy Labor Secretary Keith Sonderling, who has been vocal about "investment neutrality," oversaw the drafting process. The White House Office of Information and Regulatory Affairs completed its review in late March, clearing the rule for publication.

The sequence matters because it establishes political durability. Executive orders can be reversed by the next administration, but a finalized ERISA rule goes through formal rulemaking under the Administrative Procedure Act. Reversing it would require the same multi-month notice-and-comment process.

What This Means for Crypto Card Users

The 401(k) rule and the crypto card market occupy different ends of the same pipeline. Retirement plans are where Americans accumulate crypto exposure over decades. Crypto cards are where they spend it. If Bitcoin and Ethereum start appearing in 401(k) menus, even as a 1-3% allocation option, the number of Americans who hold crypto passively will grow substantially. That expands the addressable market for crypto spending products from today's early adopters to the broader retirement-saver population.

The timeline is long. But the direction is set.

Overview

The Department of Labor's proposed rule creates a six-factor safe harbor for 401(k) fiduciaries evaluating crypto and other alternative assets, reversing the Biden era's chilling effect on digital asset inclusion in retirement plans. The $10.1 trillion 401(k) market does not gain Bitcoin exposure overnight, but the litigation barrier that kept fiduciaries from even considering it is being formally dismantled. Comments close June 1, 2026.